Preliminary considerations

The Swiss tax system mirrors Switzerland’s federal structure, which consists of 26 sovereign cantons with more than two thousand independent municipalities. All cantons have full right of taxation except for taxes that are exclusively reserved for the federal government. Consequently, Switzerland has three levels of taxation: the federal, the cantonal and the communal level. For several years now, formal aspects of the various cantonal tax laws regarding income tax have been harmonised, for example, regarding the determination of taxable income, deductions, tax periods, and assessment procedures. The cantons and municipalities still have significant autonomy for the quantitative aspects of taxation especially with respect to determining the applicable tax rates. Consequently, the tax burden varies considerably between cantons.

Another important element is that to comply with international taxation standards, the Swiss Federal Council and Swiss Parliament has adopted a significant revision of the Swiss corporate tax regime (Corporate tax reform) since 1st January 2020. Consequently, the special tax regimes which granted various tax privileges at the cantonal level (privileged taxation as holding company, mixed company, domicile company) has been abolished.

Nevertheless, the tax reform ensures that Switzerland remains an attractive place of business by introducing internationally recognised replacement measures such as:

- A general decrease of the corporate effective income tax rates at the cantonal level, thus securing Switzerland’s competitiveness. Effective tax rates as low as 12% - 21%.

- Mandatory tax deductions (patent box) on Swiss and foreign patents or comparable rights, as well as super deductions on income from patents and qualifying Swiss sourced R&D expenses.

- A notional interest deduction on excess equity.

Finally, starting from 1st January 2024, Switzerland will introduce the OECD minimum tax rate of 15% for large multinational enterprises with a global annual turnover of at least EUR 750 million. For companies falling in the scope of this new framework, the above measures may cause their effective tax rates to fall below the minimum rate of 15% and thus trigger the payment of a supplementary tax.

Tax treatment of income and gains

Rental income and rental value

Individuals

Introduction

Switzerland distinguishes between two kinds of individuals: employed individuals and self-employed individuals who are a hybrid category between individuals and companies. In most instances, self-employed individuals and employed individuals alike must pay income and wealth taxes; however, self-employed individuals must file a tax return based on their commercial wealth (business accounts) and on personal wealth. Commercial wealth includes all elements of wealth which serve self-employment, wholly or predominantly. For instance, capital gains arising from the alienation of commercial assets will be taxed as ordinary income from self-employment. Self-employed individuals are, on the other hand, entitled to fiscally deduct everything which is commercially justified expense like companies.

Liability to tax

The taxable income of an individual does not only include rental or lease fees received from third parties, but also the rental value of the immovable property used personally by the taxpayer (fictitious taxable income), even for one day. The rental value of a property is determined by the cantonal tax authorities and corresponds to the income that could be generated if the building was rented. Such rental income is communicated to the owner of the real estate by the cantonal tax authorities. It is generally between 70% and 90% of the rental market value if the property was rented out in the market.

Basis to tax

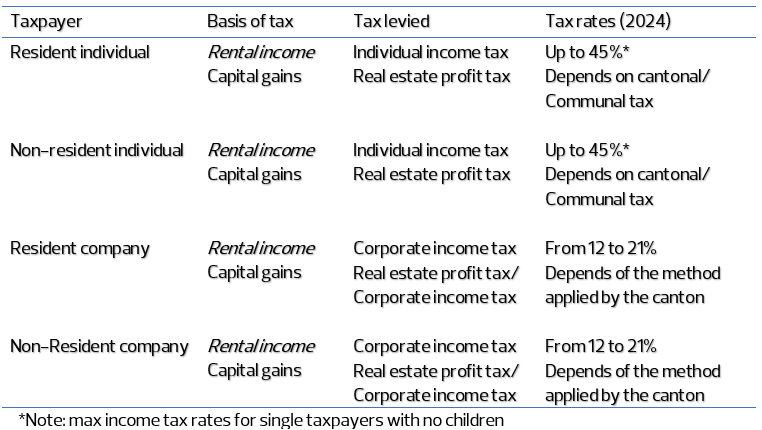

Individuals are subject to taxation on federal and cantonal/communal level if they have their permanent or temporary residence in Switzerland. Resident individuals are subject to tax on their worldwide income. However, revenues derived from business conducted abroad, permanent establishments, and from immovable property situated abroad are exempt but considered to determine the applicable tax rate (exemption with progression).

Non-resident individuals are only taxed on Swiss-sourced income and wealth (limited tax liability), if: they receive income by physically working in Switzerland or are member of the board of directors or the management board of a Swiss company; they are creditor or beneficiary of claims secured by a mortgage on real estate in Switzerland or have real estate in Switzerland; they receive pensions and similar income from former public law employment; they generate income allocated to a fixed place of business in Switzerland.

Companies

Introduction

Rental income is added to a company’s net profit and treated as ordinary business income.

Liability to tax

Instead of the personal income and wealth tax, companies pay a federal, cantonal and communal tax on the net profit and – but only at cantonal and/or communal level - a supplementary tax on equity and reserves (accumulated retained earnings). The net profit of a company consists of all earnings and capital gains realised by a company during a commercial year decreased by commercially justifiable expenses. Accordingly, rental income is subject to corporate income tax as business earning.

Basis to tax

Companies which have their registered office or effective administration in Switzerland are liable to federal, cantonal and communal corporate taxes on an unlimited basis. However, this liability doesn’t extend to companies, permanent establishments and real estate located abroad.

On the contrary, non-resident-companies are deemed resident for tax purposes through economic affiliation when: they are associated with a company established in Switzerland; they operate a permanent establishment in Switzerland; own real estate located in Switzerland or have real occupancy rights on such real estate or personal rights similar economically to real occupancy rights; are holders or usufructuaries’ of debts secured by a mortgage or security on real estate located in Switzerland; deal in real estate located in Switzerland or act as brokers in real estate transactions.

A proportionate federal effective tax rate of 7.8% is levied on the net profit. Each canton and commune can define its own tax rate. Together with the federal tax, the overall effective income tax rate can vary from 12% to 21% depending on the region. With the introduction of a minimum tax rate for large multinational enterprises (global annual turnover of EUR 750 million or more), the effective tax rate would be of at least 15% for these companies.

Capital gains

Individuals

Introduction

Regarding taxation of capital gains on immovable assets, no special tax is levied at the federal level, whereas all the cantons levy such tax. Furthermore, the tax will in some instances be levied by the canton alone, on the other hand, cantonal legislation can enable municipalities to be the recipients of the special tax. Moreover, in most cantons, the scale of the special tax on real estate gains depends on two factors: the amount of the gain and the length of possession. The law even provides a higher tax burden on short term profit-oriented sales. Respectively, sellers can benefit from a tax deduction in case of lengthy possession.

Finally, at the cantonal level, two different systems apply on taxation of capital gains:

- The monist system: all capital gains realised through the sale of immovable assets are subject to a special ‘real estate profit tax’ which applies to individuals and companies alike.

- The dualist system: capital gains realised through the sale of immovable assets in the private wealth of individuals are taxed separately based on the special tax (as described above). However, gains realised on commercial wealth (self-employed individuals and companies) are subject to the ordinary income tax (up to 45%), respectively the corporate income tax (between 12% to 21% depending on the region).

Liability to tax

Depending on the cantonal system applied, capital gains made on the sale of commercial assets by a self-employed individual are either liable to personal income tax or special tax on capital gains. Regarding the tax treatment of private capital gains on the other hand, they are subject to special tax on capital gains.

Basis of tax

The taxable income represents the difference between the profit arising from the sale and the investments expenses (acquisition price and upgrades) and the legal deductions (administrative costs, commission fees, etc).

The computation varies between cantons:

- Some cantons treat each capital gain separately and consider the amount of the gain and/or the length of possession.

- Whereas some other cantons tax all capital gains realised within a particular timeframe.

Companies

Introduction

Swiss corporate income tax includes capital gains realised through sale of moveable or immovable assets. As commercial capital gains are not exempted, they are added to the company’s profits.

Liability to tax

Business income is taxed against an effective tax rate of 7.8% at the federal level, and up to 21% including cantonal and communal tax.

Basis of tax

Please refer to the section applicable to individuals.

Exemptions

Taxation on capital gains can be deferred provided that:

- A company reinvests in equally essential commercial assets within two years.

- Within the Swiss territory.

- At similar book value.

The same deferral applies to capital gains on moveable assets when:

- A company reinvests in equally essential commercial assets within two years.

- The stakes held by the company amounts to 10% of the share capital at the time of the sale.

- The holding period lasted at least a year.

Swiss VAT & real estate transfer tax

![]()

Value added tax

Individuals

Introduction

The confederation levies a general tax on consumption with deduction of the input tax at each stage of the production and distribution.

Liability to tax

Unless they are exempted by Swiss VAT law, commercial or professional activities performed in Switzerland are subject to the VAT. Moreover, irrespective of their legal form, businesses (self-employed individuals included) are liable to VAT, except when their annual turnover from taxable supplies generated in Switzerland and/or abroad is less than CHF 100’000.

Basis of tax

As a rule, the supply and lease of non-commercial immovable property are exempt from VAT. Thus, the sale of a residential estate between individuals is not subject to VAT. However, in case of a sale of commercial real estate made by an individual liable to Swiss VAT, the operation can be subjected to VAT on a voluntary basis. Likewise, the lease of a commercial estate by an individual liable to VAT to another VAT taxpayer can also be subjected to VAT.

Companies

Introduction

The same rules that apply for self-employed individuals apply to companies.

Real estate transfer Tax

Individuals

Introduction

The tax is levied on the transfer of real estate from one person or company to another. Rights on immovable property (share deal) can qualify as real estate.

Liability to tax

Transfer taxes applies on the acquisition of the legal or economic ownership of Swiss real estate and is usually payable by the purchaser. However, depending on the canton, the tax may be split between the purchaser and the seller whether by contract or by law.

Basis of tax

The real estate transfer tax varies from canton to canton. The market value of the immovable property is taxed against a proportionate tax rate of 0.0% and 3.3%.

Exemptions

There are various exemptions available in case of a merger, transformation, restructuration, or transfer of wealth. Other cases include donations, successions, exchange or forced sale in case of bankruptcy.

Companies

Similar rules apply for companies.

Swiss local taxes

Individuals

Introduction

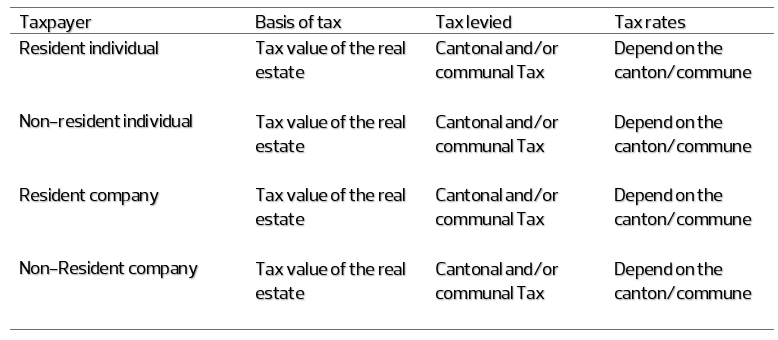

The real estate tax is a cantonal and/or communal tax levied on a periodic basis on Swiss real estate. The tax is collected each year and generally calculated according to the determining tax value existing at the end of each tax period.

Liability to tax

Every owner of residential or commercial buildings in Switzerland is liable to the real estate tax. However, certain cantons have decided not to levy the tax.

Basis of tax

The real estate tax is a proportionate tax expressed in % based on the tax value of the real estate. The tax value is determined by the competent authorities. Depending on the canton, they apply a formula or make an on-site estimate. As a general rule, the tax value is between 70 and 90% of the market value of the property. Local authorities determine the amount of the tax in their real estate tax laws, in some instances it can go up to 3%.

Companies

Exemptions

Apart from public buildings or real estate intended for public use, cantonal laws provide exemptions for religious organisations, or real estate that belong to companies whose primary objectives are philanthropy and social well-being.

Swiss Wealth tax

Individuals

Introduction

Wealth tax is a cantonal and municipal tax levied on the total net market value of assets, including real estate. Loans on the real estate are deductible.

Liability to tax

Wealth tax is due on the net wealth of individuals. Net wealth includes the value of real estate less the liabilities related to the real estate and other social deductions.

Basis of tax

Wealth tax is generally composed of a progressive tax rate expressed in per mile, multiplied by a periodically fixed coefficient, while a few cantons apply a proportionate tax rate. Fiscal burden may vary between 0.0010% and 1%. Moreover, certain municipalities levy a tax based on the cantonal tax.

Exemptions

Public agents of foreign states, and diplomats are exempted from the wealth tax. The taxation of wealth in Switzerland is dependent on the individual’s tax residence status. A foreign individual who is regarded as a tax resident in Switzerland will in general be subject to tax on worldwide net wealth while a non‑resident taxpayer is only subject to Swiss taxation on Swiss situs assets.

Companies

Not applicable because unlike individuals, companies are taxed on their net profit and their equity.

Vehicles for Swiss real estate

Commonly used vehicles for ownership and management of real estate

Limited Company

Companies most frequently used for the ownership, management and sale of Swiss real estate are known as real estate companies (sociétés immobilières). They are first and foremost Swiss limited companies (AG/SA), the designation is meant for tax purposes only. The equity is divided into shares and the shareholders of the company are not personally liable for the business debt.

Partnership & joint ventures

Corporate joint ventures and Swiss limited liability companies are similarly treated for tax purposes. On the other hand, contractual joint ventures (sociétés simples) have no legal personality and are not subject to taxation as such, they are considered fully transparent unless they qualify as a permanent establishment. Losses of the joint venture may therefore be offset against the income of the partners.

Trusts

Duly established trusts are recognised by Swiss authorities, as long as they are in accordance with Swiss imperative laws. Trusts have no legal personality. Moreover, if neither the settlor nor any of the beneficiaries are Swiss residents and if the trust assets do not include any Swiss real property, the trust arrangement is not subject to Swiss income taxes.

However, regarding Swiss-related trusts, settlors, trustees and beneficiaries are liable to Swiss taxes in several instances:

- Settlors of revocable trusts domiciled in Switzerland remain liable to individual income tax and individual wealth tax, since revocable trusts are transparent for Swiss tax purposes. Thus, all the trust’s assets, and all income earned by the trust will be allocated to the settlor. Distributions to the beneficiaries are taxed as a donation. Donations from parents to their children (or vice versa) are generally not subject to gift tax in most cantons. Thus, resident beneficiaries of a revocable trust established by a direct line settlor can still be fully exempt from tax, irrespective of the settlor’s place of residence.

- The establishment of an irrevocable fixed interests trust is treated as a donation. The structure will be subject to cantonal donation and inheritance laws. The position of beneficiaries is analogous that of an usufructuary. Therefore, the trust assets and all income derived from these assets is attributed to the beneficiaries. The portion attributable to the Swiss beneficiaries is subject to cantonal wealth tax. Distributions are considered as taxable income in the hands of the Swiss beneficiaries. Consistent with general income tax rules, capital gains and distributions of trust property are not subject to tax.

- Irrevocable discretionary trusts are treated as donations and subject to cantonal donation and inheritance taxes. No Swiss tax is due on the establishment if the settlor is not a Swiss resident. Regarding Swiss resident settlors however, the trust assets remain attributable to them. As beneficiaries only have contingent rights, no donation effectively occurred. Therefore, the resident settlor will remain taxable as the owner of the trust assets. As long as the assets are not attributed to particular beneficiaries, no wealth tax will be payable by Swiss resident beneficiaries. Instead, the wealth tax will be levied in the hands of the settlor. Distribution of income is taxable income of the Swiss resident beneficiaries. Exceptionally, capital gains attributable to Swiss resident beneficiaries are taxed as regular income.

Trustees domiciled in Switzerland are only liable to income tax on the income they earn in exchange to the services they provide.

Specific real estate vehicles for Swiss real estate

Real estate funds

Swiss real estate funds exist in three forms: either open (contractual or SICAV) or closed (SCPC). The tax treatment of real estate funds depends on whether the fund holds real estate either directly or indirectly through a real estate company. As a rule, contractual real estate funds have no legal personality and are therefore tax exempt from corporate income and capital tax. Income arising from the fund is taxable in the hands of the investors. Nevertheless, real estate funds holding real estate in direct property are assimilated to natural persons and are thus taxable subjects. At the Federal level, the applicable rate is half the ordinary tax rate. Capital gains are taxed at the level of the fund, irrespective of its form. When the fund holds real estate in direct property, transfer tax is levied at the level of the fund itself.

Regarding the individuals acting as investors, all the income arising from the fund are taxable in their hands, provided that the units of the fund are held in their private wealth. As for self-employed individuals or natural persons holding units in their commercial wealth, all income arising from a fund not holding real estate in direct property is taxed as personal income or business income. Regarding personal wealth, assets taxed in the hands of the fund shall not be taxed in the hands of the investors as well.