Introduction: A Strategic Shift in Group Audit Oversight

The revised Standard on Auditing (SA) 600 marks a significant shift in how complex, multi-entity business groups are audited. This revision goes beyond a technical update for auditors; it fundamentally reshapes expectations for group management, boards, and corporate governance.

Under SA 600 (Revised), group audits are designed to be risk-based, coordinated, and driven from the center. As a result, management and boards should expect deeper engagement, greater transparency, and more structured dialogue throughout the audit process.

Here is what Boards and Executive teams need to know about the strategic implications of SA 600 (Revised):

The Core Shift: What SA 600 (Revised) Means for Group Management

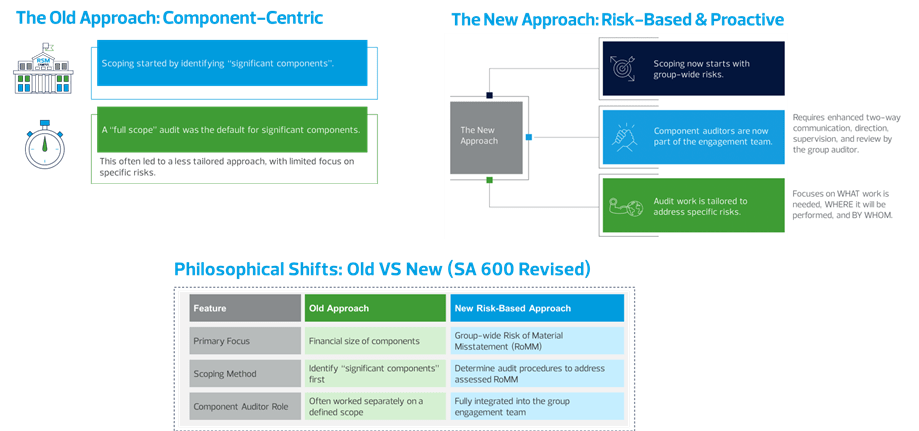

The most critical change introduced by SA 600 (Revised) is that the Group Engagement Partner is fully accountable for the group audit opinion, regardless of the extent of work performed by component (subsidiary) auditors.

Implications for Management include:

- Unrestricted Access (Non-Negotiable)

Prior to the engagement, management must agree to provide unrestricted access to people, information, and documentation across all group entities (Par. 19).

- Centralized Direction

Group auditors will drive audit strategy at the group level. Local entities should expect instructions aligned with a coordinated, group-wide audit plan rather than operating independently.

Strengthening the Chain: Why Communication with Component Auditors is Critical

SA 600 (Revised) requires structured, two-way communication between group auditors and component auditors. Management plays a critical role in enabling this communication.

- Early Alignment

Component CFOs and controllers should be briefed early on the new expectations. A group-wide audit kick-off meeting is strongly recommended.

- Top-Down Information Flow

Group management must proactively cascade information on related-party transactions, going concern considerations, fraud risks, and group-wide risk areas to ensure audit focus is aligned.

Risk-Based Audits as a Governance Tool

SA 600 (Revised) enforces a rigorous risk-based audit approach, concentrating audit effort where the risk of material misstatement is highest.

Management should anticipate:

- Increased scrutiny over recently acquired or reorganized entities

- Focus on complex or non-routine transactions

- Heightened attention on areas identified in Appendix 3 of the standard

The group consolidation process is explicitly identified as a key risk area. Group auditors are required to perform specific procedures to evaluate the appropriateness, completeness, and accuracy of consolidation adjustments, reclassifications, and intercompany eliminations (Par. 38, A141).

This approach offers management a strategic opportunity: by understanding audit focus areas, internal risk assessment and control monitoring processes can be better aligned.

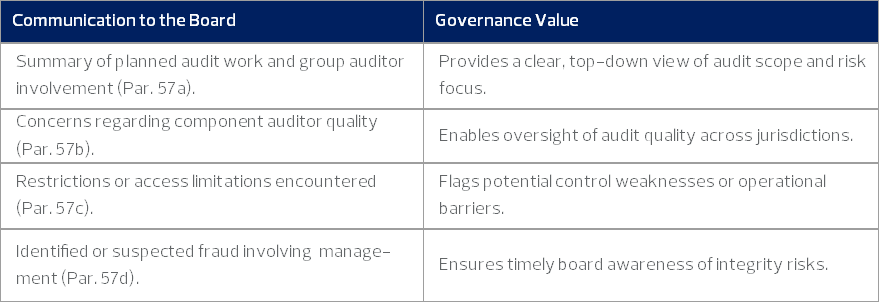

From Audit to Governance: Enhancing Transparency with the Board

SA 600 (Revised) strengthens audit committee oversight by expanding required communications between auditors and the board.

Management’s Preparation Checklist for SA 600 (Revised)

To ensure a smooth transition, management should:

- Establish a formal “access-all-areas” audit protocol

- Brief subsidiary leadership on transparency and cooperation expectations

- Clearly document the rationale for consolidation adjustments

- Identify and prepare documentation for high-risk areas

- Prepare the board with a briefing on scope and expected audit focus

By embracing these changes, organizations can turn compliance with SA 600 (Revised) into a catalyst for stronger financial discipline and governance.

By Edward B. Hutajulu & Tyas Widyanti, Audit Practice