In the context of cross-border employment relationships between Germany and Switzerland, also the question of the allocation of taxation rights for employment income of employees in management positions arises. The following article examines the tax classification and specific Swiss tax practice for senior executives who are tax residents in Germany and hold a senior position at a company based in Switzerland.

Swiss tax law

Individuals who are not tax resident in Switzerland are subject to limited tax liability in Switzerland if, among other things, they physically carry out gainful employment in Switzerland or if they physically carry out gainful employment abroad for an employer with its registered office, actual administration or permanent establishment in Switzerland and Switzerland is granted the right of taxation with regard to the gainful employment physically exercised abroad in accordance with the applicable double taxation agreement with the respective neighbouring country.

Double tax treaty (DTA) Switzerland-Germany

In addition to limited tax liability in Switzerland, individuals who are tax resident in Germany are subject to unlimited tax liability under German tax law. Consequently, both countries levy tax on employment income, which, in a first step, results in a double taxation. Thanks to the DTA between Switzerland and Germany, this is avoided by assigning the right to tax employment income to only one contracting state.

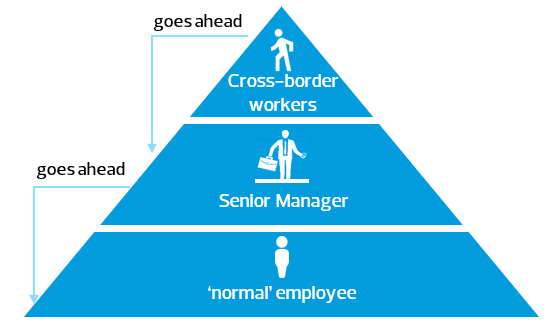

In the case of a person in a management position, the following steps must be examined in the specified hierarchical procedure:

If the employee is not considered a cross-border commuter, in a second step it is to check whether he or she qualifies as a senior executive within the meaning of Art. 15 para. 4 of the DTA between Switzerland and Germany.

To qualify as senior executive, the following criteria must be met cumulatively:

- Cross-border residence/work relationship;

- No qualification as a cross-border commuter;

- Dependent employment;

- Entry in the commercial trade register with single or collective signature or a verifiable comparable authority to represent the company externally;

- Function as a member of the board of directors, director, deputy director, vice-director, general director, managing director, authorised signatory (or comparable function);

- Activity does not only include tasks outside the employer's country of residence;

- Employer is a corporation.

Whether comparable authority to represent the company externally exists can be assessed on the basis of the following criteria:

- Amount of remuneration;

- Classification in one of the highest salary levels within the company;

- Granting and amount of profit sharing/profit bonus;

- Granting of a special monetary benefit;

- Number of persons bound by instructions;

- Authority to independently hire and dismiss employees;

- Promotion/advancement associated with a change or expansion of the area of responsibility;

- No application of legal limits on maximum working hours.

Not all criteria need to be met in order for a qualifying power of representation to be assumed. The overall circumstances are considered individually in each case.

Through informal consultations with several cantonal tax authorities (ZH, BS, SH, ZG, TG), we have determined that the above approach and thus the consultation agreement of 6 April 2023 are not being implemented uniformly in practice. Some cantons are implementing the consultation agreement as intended. Other cantons are focusing on the above criteria regarding the authority to represent the company externally and are reviewing these with or without an entry in the commercial trade register. A third of the cantons surveyed are focusing on Germany's perspective.

The salary of a senior executive is always taxable in the contracting state where the employer is seated, regardless of where the work was physically performed (i.e. working days in the country of residence of the employee, in the employer's country of residence, in third countries). This contrasts with ‘normal’ employees, for whom the right of taxation is primarily assigned to the contracting state in which the physical work was performed and secondarily to the country of residence (183 day-clause). In Germany, the employment income of a senior executive working for a Swiss company is exempt from taxation subject to progression. There is no overarching taxation by the German tax authorities.

Swiss assessment procedure

Swiss wage source taxes

Regardless of their nationality or residence status under immigration law (e.g. cross-border commuters, weekly residents, short-term residents), individuals being resident abroad are subject to Swiss wage source taxes if the salary is paid by a debtor having its domicile, registered office, actual administration, permanent establishment or fixed facility in Switzerland.

The taxpayer's worldwide gross employment income is taken into account when determining the rate-determining income, regardless of the country in which this income was earned.

Recalculation of the Swiss wage source taxes

Individuals being tax resident abroad have, regardless of their income level, the option (voluntary) to submit an application for a recalculation of their Swiss wage source taxes (formerly tariff correction) if they are not required to file a tax return. An application for recalculation may be advisable if:

- The taxable and/or rate-determining gross salary is incorrect (e.g. if taxable income earned abroad has not been allocated correctly or has not been taken into account for the tax rate determination);

- An incorrectly applied withholding tax rate shall be corrected.

Subsequent ordinary assessment

In certain circumstances, individuals being tax resident abroad are obliged or have the option (voluntarily) to submit a regular Swiss tax return retrospectively.

Individuals being subject to Swiss wage source taxes and who are tax resident abroad may be required to submit a tax return if they have income or assets that are taxable in Switzerland, but are partially subject to Swiss withholding taxes (e.g. salary, securities income) and partly subject to the ordinary assessment procedure (e.g. self-employed income, real estate income).

They may (voluntarily) apply for subsequent ordinary assessment if at least 90% of their worldwide gross income is subject to taxation in Switzerland in the relevant tax period.

Digression: Risks of corporate tax law

In addition to the tax consequences for the employee, there are also potential tax consequences for the employer.

If, for example, the senior executive in Germany (e.g. when working from home) regularly concludes contracts or makes management decisions on behalf of and for the account of the Swiss employer, there is a risk that the Swiss company will establish a permanent establishment in Germany.

If all measures necessary for the management of the business are regularly taken in Germany, the German tax authorities could even argue that the centre of the Swiss employer's senior management and thus its effective place of management is in Germany.

In both cases, the Swiss company would become liable for corporation tax in Germany, either limited or unlimited. Further tax obligations for German business tax and VAT could follow and also transfer pricing issues would have to be clarified.

Conclusion

Senior executives within the meaning of Art. 15 para. 4 of the DTA Switzerland-Germany are specially taxed. Regardless of where they physically perform their work, they are always taxable in the country where their employer is seated.

Due to the constantly changing legal basis and its varying interpretation and implementation in practice by the Swiss cantonal tax authorities on the one hand and the German tax authorities on the other hand, it is advisable to examine the tax consequences and risks for both the employee and the employer before concluding an employment contract. Proactive clarifications can help to avoid unpleasant surprises. We would be happy to assist you in this regard.