RSM Indonesia Client Alert – 17 June 2026

On 4 May 2026, the Director General of Taxes (DGT) issued DGT Regulation No. PER-6/PJ/2026 concerning “The Procedures for Exercising Rights and Fulfilling Obligations under Global Minimum Tax” (GMT) (PER-6). PER-6 is the implementing regulation for Minister of Finance Regulation No 136 of 2024 (PMK-136) that imposes in Indonesia the Global Anti-Base Erosion (GloBE) Rules developed by the OECD/G20 (please refer our Client Alert on 30 January 2025 for details).

WHEN DOES IT APPLY?

It is applicable on 4 May 2026.

KEY POINTS

- A new operational layer is now in force. PER-6 supplements PMK-136 with detailed procedures for registration, tax returns, GloBE Information Returns (GIR), notification requirements, payment, post-filing adjustments, supervision, and audit.

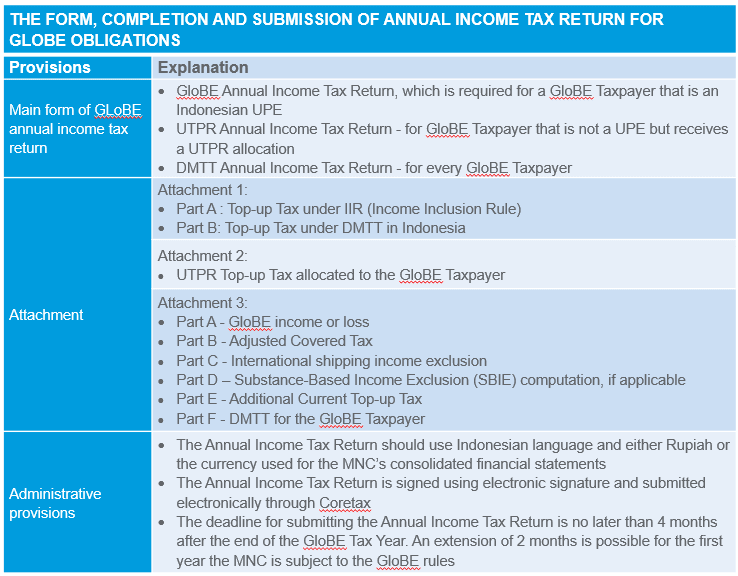

- Three return types. The format for the annual GMT return package is now available. It consists of the (1) GloBE Annual Income Tax Return for Indonesian Ultimate Parent Entities (UPE), (2) DMTT (Domestic Minimum Top-Up Tax) Annual Income Tax Return for every Indonesian Constituent Entity (CE), and (3) UTPR (Undertaxed Payment Rule) Annual Income Tax Return (where UTPR is allocated to the entity).

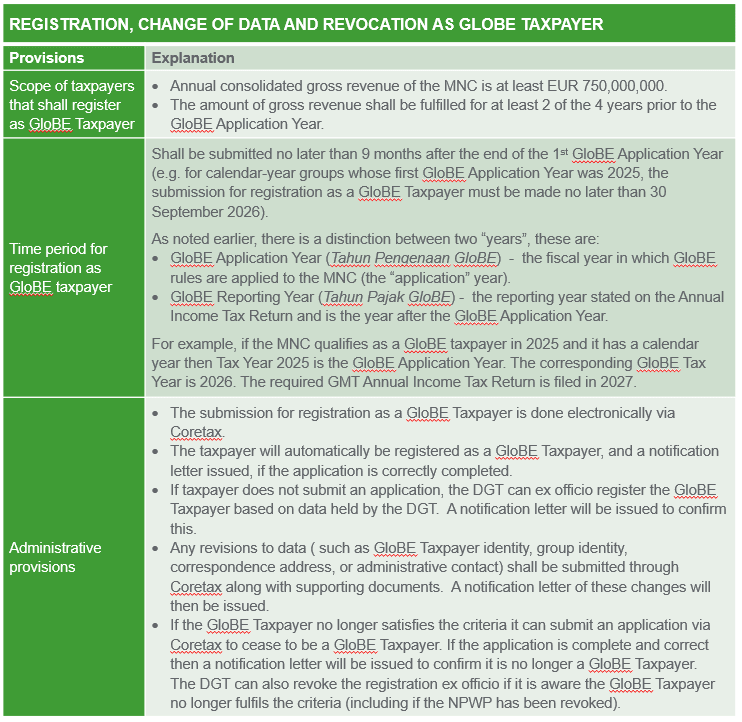

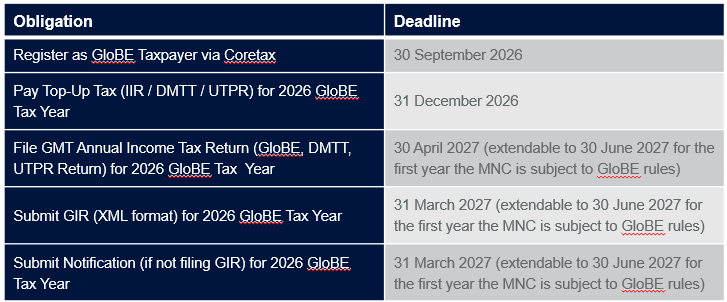

- First registration deadline. Groups must register as a GloBE Taxpayer within nine months after the end of the first GloBE Application Year. The GloBE Application Year (Tahun Pengenaan GloBE) is the fiscal year in which the GloBE rules apply to the Multinational Corporation Group (MNC). For calendar-year groups whose first GloBE Application Year was 2025, the deadline is 30 September 2026.

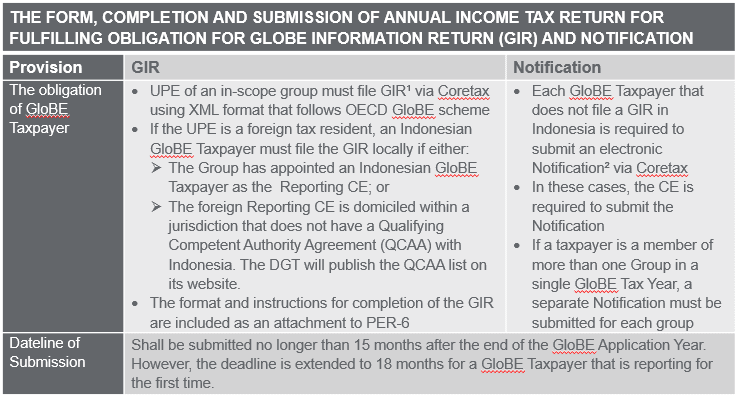

- GIR submission is in OECD XML format, with the deadline no later than 18 months after the end of the first GloBE Application Year. The deadline reduces to 15 months for subsequent GloBE Application Years. For first-time filers for the year ended 31 December 2025, the GIR is due by 30 June 2027.

- Top-up tax must be paid before the Annual Income Tax Return is filed. Payment is due no later than the end of the GloBE Tax Year (Tahun Pajak GloBE). The GloBE Tax Year is the reporting year stated on the Annual Income Tax Return and is defined as the year after the relevant GloBE Application Year. For example, the 2026 GloBE Tax Year and related Annual Income Tax Return are used to report the GloBE Taxpayer’s obligations for the 2025 GloBE Application Year.

- A transitional simplified reporting framework has been introduced - but it is only a simplification for reporting. It is not a safe harbour, and not a substitute for the Transitional CbCR Safe Harbour analysis stipulated by PMK-136.

THE TABLES BELOW SUMMARISE THE MAIN POINTS REGULATED BY PER-6.

TIMING OF PAYMENT OF TOP-UP TAX

Payment of Top-Up Tax under IIR, DMTT, and UTPR must be paid by the end of the GloBE Tax Year. For example, Top-Up Tax for the 2026 GloBE Tax Year must be paid no later than 31 December 2026.

OTHER SIGNIFICANT PROVISIONS:

- Currency Election

Annual Income Tax Return shall use Rupiah or the currency used in the Consolidated Financial Statements. However, if several GloBE Taxpayers within a Group use different currencies for book-keeping, the Group shall make a election (for 5 years) to use either Rupiah or the currency of the consolidated financial statements for the purposes of calculating Top-Up Tax.

- Transitional Simplified Reporting Framework

(1) Where a jurisdiction either has no Top-Up Tax liability or has Top-Up Tax that does not require entity-level allocation, the Constituent Reporting Entity can make adjustments to the financial accounting net profit or loss in aggregate for each country or jurisdiction.

(2) The Simplified Reporting Framework applies to the GloBE Application Year that starts on or before 31 December 2028. It is no longer applicable for GloBE Application Years ending after 30 June 2030.

(3) Simplified Jurisdictional Reporting Framework does not restrict the DGT from requesting additional information/data from the GloBE Taxpayer including information on each CE.

(4)The Simplified Reporting Framework does not eliminate any substantive Top-Up Tax. It is distinct from the Transitional CbCR Safe Harbour, which is a substantive Effective Tax Rate (ETR) test.

Post-filing adjustments

If a covered tax for a GloBE Application Year is later adjusted, the treatment depends on the direction and materiality of the adjustment:

- Increases in covered tax are treated as adjustments in the GloBE Application Year when the adjustment occurs.

- Decreases in covered tax require a recalculation of ETR and Top-Up Tax in the GloBE Application Year when the decrease occurs, applying the Additional Current Top-Up Tax rules.

- However, if the decrease is less than EUR 1 million per jurisdiction then the taxpayer can elect to treat as a decrease in adjusted covered tax for the GloBE Application Year in which the adjustment is made.

AUDIT AND DISPUTES

The DGT may conduct audits to test compliance of the taxpayer’s GloBE tax obligations and for other purposes in terms of the implementation of GMT provisions.

The audits and any disputes arising from these are subject to the provisions of the Law on General Provisions and Procedures of Taxation (KUP).

COMPLIANCE CALENDAR FOR THE FIRST YEAR (FOR CALENDAR YEAR GROUPS)

For an MNC Group whose first GloBE Application Year is Tax Year of 2025 (1 January -

31 December 2025):

RSM COMMENTS

PER-6 turns Pillar Two into an operational regime in Indonesia. Our observations for in-scope groups:

- The compliance burden is bigger than groups expect. The GMT Annual Income Tax Return is detailed, data-heavy, and must be filed even when no Top-up Tax is payable. For in-scope MNEs, it is comparable to preparing an additional corporate income tax return annually.

- The data demands are cross-functional and entity-level. GloBE income, covered taxes, deferred tax movements, SBIE inputs (tangible asset carrying value, payroll), and ownership interests are all required across the consolidated group. This is not something a tax department can deliver alone.

- DMTT is where Indonesian exposure will crystallise. Tax holidays, tax allowances, and final-taxed income reduce the Indonesian ETR without reducing GloBE income, so a top-up is likely. Indonesian groups benefiting materially from these incentives should calculate their exposure early.

- The QCAA list is one of the most important documents to track. It determines whether the Indonesian CE must file a GIR locally, or whether the DGT receives it through automatic exchange of information from a foreign tax authority. The list will be published on the DGT website.

- Scoping and Safe Harbour eligibility need early attention. The EUR 750 million threshold requires a clean look at the UPE's Consolidated Financial Statements over the four preceding years. The Transitional CbCR Safe Harbour, still the most efficient route to administrative relief, only applies where the group has a Qualified CbCR built on Qualified Financial Statements, applied consistently across constituent entities.

- Financial Statement disclosure obligations are already in force. PSAK 212 applies to FY 2025 reporting periods. Groups that have not separately disclosed Pillar Two tax impacts should revisit the position before the next reporting cycle.

- The compliance calendar is non-negotiable. Registration, payment, annual income tax return filing, GIR, and Notification each have separate deadlines. Missing any of them carries administrative consequences under Indonesian tax law.

HOW RSM INDONESIA CAN HELP

RSM Indonesia advises Indonesian and multinational groups across the full GMT compliance lifecycle:

- Pillar Two scoping and impact assessment - threshold testing, constituent entity mapping, exposure modelling.

- Transitional CbCR Safe Harbour analysis - including Qualified CbCR validation and preparation of CbCR aligned with the GMT Standard.

- DMTT, IIR, and UTPR computation - using consolidated and entity-level data, with full reconciliation to the GloBE schema.

- GIR, Notification, and GMT Annual Income Tax Return preparation - including XML lodgement support.

- Financial statement disclosure support - PSAK 212 compliance.

- Cross-border coordination - with RSM offices globally and with the group's existing advisors and auditors.

- Tax holiday and incentive interaction analysis - for groups currently enjoying or planning incentive-based regimes.

- Audit and dispute readiness - including documentation aligned with the DGT's supervisory and audit powers under PER-6.