Are your systems ready for the new VAT rates?

With this news alert, we would like to draw your attention once again to the fact that the VAT rates will change on January 1, 2024 as shown below. Please note that these rate changes may require adjustments to your systems. Please remember to take the necessary precautions in good time.

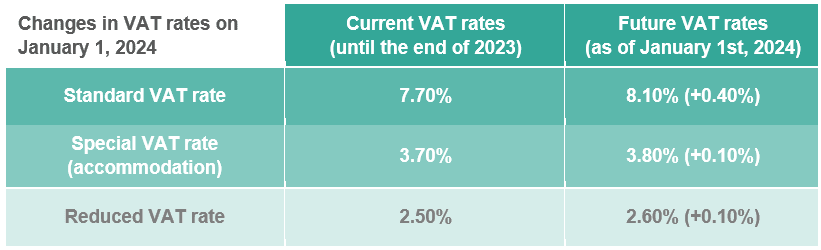

The Swiss VAT rates will be changed on January 1, 2024, according to the table below:

This already has consequences in 2023 for certain companies that provide services over multiple periods (billing in 2023 for services that will be provided beyond the end of the year).

In fact, the VAT debt arises, regardless of the applicable VAT rate, at the time of billing (or at the time of payment when the company counts VAT based on received considerations). However, what is decisive for determining the applicable VAT rate is neither the invoice date or the date of collection but the date or period when the service is provided.

Thus, each taxpayer must identify if it is necessary to apply the new VAT rates for certain services as of the first quarter of 2023.

If the date or effective period of the service concerns 2024, the updated VAT rates must be applied. In principle, taxable services provided before January 1, 2024, are subject to current VAT rates, while taxable services provided after December 31, 2023, are subject to the new VAT rates.

Annual services provided partly after the rate increase

Subscriptions for transport services (e.g. half-fare and general subscriptions, seasonal subscriptions for skiing), telecommunications, or contracts for the service and maintenance of elevators, household appliances, computer systems, etc., generally have to be paid in advance. If such a subscription or contract extends beyond the date of the rate increase, a pro rata temporis allocation of the counter-consideration between the current rate and the new rate must be made. If this is not the case, the tax authorities reserve the right to consider the entire service at the higher tax rate.

Other advance payments and invoices for advance payments

If, at the time of the advance payment or the invoice for advance payment (e.g. rentals for which it was opted, construction services, etc.), it is planned that the delivery or service will be fully or partly performed after December 31, 2023, the part of the service that will be provided after that date must already be subject to the new rate in the invoices sent to the customer.

If it is not clear from the invoice when and to what extent the supplies were rendered and what part of the remuneration is attributable to the respective services, the total consideration is, in principle, subject to the higher VAT rate. It is therefore essential for companies to understand the billing and accounting rules related to these VAT rate changes to avoid any risk of error or non-compliance. It is also recommended to plan ahead to avoid any problem or delay in the application of the new rates.

For taxable companies that do not perform services over multiple periods, the changes in VAT rates will not have any major consequences. However, it is advisable to review the billing and accounting procedures to ensure compliance with the new VAT rates.