Background: Taxation of Real Estate Companies

When a property is owned by a real estate company (RE), the sale of that company’s shares may, in certain cantons, be treated for tax purposes as a sale of the property itself. *

Generally, the transfer of shares in a real estate company owned by either a legal entity or an individual may be considered an economic transfer of the property. The transaction is thus subject to real estate gains tax (IGI) calculated on the capital gain realized.

As a reminder, IGI is a cantonal tax. Consequently, the step-up mechanism applicable to this tax has no effect on federal tax.

*For more information and details regarding the sale of real estate companies in Switzerland, we invite you to read our article on this subject.

The Risk of Double Taxation

Initial Taxation Upon the Share Deal

In certain situations, a double taxation issue may arise:

Upon the sale of the real estate company’s shares (share deal), the shareholder is liable for real estate gains tax (IGI). This tax is calculated by “isolating” the value of the real estate (book value of the asset, mortgage debt, etc.) from the total price of the shares.

A second round of taxation upon the sale of the building

Upon a subsequent sale of the building by the company (asset deal), the same economic capital gain may be taxed a second time at the corporate level via cantonal and municipal income tax (IBCC). This is because the book value of the property in question has not changed following the initial share deal.

This situation may result in repeated taxation of the same economic substance.

The “step-up” mechanism

To address this situation, certain cantonal tax authorities have adopted a practice that, under certain conditions, allows the value used at the time of the transfer of the real estate company’s shares to be recognized for tax purposes.

Specifically:

- Upon the sale of the shares, a taxable hidden reserve corresponding to the capital gain already taxed may be recognized in the company’s tax accounts.

- In the event of a subsequent sale of the property, this hidden reserve allows for the neutralization of all or part of the taxable gain for IBCC purposes.

- The same economic capital gain is thus not taxed a second time.

This mechanism is commonly referred to as “step-up”

Application of the “step-up”

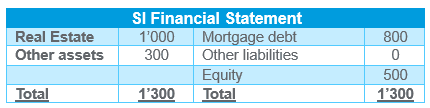

1. Sale of shares by the shareholder in year N

Assumptions: Sale price of shares = CHF 1,500, Sale price of the property = CHF 2,000, Acquisition value of the property = CHF 1,000

1. Sale of the building by the SI in year N+X – WITH step-up

Assumptions: Sale price of the building = CHF 3,000

ICC: Use of the SI's tax balance sheet to determine taxable income.

IFD: Use of the SI's financial balance sheet to determine taxable income.

In fact, this mechanism is a matter of cantonal practice. It has no effect on federal tax, as federal tax law does not provide for an equivalent step-up mechanism in connection with the economic transfers of real estate companies.

Federal Supreme Court Case Law

While the step-up principle is recognized in certain specific situations, recent case law of the Federal Supreme Court has clarified that, with regard to real estate companies, no tax revaluation of real estate may be required in the absence of a cantonal legal basis, particularly when a real estate gains tax has been levied at the shareholder level during an economic transfer (“share deal”). The step-up mechanism thus does not constitute a general principle of federal tax law but rather falls under the solutions provided for by cantonal law. The case law therefore follows a logic of allocating jurisdiction between federal and cantonal law, without recognizing an automatic right to adjust the tax value to avoid potential economic double taxation.

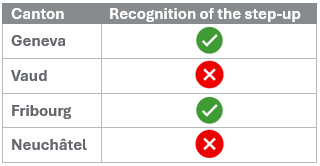

Overview of French-speaking Switzerland

The practice of step-up still varies significantly from one canton to another.

Conditions for Application in Geneva

The application of the step-up is not automatic and is permitted under the following cumulative conditions:

- The sale of the interest in the investment company by the individual (held as part of personal assets) must have actually resulted in the collection of an IGI in Geneva at a rate of at least 10%, i.e., higher than the cantonal and municipal tax rate on the neutralized profit within the investment company at the time of the sale of the property;• At the time of the real estate’s sale by the SI, the recognition of the net real estate gain already taxed (tax neutralization of the real estate gain at the SI level) is granted, at most, only up to the amount of the reported economic real estate gain, excluding the book gain comprising any catch-up depreciation allowed for tax purposes within the SI;

- The Geneva-based SI must request the recognition of the net capital gain already taxed no later than before the tax assessment for the tax period during which the individual disposed of the interest becomes final;

- The SI making the request must first obtain a waiver of tax secrecy from the shareholder who sold the interest in the SI;

- The inclusion of the net real estate gain already taxed is permitted, per property, up to the amount of the net real estate gain (after deduction of expenses) previously taxed under the IGI for the individual.

A request for approval must be submitted to the Tax Affairs Directorateand must be accompanied by the tax secrecy waiver form.

In our experience, the Canton of Fribourg generally adopts the conditions in force in the Canton of Geneva.

Conclusion: A Tax Tool to Anticipate

The step-up is now a central element of real estate company taxation. Its introduction helps limit situations of economic double taxation and enhances the attractiveness of transactions carried out as “share deals.”

Its application, however, varies significantly by canton and remains subject to their respective rules and practices.

A preliminary analysis is essential for any transaction involving a real estate company. We also strongly recommend approaching the cantonal tax authorities to request a prior approval (tax ruling) to validate the tax treatment of the proposed transaction(s).

Our experts are at your disposal to assess your situation and support you in your future projects, as well as to answer any questions you may have.