With the recent introduction of the Federal Digital Games Tax Offset (DGTO) into law, an unprecedented opportunity has arisen for Australian game developers to fuel their growth.

Coupled with State-based benefits introduced over the past few years, industry support for gaming is as high as any other incentive in Australian history. Costs from 1 July 2022 are eligible!

What is the baseline benefit?

The baseline benefit is a 30% refundable tax offset (regardless of aggregated turnover), which allows businesses of all sizes to claim at least 30% of eligible expenditures, regardless of taxable position or turnover.

What are the potential benefits?

The reason the new DGTO is a game-changer is because unlike other Incentives such as the Research and Development Tax Incentive where the entity forgoes other benefits (ie. grant clawback, forgo tax deductions etc), the DGTO specifically allows you to:

- Keep your tax deductions (worth 25% - 30% additional benefit); and

- Keep the benefit of specific grants* (for example, the NSW Digital Games Rebate or the Vic Screen Incentive both offer an additional 10% benefit, whilst the Qld Digital Games Incentive adds an additional 15% benefit).

In total, in certain circumstances, the benefit on some qualifying expenditures could reach 75% per dollar of spend.

*Some grants require adjustments where they are broad-based.

Basic eligibility rules

Whilst seemingly simple, the DGTO sits in the new Div 378 of the ITAA 1997 and contains detailed guidance on eligibility. Some highlights include:

- Only companies are eligible

- Certain threshold criteria and exclusions on types of games apply

- Detailed inclusions and exclusions on eligible expenditure as set out in the legislation, with some categories not straightforward or easily defined.

Interesting quirks

With the new DGTO sitting in Tax Legislation (similar to the RDTI), there are certain areas that may appear to overlap with R&D Tax and general tax principles.

A few notable points include:

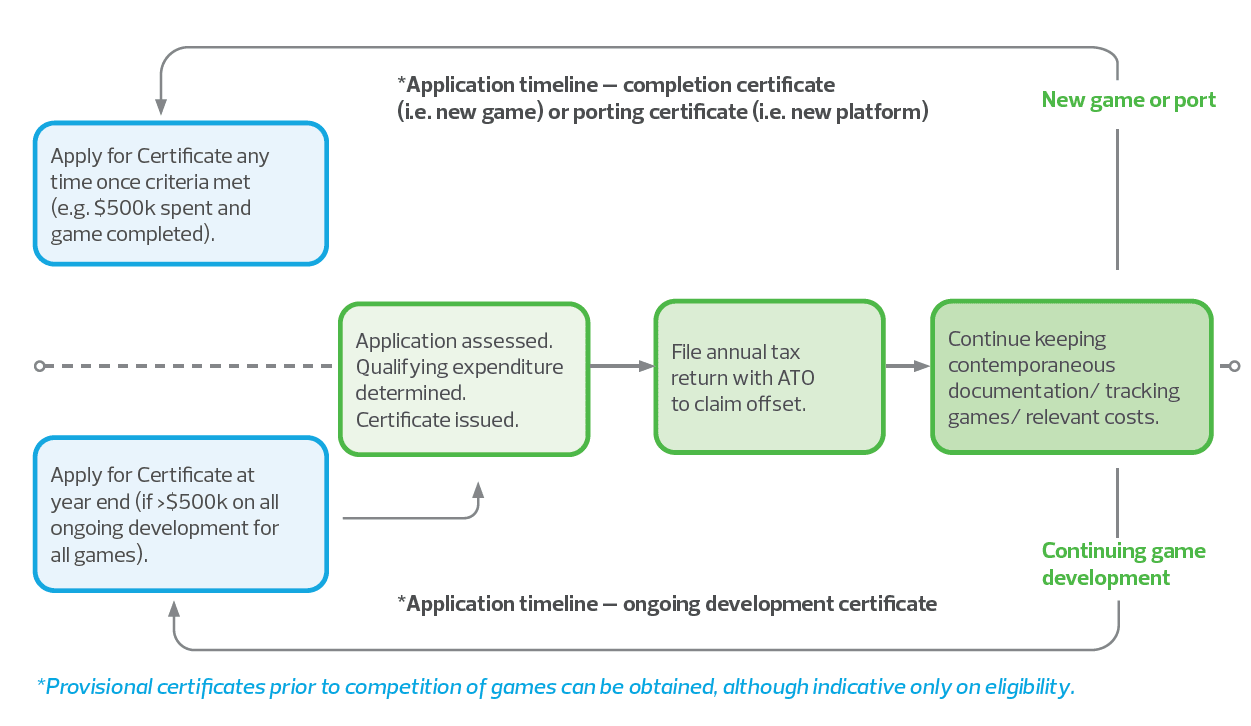

- The ongoing development certificate appears to be broad and can relate to items such as ongoing bug fixing on released games.

- Eligible costs and application timelines may be different (e.g. NSW rebate only counts expenditure after application, whilst the DGTO applies to historical spend), therefore planning is key.

- Any expenditure that has been excluded from the DGTO may be eligible for RDTI. Modelling should be done to optimise immediate and medium-term benefit.

FOR MORE INFORMATION

If you would like to learn more about the new digital games tax offset, please contact Peter Xi, Jessica Olivier or Simon Harcombe.

Click here to download a PDF version of this article.