Since the formation of the Arizona government, numerous tax measures have been adopted. This is notably the case with regard to the so-called “DRD” regime (“dividends received deduction”), in particular, through one of the conditions for applying this regime as well as through an investment mechanism benefiting from it, namely DRD SICAVs.

STRENGTHENING OF THE CONDITIONS FOR THE APPLICATION OF THE DIVIDENDS RECEIVED DEDUCTION (DRD) REGIME

Reminder

The DRD regime is a system providing for the exemption from taxation of income distributed by a subsidiary (i.e. dividends) to its parent company. Under certain conditions, the parent company may claim an exemption on these dividends, as they have already been subject to taxation at the level of the distributing subsidiary.

In order to benefit from this regime (and also the exemption for the capital gains on shares), several conditions must be met:

- Participation condition: the company claiming the exemption must hold 10% or more of the shares in the distributing company. However, where this threshold is not met, the exemption may still be claimed if the acquisition value of the shares is equal to or exceeds €2,500,000.

- Holding period condition: the shares must be held for an uninterrupted period of at least one year.

- Taxation condition: to benefit from the regime, the distributing company must not fall within any of the exclusion cases provided for by the legislator. This notably includes a minimum taxation requirement at the level of the subsidiary.

What is changing

The law of 18 July 2025 introduces a change which, although it may appear minor, has significant consequences for companies holding shareholdings below 10% but claiming the DRD or capital gains exemption.

As from assessment year 2026, large companies will only be able to benefit from this regime where the shareholding has the nature of a financial fixed asset (i.e. only where the 10% threshold is not met).

- How should a financial fixed asset be defined?

In order to determine which shareholdings may qualify as financial fixed assets, reference must be made to accounting legislation, which does not, however, provide for a clear-cut definition.

Nevertheless, the Royal Decree implementing the Code of Companies and Associations provides three types of financial fixed assets:

- Shareholdings in affiliated companies: this refers to shareholdings in affiliated companies, i.e. situations covered by article 1:20 of the Code of Companies and Associations (companies over which control is exercised, whether ‘de facto’ or ‘de jure’).

- Shareholdings in companies with which there is a participating interest: this concerns situations other than those mentioned above, where the shareholding is intended to establish a lasting and specific link enabling the exercise of influence over the company’s management.

- Other financial fixed assets: this refers to shareholdings intended to establish a lasting and specific link where such holding aims to support the company’s own activities.

With a view to clarifying this latter category, the tax authorities issued a circular (Circular 2025/C/63 of 03.10.2025) in which they set out certain key criteria for this concept.

In this respect, the notion of a lasting link should be understood to mean that the shares must be held on a long-term basis, i.e. they must not have been acquired with a view to short-term disposal. It cannot therefore be a mere investment objective. The tax authorities specify that an “investment objective” refers to “the mere realization of capital gains or dividends.”

The notion of a specific link is, for its part, defined by the tax authorities as implying a strategic business relationship between the shareholder company and the company whose shares are held.

By way of example, the tax authorities refer to shareholdings acquired with a view to subsequently increasing the participation or in anticipation of a future merger or acquisition, where there is complementarity between the activities or where a technological interest exists.

However, the above should be nuanced. The tax authorities adopt a strict interpretation of the law and maintain a degree of uncertainty.

First, with regard to the temporal aspect of the holding, the notion of “short term” is not defined. Moreover, the circular states that shareholdings may not have an investment objective, meaning that the tax authorities tend to consider that even long-term holdings for investment purposes would not qualify as a lasting link, which appears to be a rather restrictive interpretation of the law.

In addition, the explanatory memorandum indicates that such shareholdings may not be held “exclusively” for investment purposes. On this point, the circular therefore goes further than the explanatory memorandum.

- As regards the company size criteria

In addition to the definition of a financial fixed asset discussed above, particular attention should also be paid to the proper assessment of the company’s size.

Indeed, the size of a company must be assessed on a consolidated basis where it is affiliated with other companies. Beyond the usual situations, such as ‘de facto’ or ‘de jure’ control, it should be recalled that companies are also considered affiliated where they are part of a consortium, namely a situation in which several companies are under central management. This may arise, in particular, where the governing bodies of these companies are composed predominantly of the same individuals.

Note: the manner of decision-making may also be relevant. In a private limited company (SRL/BV) where each director can act independently, it is assumed for the purposes of assessing “central management” that each director is effectively the sole director, regardless of the number of other directors.

Exercise caution with changes to the board within a group of companies. Always first examine the potential consequences for the affiliation and the “size” of the company.

- Withholding tax exemption on outbound dividends ("Tate & Lyle"-provision)

The new qualitative condition also applies to withholding tax exemption on outbound dividends to foreign group entities (see Tate & Lyle case law), potentially limiting cross-border benefits.

Note that the criterion of “financial fixed assets” in Belgian accounting rules is stricter than what is prescribed by the European Accounting Directive. The latter refers to “durability” but not to “specificity,” and it does not require that the shares or units contribute to the shareholder company’s own business activities. Consequently, this could give rise to reverse discrimination, whereby foreign shareholders are treated more favourably than domestic shareholders.

Passive holding company

It should also be recalled that, in all cases, the application of the DRD regime may be denied where an arrangement is considered non-genuine and has as its main purpose the obtaining of a tax advantage. Where the holding company has little or no economic substance, the Belgian tax authorities (and, more broadly, at the European level) are increasingly relying on this specific anti-abuse measure to challenge the benefit of the DRD deduction or an exemption from withholding tax based on the DRD regime. For these holding companies, it is essential to demonstrate their decision-making autonomy and to assess and justify (from a strategic business perspective) its existence within the group structure on a dynamic basis.

Conclusion

For large companies claiming the benefit of the DRD regime, particular attention must now be paid when acquiring shareholdings below 10%, especially where these are acquired for investment purposes. The classification of participations as “financial fixed assets” (taking into account, inter alia, their purpose, duration, specific link, influence on business activities, etc.) could become a delicate point of discussion in the event of a tax audit.

The key takeaway, as is often the case, is proper justification, as well as the supporting evidence that the taxpayer can provide to demonstrate the nature of the shareholding (e.g. strategic memoranda, shareholders’ agreements, business plans, investment or cooperation intentions, etc.).

DRD SICAV

Reminder

A DRD SICAV (investment company with variable capital) allows its shareholders – in practice, companies – to benefit from the DRD regime without having to meet the participation and holding period conditions at their level. This preferential regime is notably subject to the condition that the DRD SICAV distributes at least 90% of its net income annually and that it invests in companies that meet the taxation condition (see above).

Where these conditions are met, the shareholder may exempt the income received from the SICAV based on a DRD coefficient (the latter being communicated by the SICAV on the basis of eligible income).

What is changing

The law of 18 December 2025 introduces significant changes regarding the tax treatment of this regime. These changes apply as from assessment year 2026 (i.e. for financial statements closed on 31 December 2025).

- Application of a separate tax upon exit

The legislator now provides that, in the event of a transfer to a third party, the capital gain realized will be subject to a separate tax of 5% (excluding ‘private privak’’/’pricafs privées’). In practice, however, this tax will apply only rarely. Indeed, upon a transfer of shares in an investment company, the latter generally proceeds with the redemption of its own shares (and their immediate cancellation), an operation that is treated for tax purposes as a dividend.

Finally, two important points should be highlighted. First, this levy will only be due where the DRD regime has previously been applied to its distributed income. Second, this levy will constitute a minimum taxable basis.

- Non-creditability and refundability of withholding tax

The second measure introduced by the legislator regarding DRD SICAVs concerns the non-creditability of withholding tax. Indeed, upon the payment of dividends, withholding tax must be levied at source, which is in principle creditable against corporate income tax (and refundable).

As from assessment year 2026, such credit and refund will only be possible if the minimum remuneration condition is met (i.e. the allocation of remuneration of at least €45,000.00 or the lower taxable result to an individual director – this amount is expected to increase to €50,000.00 and to be indexed annually as from assessment year 2027). This tightening applies not only to DRD SICAVs, but also to regulated real estate companies (RECs / ‘GVV’), (public) PRICAFs, specialised real estate investment funds (SREIFs / ‘GVBF’), European Long-Term Investment Funds (ELTIFs), and their foreign counterparts.

However, the credit will remain available in all cases for start-up SMEs and approved cooperative companies.

Finally, the Minister confirmed in committee that the non-creditability rule for withholding tax only applies where the DRD regime is claimed. Consequently, where the remuneration condition is not met, companies may be advised not to claim the DRD deduction, which would allow them to credit the withholding tax (resulting in a maximum tax burden of 25%).

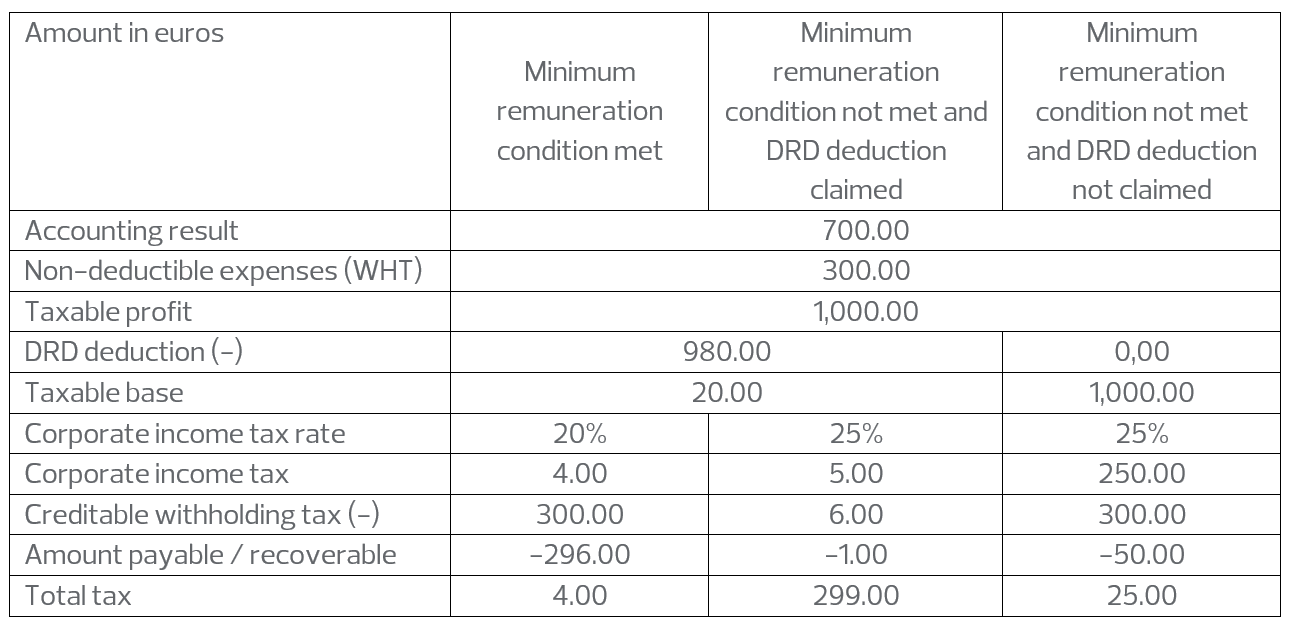

Example

To illustrate this, let us consider the example of a DRD SICAV distributing a dividend of € 1,000.00 with a DRD coefficient of 98%:

The example highlights the negative impact of the introduction of this new measure where the minimum remuneration condition is not met but the benefit of the DRD regime is nevertheless claimed. This results in a significant increase in the overall tax burden. In such situations, it is therefore advisable not to claim the DRD exemption in order to limit the taxation of the dividend to the ordinary corporate income tax rate.

Conclusion

The favourable tax regime of DRD SICAVs remains an attractive option for companies wishing to invest their excess cash. However, particular attention should be paid to complying with the minimum remuneration condition in order to avoid losing the benefits of this regime.

For any questions regarding the above matters, please do not hesitate to contact the RSM Belgium Tax team (tax@rsmbelgium.be).