Innovation is a key factor for sustainable growth and competitiveness in organizations, but its success depends not only on creativity or the implementation of new technologies, but also on the ability to measure its economic impact. The Return on Investment in Innovation (ROIi) is an essential metric for evaluating the profitability of innovative projects, helping companies to justify their investments and optimize the allocation of resources.

This innovation ROI measurement model considers not only tangible benefits, such as revenue growth and cost reduction, but also other key factors such as productivity improvement and market share expansion. It also incorporates a risk and time adjustment factor, recognizing that innovation involves uncertainty and that its benefits may materialize in the medium or long term.

The present proposal designed by RSM based on Dodgson, M., Gann, D. M., & Phillips, N. (2014) and OECD & Eurostat. (2018), establishes a structured methodology based on quantifiable indicators that allow organizations to assess the financial impact of innovation, facilitating strategic decision making. By implementing this model, companies can optimize their innovative initiatives, identify opportunities for improvement and maximize the value generated through digital transformation, product development and internal process optimization.

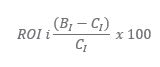

General formula of the ROI of innovation (ROIi):

Where:

- ROIi= Return on investment in innovation (%).

- BI = Benefits of innovation (additional revenue, cost reduction, impact on productivity)

- CI= Total costs of innovation (R&D investment, product development, implementation costs)

The ROI of innovation measures how much value an investment in innovation generates in relation to its cost. If the result is positive, it means that the innovation has generated more value than it has cost.

General formula for ROI of innovation (ROIi):

Model Components

1. Benefits of Innovation (BIB_IBI)

The impact of innovation on the organization can be expressed in terms of:

Where:

• IN = Increased revenues from new products or services.

• RC = Reduction in operating and production costs.

• PA = Increase in productivity (measured in efficiency or reduction in work time).

• MC = Market share improvement (impact on future sales due to innovation).

2. Costs of Innovation (CIC_ICI)

The cost of developing and implementing the innovation is expressed as:

CI=ID+CT+CI+MA

Where:

• CI = Investment in R&D (Research and Development).

• CT = Technology costs (acquisition of software, hardware, digital platforms).

• CI = Implementation costs (training, integration into existing processes).

• MA = Costs associated with maintaining and updating the innovation.

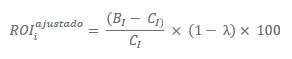

Adjusted Model with Time and Risk Factor.

To reflect uncertainty and time in the calculation of the return on innovation, we can use a discount factor (λ\lambdaλ) that considers risks associated with the implementation:

Where:

λ = Risk factor (varies between 0 and 1, where 0 means no risk and 1 is total risk).

This factor is based on the probability of success of the innovative project, obtained by historical analysis or benchmarking.

Example of the calculation:

A company invests $500,000 in new automation software. As a result, it obtains:

- Increase in revenue: $300,000

- Cost reduction: $200,000

- Productivity improvement equivalent to: $100,000

Los costos de la innovación incluyen:

• Inversión en I+D: $200,000

• Costos tecnológicos: $150,000

• Costos de implementación y capacitación: $100,000

• Mantenimiento anual: $50,000

Calculamos

BI = 300,000 + 200,000 + 100,000 = 600,000

CI = 200,000 + 150,000 + 100,000 + 50,000 = 500,000

Si el factor de riesgo (λ) es del 10%, el ROI ajustado sería:

Este modelo permite medir de forma estructurada el impacto financiero de la innovación en una empresa. Puede adaptarse a diferentes sectores y tipos de innovación, considerando tanto beneficios tangibles como intangibles. [1]

[1]Bibliografía

Dodgson, M., Gann, D. M., & Phillips, N. (2014). The Oxford Handbook of Innovation Management. Oxford University Press.

OECD & Eurostat. (2018). Oslo Manual 2018: Guidelines for Collecting, Reporting, and Using Data on Innovation. OECD Publishing.