While discussions in the Swiss Parliament are underway to make the payment of contributions even more attractive or more flexible over time, or even to increase the maximum deductible limits, RSM offers you a selection of frequently asked questions related to this tool of Swiss pension provision system.

1. 3rd pillar A and B: what is and what are the conditions to withdraw a 3rd pillar A?

The third pillar is a private and individual means that workers can use to compensate for the part of their income not covered by the first two pillars (AHV/IV, LPP) in their future retirement. This scheme is also protected by the law and offers tax benefits. It generally takes the form of a retirement savings account (3rd pillar A) or a flexible savings account such as a life insurance (3rd pillar B). They can be made with a pension fund or with a bank (3rd pillar A). Only taxpayers who are employed or self-employed and subject to AHV/IV contributions (death and invalidity risks) in Switzerland can open a 3rd pillar A.

2. Are there different types of 3rd pillar A?

Yes, there are two types:

- 3rd pillar A in a bank :

- Flexibility of contributions (amounts and timing)

- In case of early withdrawal of capital, no penalty is fixed (except the related taxation)

- A bank 3rd pillar is similar to a classic savings account with the main advantage of being able to deduct the paid contributions for tax purposes.

- 3rd pillar A in insurance :

- Fixed amount of contributions defined in advance and to be paid on the due dates (monthly, quarterly, half-yearly or annually).

- In the event of early withdrawal of capital, a penalty is fixed, the amount depends on the pension fund concerned

3. What is the maximum tax deduction in 2022?

- For taxpayers insured under the 2nd pillar: CHF 6,883

- For self-employed taxpayers who are not insured under the 2nd pillar: CHF 34,416 (provided that the maximum of 20% of their income is not exceeded)

4. How many 3rd pillar A accounts can a taxpayer have?

No limitation is mentioned in the law. However, since having several 3rd pillar A accounts allows the withdrawal of capital to be staggered (keeping in mind that a 3rd pillar A account can be paid out 5 years before the ordinary retirement age) and therefore reduces taxes, some of cantons limit the number of 3rd pillar A available before having its retirement.

5. Is it possible to early withdraw the capital accumulated in a 3rd pillar A ?

Yes, the capital can be withdrawn early before retirement age under certain conditions. A cash payment is only possible in the following cases (subject to the consent of the spouse/registered partner):

- At the earliest 5 years before the AHV retirement age or, in the case of continued employment, at the latest 5 years after the AHV retirement age

- If you receive a full invalidity pension (IV), if the risk of invalidity is not insured

- When transferring to another recognised form of pension scheme

- If you start a self-employed activity or change your self-employed activity (at the latest in the year following the start of the activity)

- Within the framework of the promotion of home ownership (main residence): acquisition, construction, repayment of mortgage loans.

Thus, it is not possible to request the cash payment of the capital to buy a car or other goods other than a main residence. For the promotion of home ownership, certain additional conditions apply if the taxpayer is over 50 years old. Furthermore, an advance payment in the context of the promotion of home ownership from a 3rd pillar A is definitive: it cannot be repaid in the future, in order to regain the amount of the capital before the advance payment. In this respect, the Swiss Federal Court has ruled that a payment in the context of the promotion of home ownership to repay the mortgage debt, followed shortly thereafter by an increase in the mortgage debt, entails a duty to repay the promotion of home ownership payment. If repayment is not possible, the taxable benefit would be added to the taxpayer's taxable income and would therefore not be taxed separately and, above all, preferentially.

Finally, it is possible to pledge (collateral) a 3rd pillar A, as it is also possible for the 2nd pillar.

6. Who will be the beneficiaries of the capital from the 3rd Pillar A contributions?

In the event of the client's survival: the client. However, if the client dies before the withdrawal of his 3rd pillar A, it is important to know that the order of beneficiaries is, by default, defined as follows by the law:

(i) the surviving spouse or the surviving registered partner, then (ii) the direct descendants as well as the persons for whose maintenance the deceased provided substantially, or the person who had formed an uninterrupted community of life with him or her for at least five years immediately prior to the death or who must provide for the maintenance of one or more common children, (iii) the parents, (iv) the brothers and sisters and finally (v) the other heirs.

However, the policyholder has the right to change the order of beneficiaries as indicated above and to specify their rights. Generally, a form is available for this purpose which must be duly completed and sent to the pension fund or the bank managing the 3rd pillar A in question. It should be noted that all benefits from pension schemes (2nd pillar and 3rd pillar A) are taxable as income only, regardless of the reason for their payment.

7. Buying back missing contribution years: What is the difference between a 3rd pillar A and a 2nd pillar?

- 3rd pillar A: The maximum annual contribution is fixed and does not allow for additional contributions. The tax deduction is then limited to the maximum annual contributions. No tax-deductible buyback is currently possible. However, this possibility is currently being debated in Parliament.

- 2nd pillar: It is possible to buyback missing contribution years (contribution gap) retroactively and benefit from a tax deduction for income tax purposes. It is even possible, once these contribution gaps have been fully compensated, that future gaps (e.g. if the taxpayer wants to take early retirement) can be bought back for tax purposes. The conditions and amounts must be discussed with the relevant pension fund.

8. Is it possible to reinvest 2nd pillar retirement assets in a 3rd pillar A?

No, it is not possible to transfer assets this way, as this would mean buying back missing years of contributions, which is not possible under the 3rd pillar A system. As mentioned above, the opposite is possible: a 3A pillar can be used to buy back a contribution gap in the 2nd pillar (up to the maximum amount of the contribution gap).

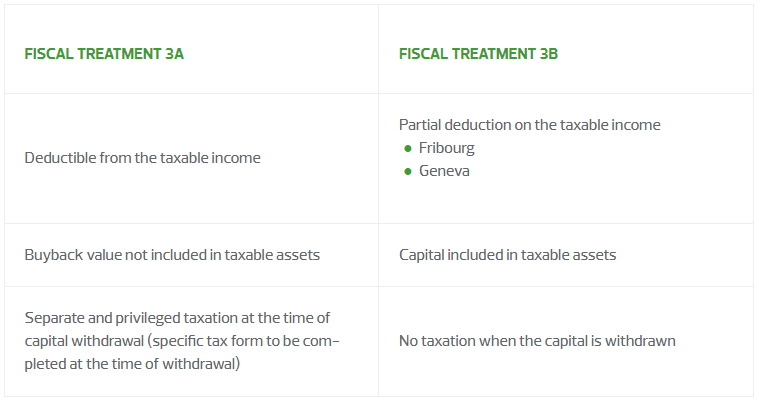

9. What is the difference between a 3rd pillar A and 3rd pillar B?

Main differences:

- 3rd pillar A: The maximum tax-deductible contribution is limited. The capital is blocked in long-term investment plans which are not available before retirement or under certain conditions.

- 3rd Pillar B: is more flexible and does not limit the annual contribution. It is generally used for various purposes such as education, holidays, etc. The capital invested is available at any time. Tax deductions are applicable in some cantons (GE, FR), as is the case for life insurance.

From a fiscal point of view, the differences can be summarised as follows:

10. What is meant by a so-called "cross-border" 3rd pillar

This is a special deduction that is only applicable in the canton of Geneva and Fribourg. With the status of deemed-resident, a cross-border worker is entitled to deduct his or her 3rd pillar since January 1, 2021.

As you can see, there are many things to consider when setting up one or more 3rd pillar A accounts, early withdrawals or planning for the approach of retirement age. The tax team at RSM will be happy to advise and assist you in this regard.