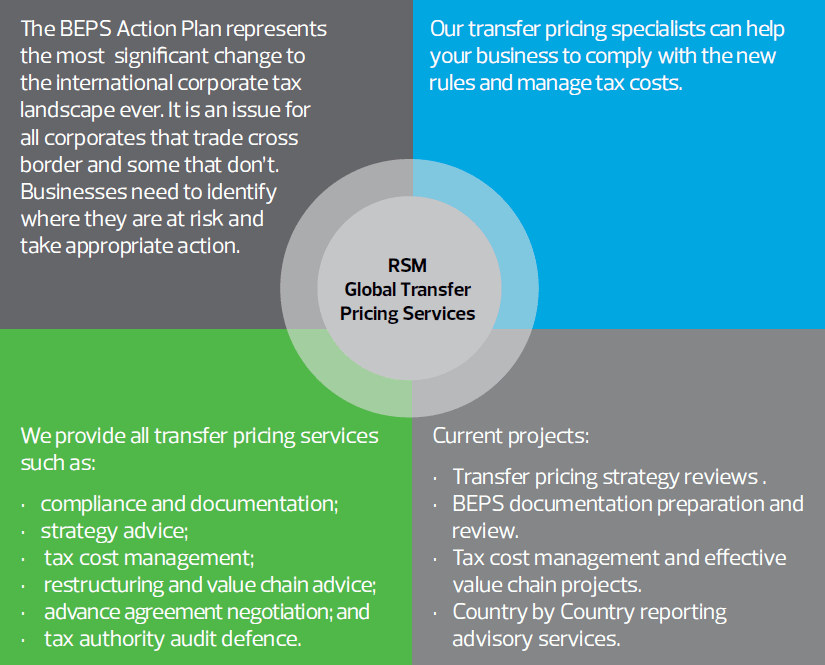

What is Transfer Pricing?

Transfer pricing is about the pricing of a related party's transactions. The OECD examined transfer pricing as part of their Base Erosion and Profit Shifting (BEPS) project. The OECD decided to retain the arm’s length principle, which means that related parties should transact with each other as if they were not related. But the arm’s length principle must work harder to ensure profits are aligned with the value created through underlying economic activities.

Evaluating transfer pricing approaches can open opportunities to review the way profits arise in different entities. Sometimes, getting this right will result in tax savings. Robust transfer pricing isn’t just about risk management and compliance. It is also about commercially-focused planning and proactive tax management.Countries around the world are incorporating OECD transfer pricing principles into domestic law.

Countries around the world are incorporating OECD transfer pricing principles into domestic law. The post-BEPS OECD guidelines should be considered to be the required approach. The basic rule, the arm’s length principle, is not new but it needs to be applied in a BEPS-compliant way:

- Documentation rules are now more prescriptive.

- Global coherence is expected; it is no longer enough to just consider the impact in one country and not others.

- Public disclosure of international tax information is the subject of ongoing debate.

- Reputational damage is a concern for many businesses.

Why should you pay attention?

Should your business be concerned about Tranfer Pricing?

The basics:

- Any businesses with overseas operations eg foreign head office, foreign subsidiary company, foreign branch, should be thinking about transfer pricing.

- There needs to be an element of common control. Control is defined differently depending on the territory.

- Transfer pricing can effect domestic transactions as well as cross border transactions.

- Small as well as medium and large sized taxpayers may be within the rules.

Typical transactions to look for:

- Sales and purchases of raw materials or goods to and from a related party.

- Management fees and head office charges (or the absence of them).

- Royalties and license fees (or the absence of them).

- Loans to or from related parties and interest charges (or the absence of them).

- Business restructures or any changes to the way business is undertaken