As financial advisers, we talk to our clients a lot about risk, one key risk for a long-term financial plan is sequencing risk. But what is sequencing risk?

Let’s start with an example…

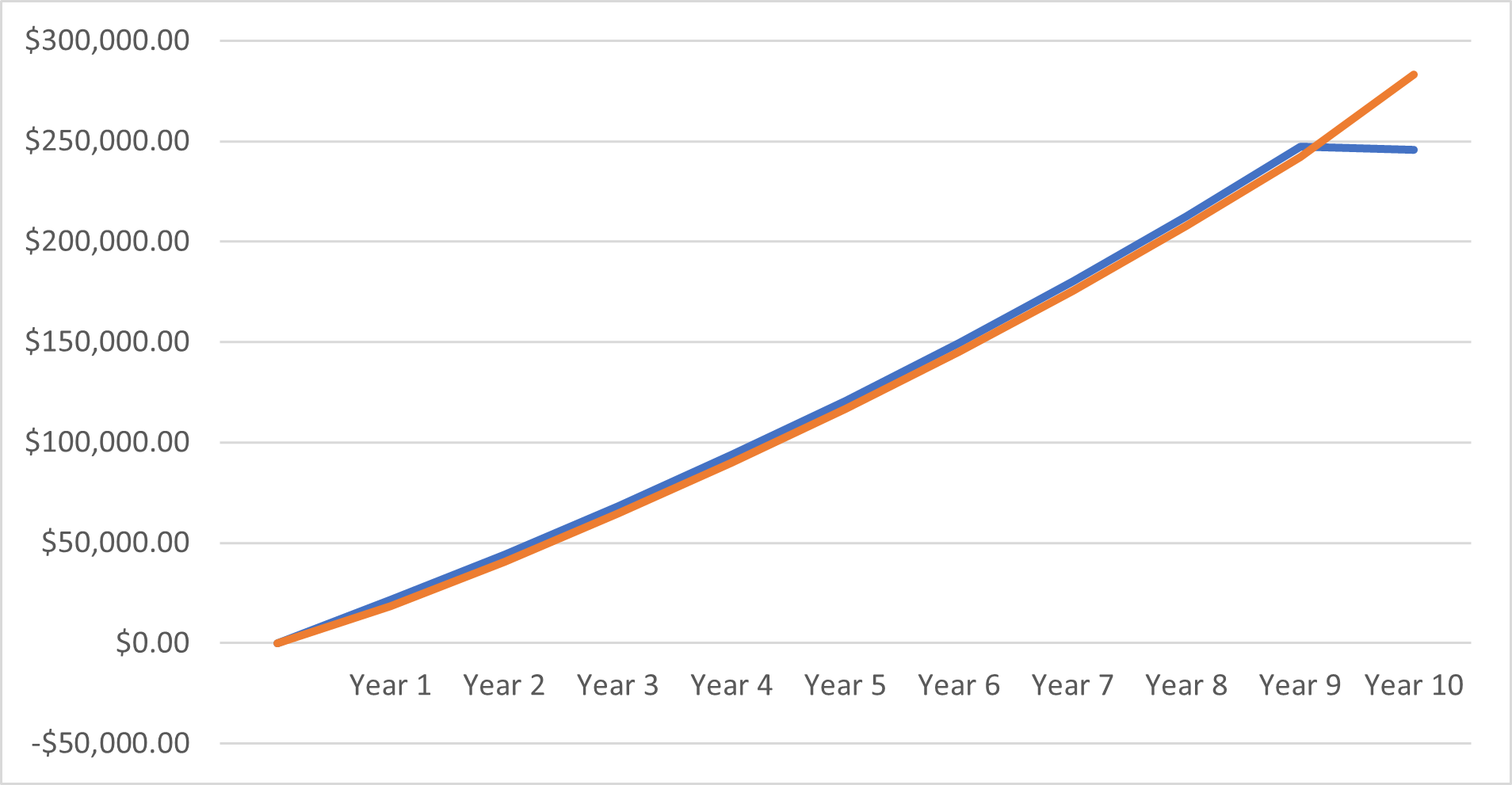

Wayne and Chris each contribute $20,000 per year to their superannuation funds for 10 years. They both earn an average return of 5% per annum, after tax and fees, and from years 2 to 9 they earn identical returns each year. The only difference is that Wayne’s portfolio returns 8% in the first year and -8% in the last year; whereas Chris’s returns are -8% in year 1, and 8% in year 10. This doesn’t seem like much of a change, yet Chris ends up with a balance of $283,071 compared to Wayne’s $245,9161. That’s a substantial difference of $37,155 or 13% less.

This simple example demonstrates that it isn’t just the average of annual returns that matter; of equal importance is the sequence in which those returns occur. Not surprisingly this is called sequencing risk.

The sequence of returns isn’t an issue with a lump sum investment. It’s only of concern when regular contributions and withdrawals are being made. And in the drawdown phase, such as in retirement, positions are reversed.

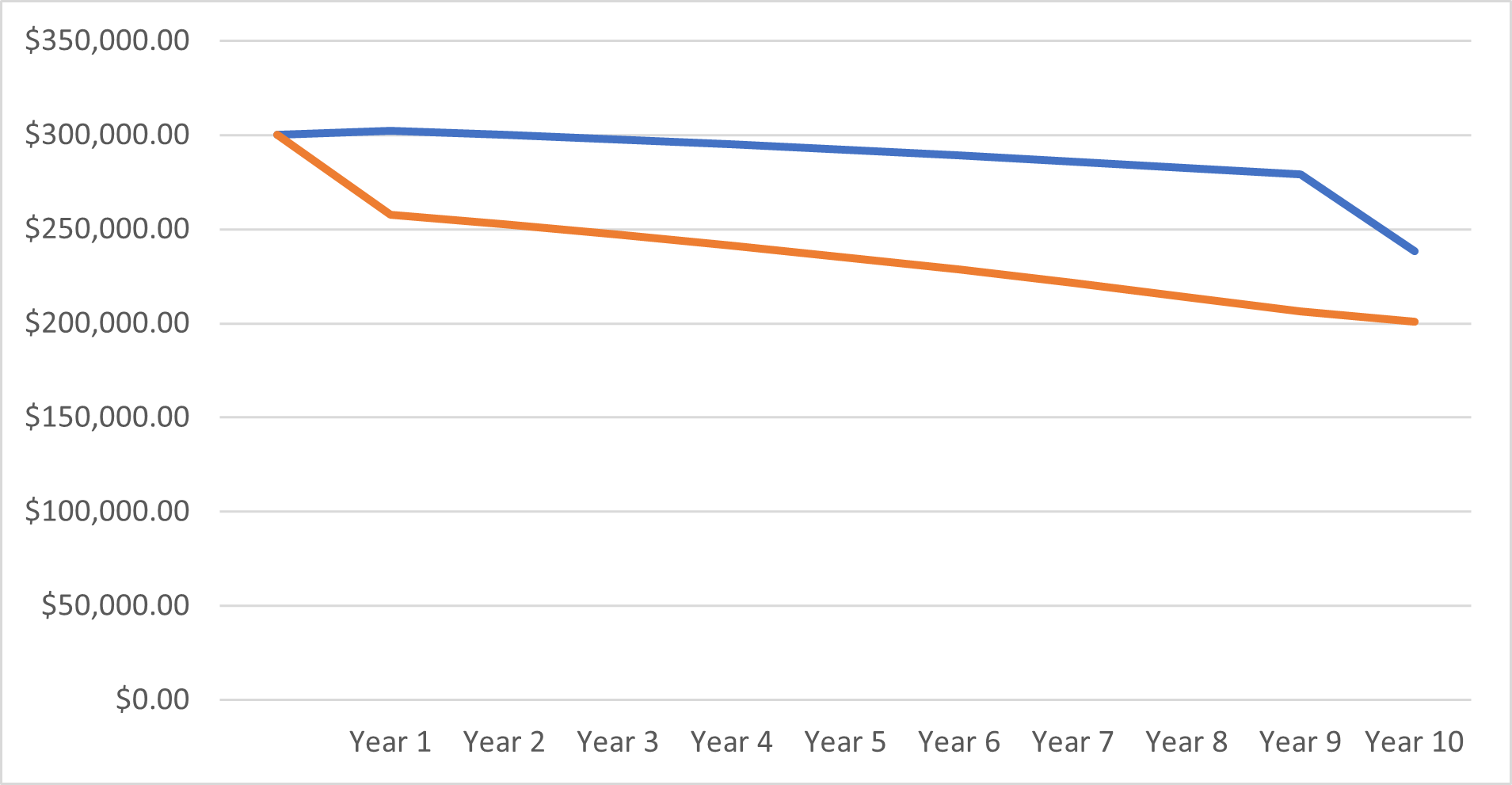

Imagine that Wayne and Chris both invest the same lump sum into a pension and withdraw $20,000 each year. If they each experience the same sequence of returns as in the first example, this time Wayne is better off by $37,145 after 10 years.

Dealing with the real world

This may make it appear that with sequencing risk, what you lose on the way in, you gain on the way out, but history is unlikely to repeat itself exactly. What is clear is that:

- Poor portfolio performance at the end of an accumulation phase can be more damaging than poor performance at the start.

- In the drawdown phase, good returns later in life may not make up for a poor start.

Both points suggest that risk should be reduced well ahead of retirement. A few key points to consider:

- Don’t carry any more risk than is necessary.

During the accumulation phase, if you reach a point where your savings will allow you to meet your needs with a more conservative investment portfolio, consider whether it’s appropriate to dial down the risk. - Start early.

The sooner you start and the more you are able to save in the early years of preparing for your retirement, the sooner you will be able to reduce your exposure to sequencing risk. - Build a cash reserve.

Aim to have two to three years’ worth of pension payments in the cash component of your superannuation savings by the time you retire. This can reduce the need to sell shares or property during any market downturns.

Achieving the right balance

Reducing sequencing risk usually involves allocating a larger proportion of the investment portfolio to cash and fixed interest.

The potential downside of this option is increasing longevity risk, that is, the risk of outliving your savings due to the lower returns. If sequencing risk catches you out, the alternatives may be to work longer or reduce your retirement living standards, neither of which may be all that palatable.

Investment risk management is a fine balancing act. The right strategy depends very much on individual circumstances. An RSM adviser will be able to assess your situation and develop a risk management strategy that’s right for you.

1 Results vary significantly depending on specific annual returns.

For more information

If you require further information on sequencing risk, please reach out to your local RSM financial adviser.

This page has been prepared by RSM Financial Services Australia Pty Ltd ABN 22 009 176 354, AFS Licence No. 238282.

As everyone's circumstances are different and this article doesn't take into account your personal situation, it is important that you consider the above in light of your financial situation, needs and objectives, and seek financial advice before implementing a strategy.

View the Financial Services Privacy Statement and Policy, Complaints Policy and Financial Services Guide