Introduction

The Swiss Confederation does not levy inheritance or gift taxes; competence lies exclusively with the cantons.

As a result, there are significant disparities among cantons in the treatment of these taxes. This article focuses on the framework applicable in French-speaking or bilingual cantons.

In practice, movable assets are taxed at the domicile of the deceased or donor, while immovable property is taxed at its place of location. Consequently, this note does not cover real estate located abroad, the treatment of which must be assessed under the domestic law of the country where the property is situated. Additional specificities may also apply (e.g., shares in companies incorporated in the United States, France or the United Kingdom).

Spouses/registered partners

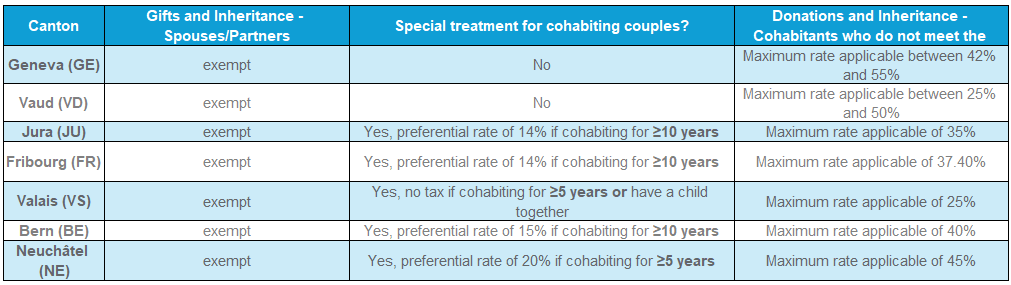

In the French-speaking cantons, transfers between spouses or registered partners (within the meaning of the Swiss registered partnership regime) are exempt from both inheritance and gift tax. This principle is confirmed by official cantonal guidance and forms the anchor point of estate planning for married couples.

In practice, the focus is therefore less on taxation and more on civil-law structuring (wills, inheritance agreements, choice of matrimonial regime) and on intercantonal/international coordination when the estate includes real property located in different cantons or countries.

Cohabiting partners

For cohabiting partners, the general rule is taxation at the scale applicable to unrelated third parties, that is, the highest schedule. However, several cantons grant preferential treatment where a minimum duration of cohabitation can be proven: Neuchâtel applies a reduced rate of 20% after five years of living together; Fribourg reduces the burden to 14% after ten years (subject to a shared tax domicile and supporting evidence); and Jura provides a 14% rate beyond ten years. Valais is currently an outlier, abolishing the tax for cohabiting partners from 1 January 2025 where either five years of cohabitation or the presence of a common child can be demonstrated.

Evidentiary requirements (continuity, domiciliation, documentation) are decisive; they are set out in official notices and legal texts, and it is essential to be able to substantiate cohabitation before the competent tax authorities.

The table below summarises the applicable cantonal practices as at 01.01.2025:

Gifts within the couple

The same logic that applies to inheritances generally applies to gifts. The main differences, where present, relate to the level of allowances or exemptions in the case of inter vivo transfers.

Practical implications and recommended approach

For a couple, the tax outcome depends first on status (marriage/registered partnership vs. cohabitation), then on the canton, and, where a preferential regime is available, on the ability to prove cohabitation.

Four levers emerge for cohabiting partners:

- Formally document cohabitation where required by law (certificates, joint lease, continuous domiciliation, shared expenses);

- Ensure that the asset transferred by gift or inheritance does not trigger taxation abroad;

- Calibrate the timing of transfers (stagger gifts, coordinate with real-estate holdings and taxing jurisdiction);

- As a last resort and depending on the partners’ wishes, consider moving to another canton to benefit, for example, from the Valais exemption or from reduced rates available in other cantonal jurisdictions.

Conclusion

These rules create significant differences between the treatment of married/registered couples and that of cohabiting partners in French-speaking Switzerland. With the Valais exemption from 2025 (subject to conditions), the preferential regimes of Neuchâtel, Fribourg and Jura (subject to proof of cohabitation), and other cantons that tax cohabiting partners as third parties, status, evidence and canton become decisive levers.

It is essential to integrate these differences into your inheritance and gift planning, calibrating documentation, domicile and timing to achieve the least burdensome outcome.

If you would like these rules translated into numbers and operational next steps for your situation, our experts are at your disposal.

Your Contacts