The term " self-defense " refers to the power-duty attributed, in general, to Public Administration (and therefore to Tax Authorities) to automatically revoke its own acts if deemed illegitimate or unfounded.

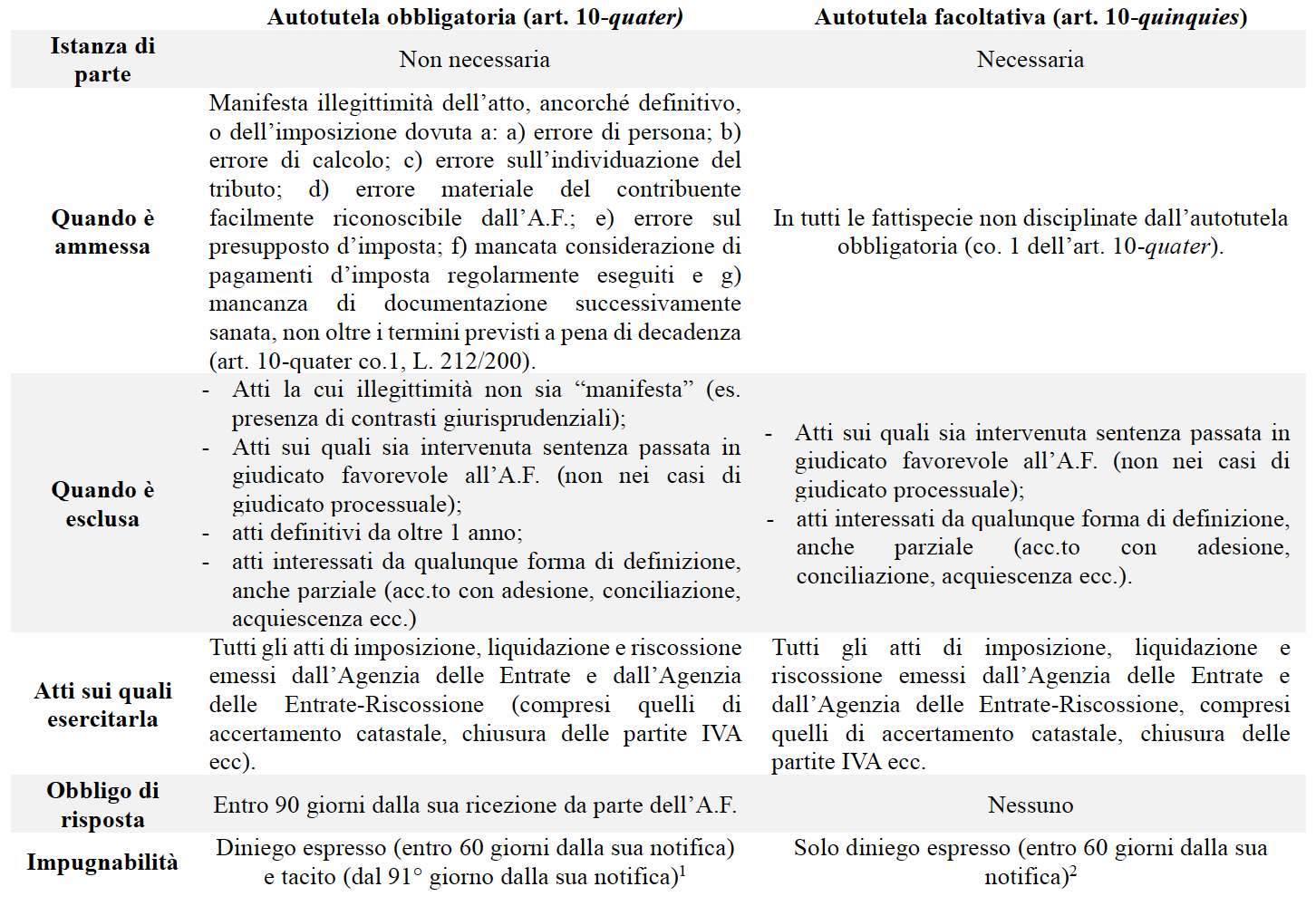

Distinguishing itself from the purely discretionary nature of the administrative self-defense power, the special discipline of tax self-defense procedure, now contained in Articles 10-quater and 10-quinquies of Law no. 212/2000 following the amendments to the Taxpayer Bill of Rights by Legislative Decree dated December 30th, 2023, no. 219 (hereinafter also referred to as the "Reform"), respectively assumes the dual connotation of "being compulsory", for cases of manifest unlawfulness of acts or impositions by the Tax Administration, and "optional", residually, for all other cases.

The specific details concerning the two forms of the tax self-defense procedure have, since their introduction, sparked an important interpretative debate that the Italian Tax Authorities recently attempted to address through the guidelines provided by the circular letter no. 21/E published in November 7th, (hereafter also "Circular"), offering official clarifications regarding the correct exercise of this power.

Please find below the main points:

- an exhaustive distinction between the two figures of the tax self-defense procedure:

- operational indications regarding the methods of submission and the content of the tax self-defense request;

Welcoming the insights from the established case law on this matter[1], it is clarified that the request for self-defense procedure should be directed solely to the Provincial Department of the Italian Tax Authorities that issued the act considered to be illegitimate or unfounded. If the taxpayer mistakenly addresses it to the wrong office, it will be the responsibility of the receiving office to forward it to the appropriate department.

Regarding the content of the application, it is required, in addition to the necessary formal elements (such as taxpayer information, contact details, references to the incorrect act, signature, etc.), that it be justified based on the factual and legal grounds supporting the request for total or partial cancellation. It should also be accompanied by the necessary documentation to allow for the review of the incorrect act. In cases of compulsory self-defense, the justification must relate to the categorization of the flaw as specified in paragraph 1 of article 10-quater of Law 212/2000.

- description of the procedures for conducting the investigation and the process for taking a self-defense measure.

In line with the principles of full and transparent cooperation with the taxpayer, the Italian Tax Authorities may request additional documentation, information and verification of similar acts issued by other offices, in order to reach a better decision regarding the request submitted by the taxpayer.

Decisions must be motivated, even per relationem, based on the facts and legal elements represented in the request and the documentation owned or provided by the taxpayer, complying with any restrictions provided by various tax laws[1]. Furthermore, if there are formal or procedural irregularities in the act subject to the self-defense, the final measure of the Italian Revenue Agency may also consist in a new act(so-called substitutive self-defense) in which the irregularities are corrected, respecting the principle of ne bis in idem and within the expiration terms of the assessment activity (unless a favorable judgment for the Italian Tax Authorities has become final), or integrated in cases of partial[2] or additional[3] assessment.

Lastly, the administrative suspension of the effects of the tax act, which is not expressly regulated, is guaranteed, and it is possible to take advantage of the definition of penalties pursuant to art. 17-bis of the Italian Legislative Decree 472/1997 following a partial annulment measure in self-defense by the office.

However, it is important to highlight that the appeal deadlines are not suspended, with the consequence that the act suspended within the administrative proceedings will be considered legitimate and founded until the total or partial acceptance of the self-defense.

- the definition of the administrative-accountability hypotheses of those required to exercise the power of self-defense, limited to cases of willful misconduct.

For both types of self-defense, the Reform limits the administrative responsibility of those charged with evaluating annulment requests to cases of willful misconduct only.

Despite the Circular letter providing useful operational guidelines regarding the reform's restyling of the tax self-defense procedure, unresolved issues persist that could compromise its usability for taxpayers.

Specifically, we refer to the possibility of appealing against the tacit denial of the Italian Tax Authorities in cases of compulsory self-defense, provided that the request for annulment is exclusively attributable to one of the cases strictly indicated in paragraph 1 of art. 10-quater and only after 90 days from the receipt of the application by the taxpayer.

According to the “ratio” of the reform, aimed at interpreting the instrument of self-defense no longer as a discretionary power exercisable ex officio by Italian Tax Authorities, the Legislator should have simplified the activation of this power by the taxpayer precisely in cases of manifest unlawfulness of the act, as well as better coordinating the terms of appeal of the tacit denial with those of a possible appeal in order to avoid that the risk of a potential silence from the office always forces the taxpayer to proceed with an autonomous appeal before the Tax Court.

Edited by Roberto Biondolillo

1 See order of the Supreme Court dated December 22th, 2018, no. 30229

2 See art. 32 par. 3 of the Italian Presidential Decree 600/1973 and art. 51 of the Italian Presidential Decree 633/1972

3 Art. 41-bis of the Italian Presidential Decree 600/1973 and art. 54-bis of the Italian Presidential Decree 633/1972

4 Art. 43 par. 3 of the Italian Presidential Decree 600/1973