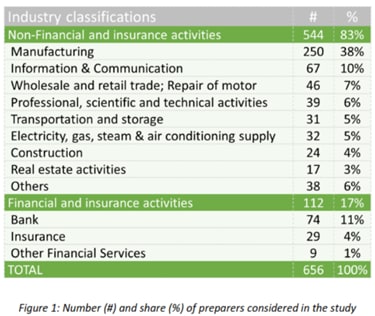

At the end of July 2025, EFRAG published its “State of Play” report, analysing sustainability reporting practices by listed entities that applied the ESRS standards for the first time on FY 2024.

The analysis was performed by EFRAG on 656 sustainability reports, highlighting key observations on both cross-cutting and topical standards across the following sectors:

1. Observations related to cross-cutting standards

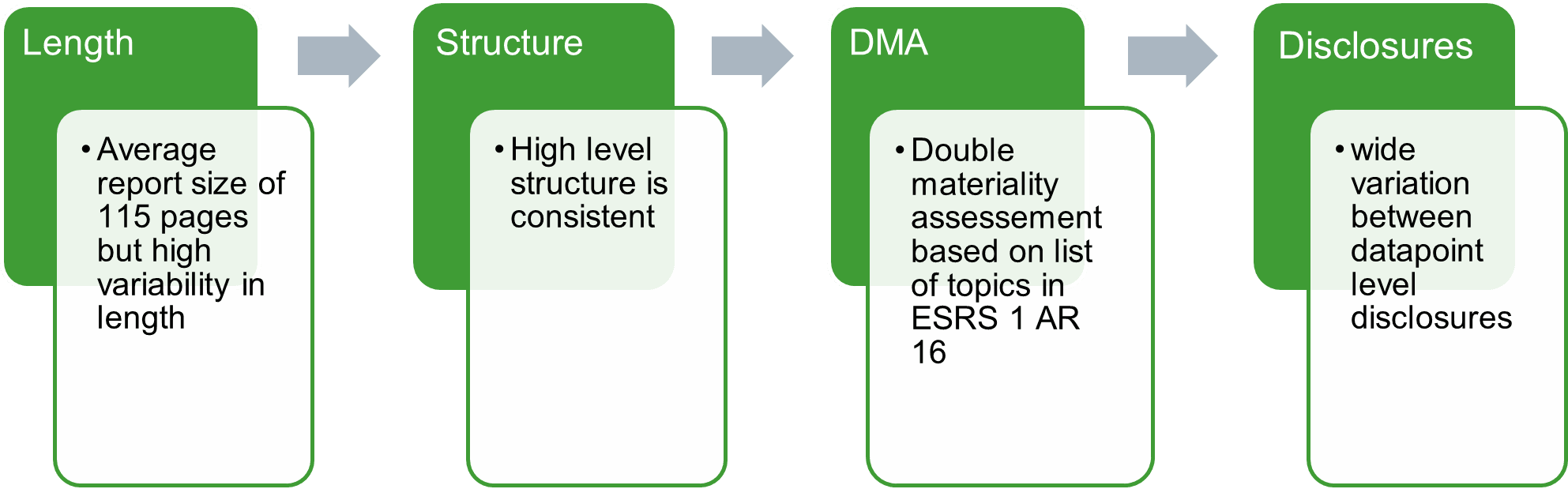

1.1. General report information

1.2. Material topics and Double Materiality Assessment

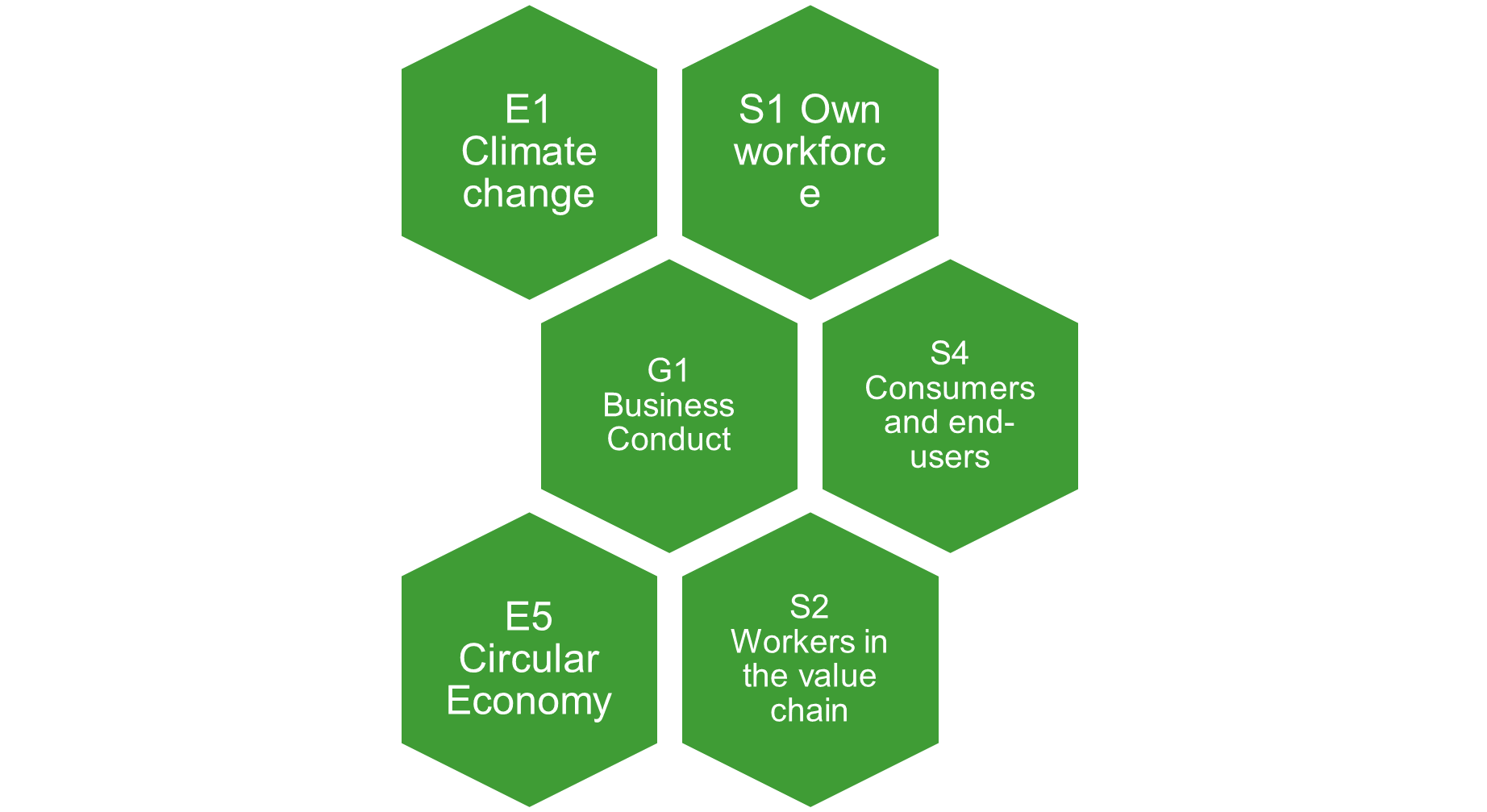

About 10% of reporters considered all 10 topical standards as material while about 25% considered maximum 4 topics as material.

The 6 following topical standards are most frequently assessed as material for a majority of preparers:

Companies most often consult business related stakeholders such as employees, clients, suppliers, investors while broader societal stakeholders such as communities, trade unions, academia… are consulted less frequently.

Impacts, risks and opportunities (IROs) have been most often identified in the upstream value chain and own operations for non-financial entities, and in the downstream value chain for financial institutions.

2.Observations related to main topical standards

A majority of preparers claim to have a transition plan for climate change mitigation but there is limited standardization of the information disclosed. While a majority of transition plans are compatible with the objectives of the Paris Agreement, only about 40% extend this target to Scope 3emissions.

Only around 30% of preparers report on biodiversity-related metrics, and few datapoints are included in the reports.

About a third of reporters disclose information about severe human rights incidents for workers in the value chain but only 10% of those reported one or more incidents. In own operations, a majority of companies disclosed that no incidents were identified.

These initial findings indicate that while the ESRS framework has already been adopted in a relatively structured manner, significant differences remain in the quality, granularity, and methodologies applied in reporting. This creates challenges for comparability and reliability of disclosures, but also offers an important learning opportunity as companies work to refine and strengthen their reporting practices in the years ahead.

If you would like guidance on how to start preparing a sustainability report that focuses on the most relevant topics, contact one of our experts.