THE GROWING RELEVANCE OF TRANSFER PRICING IN THE WORLD

Transfer pricing is receiving increasing attention from tax authorities. Indeed, there is globally a marked increase in the number of audits on how intra-group transfer pricing is determined. The intent is clearly to recover revenue in an area that particularly lends itself to non-compliance with tax regulations. Moreover, not only the rules but also the approaches followed in different countries by the respective supervisory and police bodies can vary significantly.

It is well known that multinational groups may tend to implement profit-draining policies in countries with favourable tax regimes. It is equally true that formal and substantive transfer pricing compliance is not always easily pursued. The risk of challenges and penalties is therefore now more relevant than ever.

Transfer pricing is not just about compliance with the law. Product, market, and competition analysis, which underlies the correct quantification of prices to be attributed to intercompany items, can provide very useful support for strategic decision making.

TRANSFER PRICING IN THE ITALIAN CONTEXT

In Italy the preparation of the compliant TP documentation is optional. A taxpayer who intends to benefit from the favourable regime is required to prepare two documents: the Masterfile and the National Documentation. The former provides an overview of the group while the latter focuses on the taxpayer. The advantage associated with their preparation consists in the recognition of a beneficial regime that entails the non-application of penalties in the event that the Tax Authorities determine that there is more income to be taxed, provided, however, that the documentation is complete, truthful and useful for the purposes of control. The tax authorities have effectively abandoned certain practices that in the past had led to the denial of the benefit of penalty protection for mere disagreement on the method used as well as on comparable subjects or transactions. But that's not all. Documentation gives consistency to transaction values with respect to the structure of the business, provides more complete information for the preparation of the annual financial statements, and contributes to the creation of a transfer pricing culture that facilitates the identification of other opportunities, related to tax matters, but also, for example, to intangibles.

Aiming at compliance within TP means generating economic value for the company and its shareholders

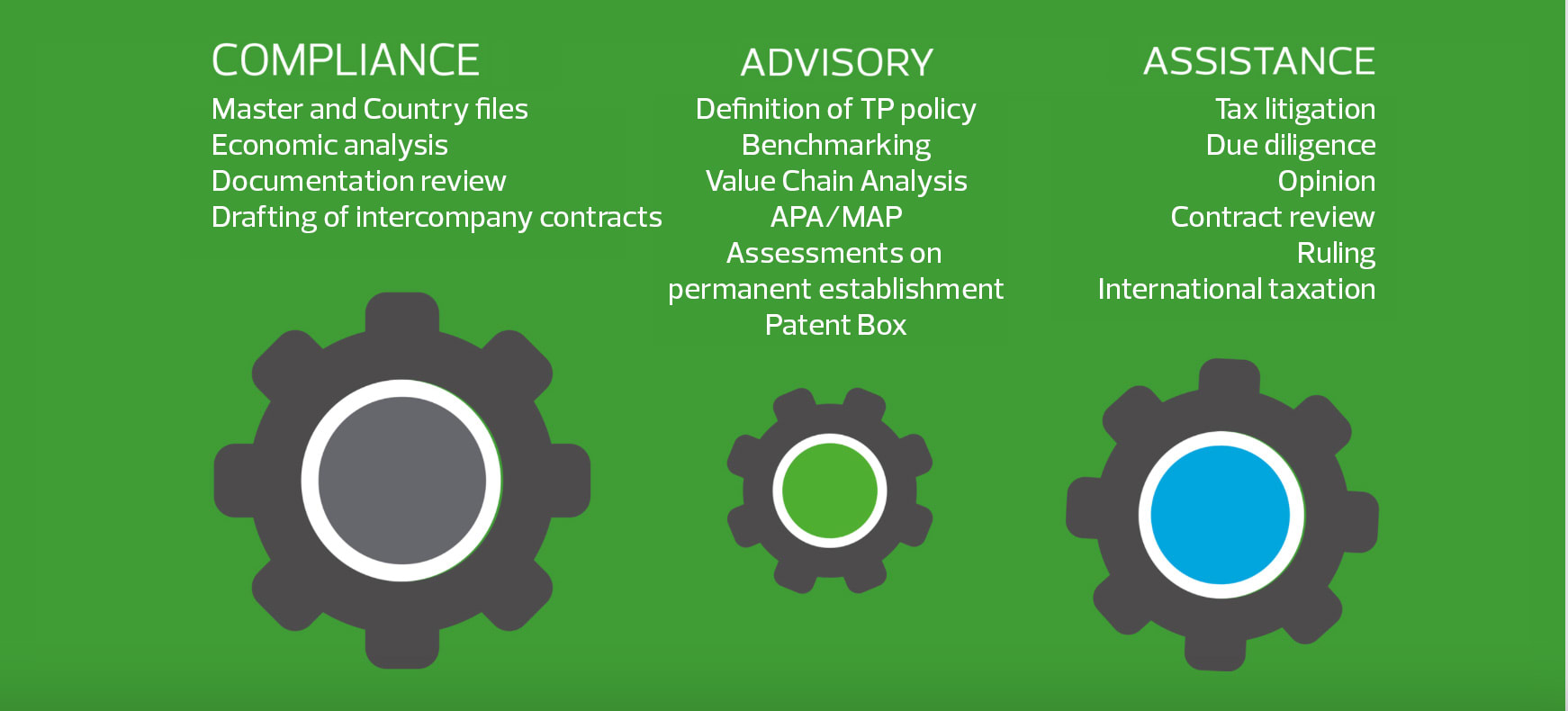

OUR APPROACH TO TRANSFER PRICING

RSM has a team of transfer pricing experts ready to assist in developing a document set that complies with local requirements existing in Italy and in most countries around the world.

In the event of a tax audit or a request for information by tax authorities, RSM can provide support in preparing a defense strategy that takes into account existing regulations, guidelines and practices both locally and internationally. Moreover, our services also extend to support at the litigation stage.

Our professionals can best understand the needs and assist in the steps leading to the conclusion of an Advance Pricing Agreement and a Mutual Agreement Procedure.

The transfer pricing team will seek to identify functions, risks and resources in order to reallocate them in the most tax-efficient manner. We also provide support in analyzing the numerous business changes that follow the change of processes underlying the value chain.

RSM can assist companies in preparing economic-statistical analyses and comparisons of industrial and financial transactions. The results of such analyses provide valuable guidance for strategic decisions.

RSM assists its clients in the preparation of contracts, due diligence stages, pricing of debt and intellectual property, and public procedures such as those related to incentives for Research and Development

Other Corporate Tax Compliance and Advisory services