As of 1 January 2026, the Swiss Federal Tax Administration (SFTA) has updated and published several parameters relevant for practice:

Interest rates (fiscal year 2026)

- Credit interest (voluntary advance tax payments): 0.0% (2025: 0.75%)

- Default / refund interest: 4.0% (2025: 4.5%)

- Notional interest rate on excess equity: 0.333% (2025: 0.317%)

This STAF deduction can currently only be applied in the Canton of Zurich.

Tax Deductions / Parameters (fiscal year 2026)

- Pillar 3a (maximum deduction / contribution limit): CHF 7,258 (with 2nd pillar) / CHF 36,288 (without 2nd pillar) – unchanged from 2025

- Lump sum taxation (minimum taxable amount): CHF 435,000 (2025: CHF 434,700)

- Tax exempt threshold for certain lottery winnings (Art. 24 DFTA): CHF 1,071,000 (2025: CHF 1,070,400)

Exchange rate lists / currency rates for 2025

The SFTA has updated the exchange rate lists and the lists of bonus shares for 2025.

These are now available on ICTax (year end exchange rates as of 31 December 2025 and annual average rates).

Pillar 3a – Retroactive Contributions

Starting in 2026, missing contributions to Pillar 3a can be made retroactively for up to 10 years. This rule applies to individuals gainfully employed in Switzerland with income subject to AHV contributions who did not fully utilize the maximum Pillar 3a contribution in previous years and who have not yet received any retirement benefits.

Retroactive contributions can be made for the first time in the 2026 fiscal year, covering contribution gaps from 2025 onwards. The regular annual Pillar 3a maximum contribution for the current year must be paid first before earlier gaps can be filled.

Capitalization Rate (valuation of securities without market value)

- As of 31 December 2024 (valuation year 2024): 8.75%

- As of 31 December 2025 (valuation year 2025): 10.00%

Implication: A higher capitalization rate leads, ceteris paribus, to a lower capitalized earnings value.

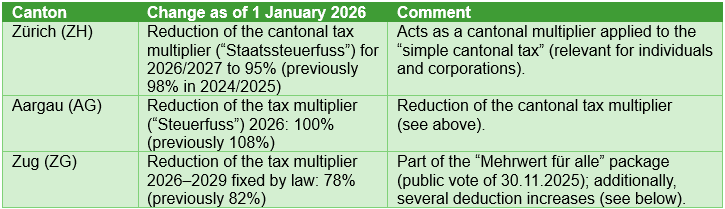

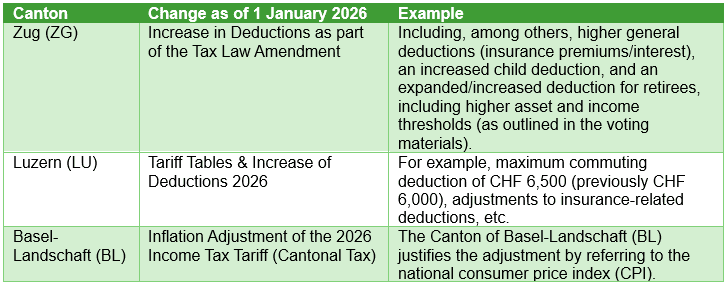

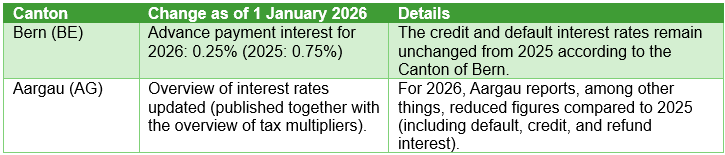

Selected Cantonal Changes

Below are some important cantonal changes effective as of 1 January 2026.

Tariffs and Deductions for Individuals (Cantonal)

Interest Rates (Cantonal Taxes)

Other cantonal taxes

Withholding Tax (implemented at cantonal level, updated nationwide)

The withholding tax tariffs for 2026 have been fully updated and published.

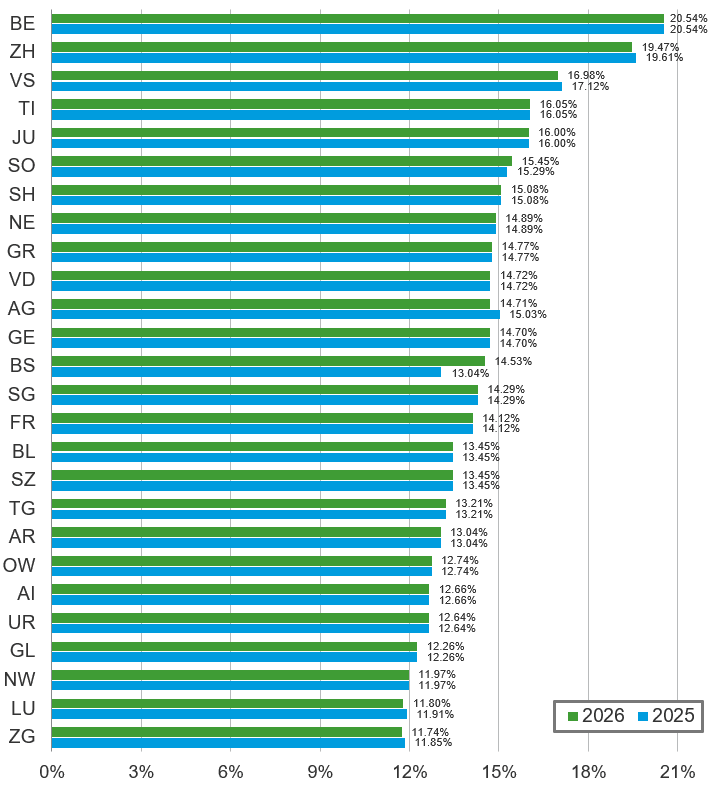

Canton Overview of Effective Tax Rates by Canton

Methodology: The effective tax rate refers to the taxation of corporate profits at the capital city of the respective canton. The rate includes federal, cantonal, and municipal taxes and is calculated based on profit before taxes. If multiple tiered tax rates are published, the highest applicable rate was used. All calculations and information are provided without guarantee. Cantons may adjust tax rates and tax multipliers at any time.