Im Oktober 2024 veröffentlichte die Eidgenössische Steuerverwaltung (ESTV) das Kreisschreiben Nr. 6a, das das bisherige Kreisschreiben Nr. 6 aus dem Jahr 1997 ersetzt. Dieses Update war lange erwartet, da sich die wirtschaftlichen, buchhalterischen und steuerlichen Praktiken in den vergangenen Jahrzehnten erheblich weiterentwickelt haben.

Kreisschreiben 6a bringt wesentliche Klarstellungen und führt wichtige Änderungen bei der Identifikation und steuerlichen Behandlung von verdecktem Eigenkapital ein. Diese Neuerungen haben direkte Auswirkungen auf Schweizer Unternehmen, insbesondere im Hinblick auf konzerninterne Finanzierungen, die Abzugsfähigkeit von Zinsen und Risiken im Bereich der Verrechnungssteuer.

Was bedeutet verdecktes Eigenkapital?

Verdecktes Eigenkapital bezeichnet Fremdmittel (häufig Gesellschafter- oder konzerninterne Darlehen), die aufgrund ihrer Art oder übermässigen Höhe steuerlich als Eigenkapital umqualifiziert werden.

Diese Umqualifizierung hat folgende Konsequenzen:

- Nichtabzugsfähigkeit der Zinsen auf den Teil des Darlehens, der als Eigenkapital gilt

Verrechnungssteuer (35 %) auf die gezahlten Zinsen

Einbeziehung des verdeckten Eigenkapitals in die Bemessungsgrundlage der Kapitalsteuer

Wirtschaftliche Doppelbesteuerung in bestimmten Fällen

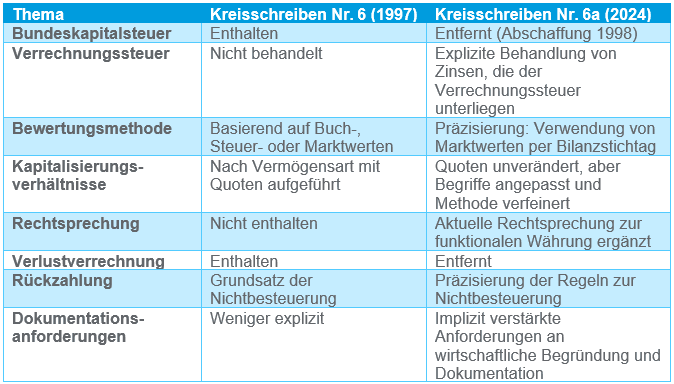

Kreisschreiben 6 vs. Kreisschreiben 6a: Was hat sich geändert?

Kreisschreiben 6a modernisiert den Ansatz der ESTV, indem es aktuelle Rechtsprechung und zeitgemässe Rechnungslegungspraktiken integriert.

Folgende Punkte haben sich geändert:

Die Änderungen zielen darauf ab, den Steueransatz zu modernisieren, Unsicherheiten bei der Anwendung zu verringern und die Schweizer Praxis international auszurichten.

Praktisches Beispiel

Eine Schweizer Gesellschaft besitzt eine Gewerbeimmobilie, die in der Buchhaltung mit CHF 5 Millionen erfasst ist. Ihr Marktwert beträgt jedoch CHF 6 Millionen. Gemäss den Kapitalisierungsverhältnissen des Kreisschreibens 6a darf die externe Finanzierung höchstens 70 % des Marktwerts betragen, also CHF 4,2 Millionen.

Wenn die Gesellschaft durch ein Gesellschafterdarlehen von CHF 4,5 Millionen finanziert wird, das vollständig zum maximal zulässigen Zinssatz verzinst ist, gelten CHF 300.000 als verdecktes Eigenkapital.

Die steuerlichen Konsequenzen sind:

- Zinsen auf diesem Betrag sind nicht steuerlich abzugsfähig.

- Es fällt eine Verrechnungssteuer von 35 % auf die gezahlten Zinsen an – die Gesellschaft muss den Fall der ESTV melden und ihn regularisieren.

- Die Gesellschaft muss die Höhe der Verschuldung und die Finanzierungsstruktur wirtschaftlich begründen.

- Das verdeckte Eigenkapital wird in die Bemessungsgrundlage der Kapitalsteuer einbezogen

Gut zu wissen: Diese Situation lässt sich durch eine Anpassung der Finanzierungsstruktur optimieren.

Wie RSM Sie unterstützen kann

Bei RSM Switzerland helfen wir Ihnen:

- Finanzierungsstrukturen im Hinblick auf Kreisschreiben 6a zu analysieren

- Kapitalisierungsverhältnisse zu modellieren und Risiken einer Umqualifizierung zu identifizieren

- Wirtschaftliche Dokumentation zu optimieren, um konzerninterne Darlehen zu begründen

- Steuerliche Auswirkungen im Zusammenhang mit Verrechnungssteuer und Nichtabzugsfähigkeit zu antizipieren

- Bei Kapitalrestrukturierungen zu unterstützen, um Risiken verdeckten Eigenkapitals zu vermeiden

Diese Massnahmen können sowohl während des Lebenszyklus eines Unternehmens als auch bereits bei der Gründung umgesetzt werden.

Wir unterstützen Sie gerne mit unseren Dienstleistungen zur Unternehmensgründung, da steuerliche Überlegungen ebenso entscheidend sind wie rechtliche für das reibungslose Funktionieren Ihrer Gesellschaften.

Unser Ansatz ist interdisziplinär: Wir kombinieren steuerliche, buchhalterische und rechtliche Expertise, um Ihnen massgeschneiderte Lösungen zu bieten, die auf Ihren Sektor und Ihre Struktur zugeschnitten sind.

Ihre Kontaktpersonen