Substance is now a key factor in analysing the tax treatment of cross-border dividends. When a Swiss company pays a dividend to a foreign company, access to the declaration procedure or refund of withholding tax depends on the application of the double taxation agreement (DTA) concluded with the beneficiary's country of residence.

However, these treaty benefits are only granted if the recipient company has a real economic existence and has not been set up primarily to obtain a more favourable treaty rate. For this reason, the FTA now systematically examines the substance of foreign companies.

Substance: what are we talking about?

The substance corresponds to the economic reality of a company: having real activities, its own resources (staff, offices, functions) and an effective role within the group. In other words, a company that exists in reality, and not just for tax purposes.

What are the criteria?

A foreign company receiving dividends may demonstrate its substance by means of three alternative criteria:

- Personal substance: presence of staff and premises.

- Functional substance: holding of other substantial participations abroad (international holding company function).

- Balance sheet substance: sufficient level of self-financing (at least 30%).

In most cases, a single criterion is sufficient to demonstrate economic reality.

Why do we check the substance?

The SFTA seeks to prevent two forms of abuse:

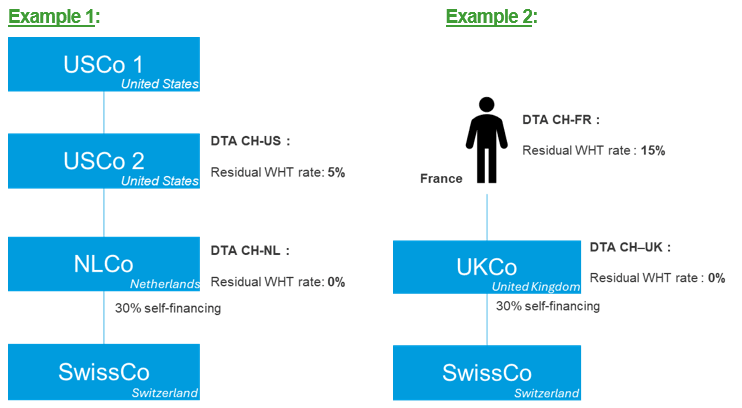

- “Treaty shopping”: interposing a company in a country whose DTA offers a better rate than that applicable to the indirect shareholder (Example 1).

- “Rule shopping”: using an intermediary company to benefit from the rate reserved for legal entities (e.g., 0–5%) when a natural person would only be entitled to a conventionally higher rate (generally 15%) (Example 2).

These situations are not abusive as long as the intermediary company has sufficient substance.

How many substance criteria must be met?

The SFTA requires two criteria only in situations presenting an increased risk of abuse

Two criteria are required when the indirect shareholder cannot invoke the DTA (qualified treaty shopping), in particular:

- when there is no DTA with their country of residence (e.g., Monaco, Bermuda);

- or when a DTA exists, but the indirect shareholder cannot benefit from resident status within the meaning of the agreement.

In these cases, the interposition of a corporation provides an advantage that the indirect shareholder could never have obtained through direct ownership, which justifies two substance criteria.

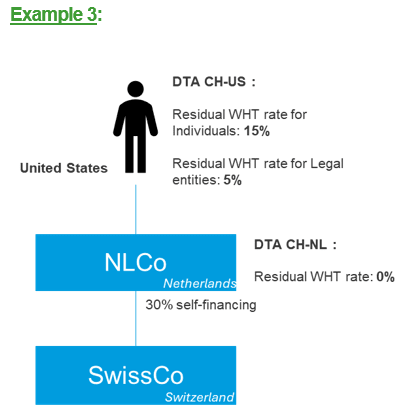

Two criteria are also required when the interposition creates a double advantage (Example 3), namely:

- an advantage linked to the status of the company (access to the rate applicable to legal entities) (rule shopping effect); and

- an advantage linked to a more favorable DTA than that applicable to, or inaccessible to, the indirect shareholder (treaty shopping effect).

In all other cases: a single criterion of substance is normally sufficient.

What are the risks of non-compliance?

If the substance is deemed insufficient, the SFTA may refuse:

- the declaration procedure,

- the refund of withholding tax.

This can result in double taxation and significant tax costs for the group.

How can you prepare for this?

Groups must analyse their chains of participation and dividend flows, document the actual role of their foreign companies, and verify that they have substance consistent with their function. Adequate preparation ensures the secure application of DTAs and limits risks during SFTA audits.

Our team is here to help

Do you have questions about the substance of your companies? Would you like to secure your dividend flows or obtain a diagnosis?

Our Corporate Tax & Private Client Services team is available to assist you.