We are proud to share the IBFD publication: “HNWIs and the Italian Tax System – The Link Between the Flat Tax and the “Impatriate” Regime: Insights from Revenue Ruling 16/2025 signed by GG, DG e GS.

This note address the Italian Revenue Agency acknowledgment of the possibility of combining tax benefits for the same taxpayer under the newly introduced Inbound Workers Regime, as stipulated in article 5 of Legislative Decree 209/2023, alongside the regime for Researchers And Teachers, owing to the absence of any express prohibition against this practice in the recent Tax Ruling 16/2025.

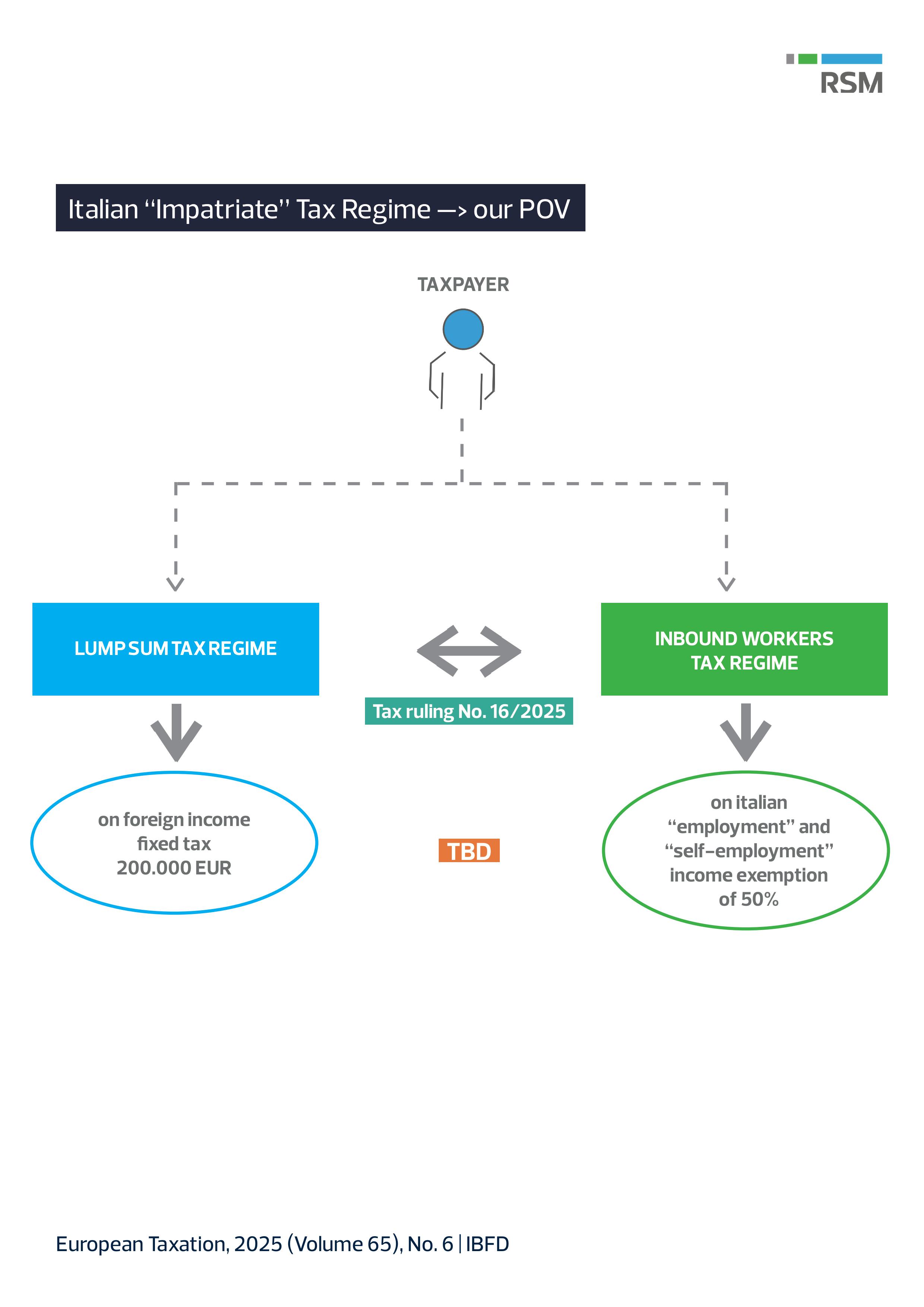

This raises the question of whether the same applies to the Italian Lump Sum Tax Regime and the new Inbound Workers Regime, given that there is no explicit prohibition in this scenario as well.

The sole provision that might hinder this combination is article 1, paragraph 154 of the 2017 Budget Law, which prohibits the cumulation of these regimes but refers specifically to the now repealed regime mentioned in article 16 of Legislative Decree 147/2015 regarding inbound workers.