RSM INDONESIA CLIENT ALERT – 20 August 2025

The Government has expanded its efforts to tax the e-commerce sector by issuing Minister of Finance Regulation No 37 Year 2025 concerning “the Appointment of Other Parties as Income Tax Collectors and the Mechanism of Collection, Deposit, and Reporting Income Tax collected by the Other Parties from Income earned by Domestic Traders through e-commerce Marketplaces” (PMK-37) on 11 June 2025.

PMK-37 states that e-commerce marketplaces can be appointed by the Director-General of Taxation (via delegated authority from the Minister of Finance) to collect Article 22 income tax from transactions involving domestic traders.

PER-15/PJ/2025, the related regulation stipulating the monetary and/or traffic/user thresholds to be met before an e-commerce marketplace can be appointed to collect Article 22 tax, was issued on 5 August 2025 (PER-15).

WHEN IS PMK-37 EFFECTIVE?

PMK-37 is effective commencing 14 July 2025, although it required the issue of the Director-General of Taxation (DGT) regulation stipulating the monetary and traffic/user thresholds. These thresholds are now stipulated by PER-15 and therefore the DGT can proceed with appointing e-commerce marketplaces as Article 22 tax collectors (refer to next page regarding the thresholds).

WHICH TAXPAYERS ARE SUBJECT TO ARTICLE 22 TAX PER PMK-37?

PMK-37 applies to domestic traders that earn income using e-commerce marketplaces that have been appointed as Article 22 tax collectors.

“Domestic traders” are defined as individuals or entities (badan) that reside or are domiciled in Indonesia who conduct e-commerce using facilities that are either created and managed directly by themselves or that are owned by an e-commerce marketplace or using other electronic systems that provide facilities for e-commerce.

Further, these individuals or entities must:

- Receive income using a bank account or similar financial account; and

- Conduct transactions using an internet protocol address in Indonesia or a telephone number with an Indonesian country code.

Finally, domestic traders shall also include delivery companies, insurance companies, and other parties conducting transactions with buyers of goods and/or services via e-commerce marketplaces.

WHICH E-COMMERCE MARKETPLACES CAN BE APPOINTED AS ARTICLE 22 TAX COLLECTORS AND WHAT ARE THE THRESHOLDS?

Both foreign and domestic e-commerce marketplaces can be appointed by the DGT as an Article 22 tax collector if the marketplace meets the following criteria:

a.) Uses an escrow account to receive income earned by the domestic traders (i.e. the e-commerce marketplace has the ability to collect Article 22 tax from those funds), and

b.) The e-commerce marketplace’s activity exceeds either:

- A certain threshold for total transaction value during a 12 months period and/or

- A certain threshold for the traffic amount or users who access the marketplace during a 12 months period

The monetary and traffic/user thresholds shall be stipulated by the DGT in accordance with delegated authority from the Minister of Finance.

The threshold criteria per (b) are the same as those regulated in Part 19 of Minister of Finance Regulation No. 81/2024 dated 14 October 2024 (PMK-81), regarding the appointment of parties as collectors of VAT where intangible goods and/or services are provided via e-commerce from overseas to buyers/users in the Indonesian customs area.

Further, the actual threshold amounts stipulated in PER-15 are the same as those stipulated by the implementing regulation for PMK-811. That is:

- If the value of transactions in Indonesia within a 12-month period exceed IDR 600 million or IDR 50 million per month and/or

- If the amount of traffic or users in Indonesia within a 12-month period exceeds 12,000 or 1,000 per month.

E-commerce marketplaces can also proactively request appointment as an Article 22 collector through submission of a form stating, amongst others, the business conducted and the level of activity. The DGT will then review and determine if the applicant will be appointed as an Article 22 collector.

WHAT IS THE RATE OF ARTICLE 22 TAX AND WHAT IS THE TAX OBJECT?

The Article 22 rate is 0.5%. This is imposed on the gross turnover earned by the domestic trader from transactions conducted through the appointed e-commerce marketplace, excluding VAT and Luxury Goods Sales Tax (PPN BM). “Gross turnover” is before deducting discounts or similar.

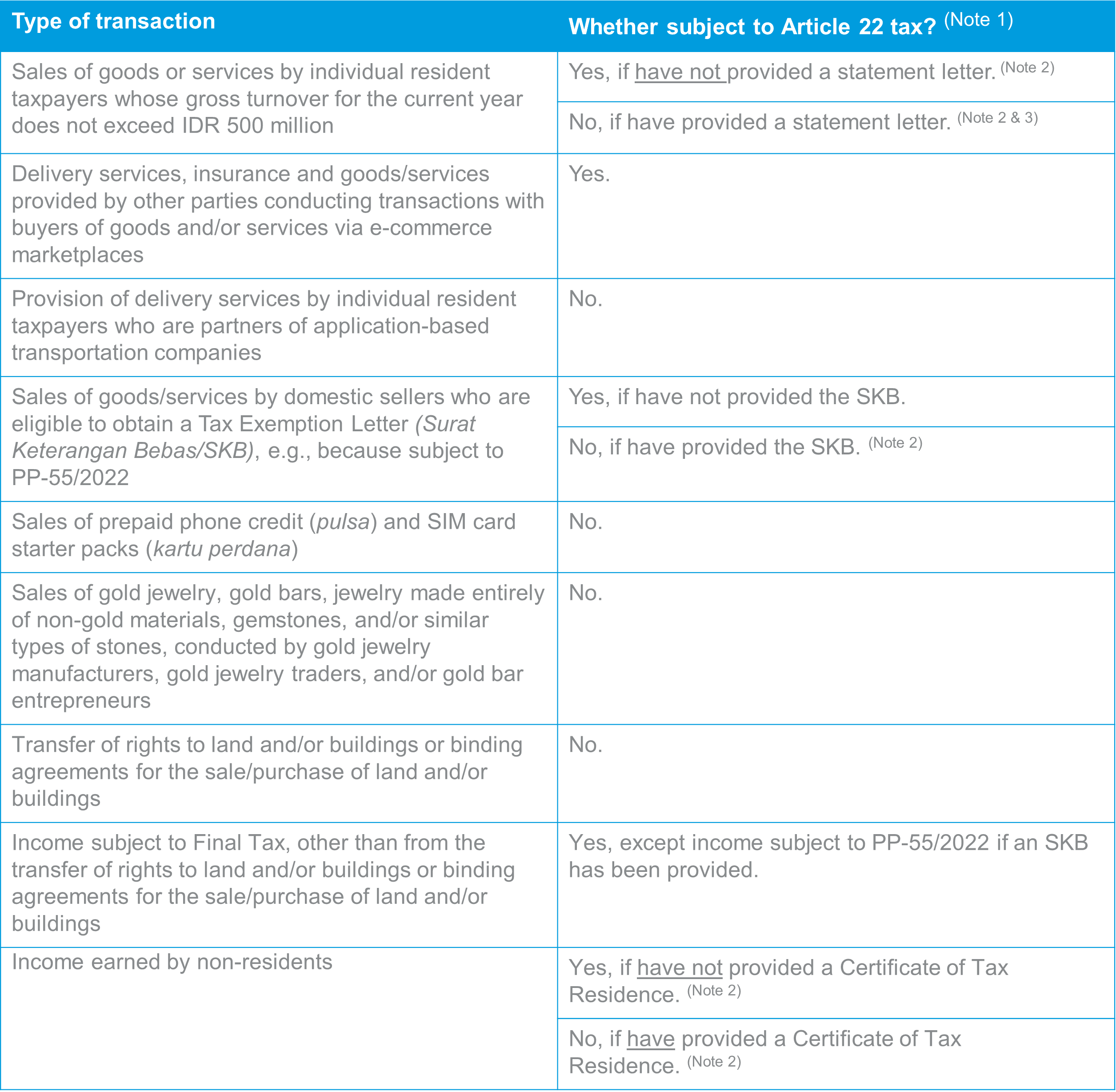

The table below summarizes the types of transactions conducted through an appointed e-commerce marketplace (commencing the month after the marketplace has been appointed) that are subject to Article 22 tax, or are not subject to Article 22 tax:

For certain transactions the tax object might include other amounts and/or there could be more than one tax subject:

Third party delivery charges (unless not subject to Article 22 tax per above table) and insurance costs borne by the seller that are charged through the marketplace are not deducted from gross turnover to determine the amount subject to Article 22 tax.

Further, these costs are subject to separate Article 22 tax collection – on the total (for the main trader) and, as applicable, the delivery provider and the insurer.

Own delivery charges (kurir toko) are added to the gross turnover to determine the amount subject to Article 22 tax.

IMPLICATIONS FOR DOMESTIC TRADERS SUBJECT TO FINAL TAX

With the exception of income from the transfer of titles over land/buildings or from the transfer of binding buy sell agreements over land/buildings, and income subject to PP-55/2022 (provided an SKB is provided), other final taxed income earned through appointed e-commerce marketplaces is subject to Article 22 tax.

If the tax collected is less than the amount due under the relevant final tax regime (e.g., 10% for income earned from land/building rental) then the domestic trader is required to self-withhold, pay and report the balance in the monthly tax return for the month of the transaction.

If the tax collected exceeds the amount due under the relevant tax regime, then the taxpayer may submit a request for refund of taxes withheld that were not due.

INCOME TAX CREDIT

If the income is not subject to Final Tax, the Article 22 tax collected by the marketplace (as evidenced by the invoice issued through the e-commerce marketplace) may be used as an income tax credit to be deducted against gross Article 29 income tax payable at year-end.

1The implementing regulation is DGT Regulation No. PER-12/PJ/2025 dated 22 May 2025 concerning “Thresholds for Other Parties and the Appointment of Other Parties, Collection, Deposit, and Reporting of VAT on the utilization of Intangible Goods and/or Taxable Services from outside the Customs Areas within the Customs Area through Electronic Commerce in the Framework of implementing the Core Tax Administration System”.

Note 1: Transactions not subject to Article 22 tax under PMK-37 are subject to taxation in accordance with the general prevailing tax regulations.

Note 2: Notifications/documents must be provided to the e-commerce marketplace before the transactions occur. The e-commerce marketplace is permitted to determine the procedures for reporting. If the relevant condition exists in the following year, then these documents must be

re-submitted at the beginning of that year.

Note 3: If the individual’s gross turnover exceeds IDR 500 million then that individual must advise the e-commerce marketplace no later than the end of the month when the turnover exceeds IDR 500 million.