Tax treatment of real estate income

Rental income

Individuals

Introduction

Interest income is taxed in income tax as business income (box 1) or as investment income (box 3).

Liability to tax

Rental income received by individuals is subject to personal income tax.

Basis to tax

The income of individuals is divided into three ‘boxes,’ each with different tax rates.

In box 1, income from employment and homeownership is taxed, including income from employment and business income derived from entrepreneurship. If interest income qualifies as business income, it is taxed in box 1. Box 1 applies a progressive tax rate, reaching up to 49.5%. Interest income qualifies as business income if an individual engages in a certain level of labor or entrepreneurial activity. In practice, this means that real estate held purely as an investment (for rental purposes) without active involvement by the individual is taxed in box 3.

In box 2, income derived from holding at least 5% of the shares in a legal entity is taxed. This includes dividends (regular benefits) and capital gains (disposal benefits) realized upon the sale of shares.

When a legal entity rents out real estate and distributes the income as dividends to its shareholders, this income—after being taxed at the corporate tax level—is taxed in box 2 at the shareholder level. Box 2 applies a two-tier tax system, with a basic rate of 24.5% on the first €67,000 and a top rate of 31% on the excess.

In box 3, income from savings and investments is taxed, where the actual (interest) income received may not be relevant. This is because box 3 is based on a deemed return rather than actual earnings.

The deemed return rates for 2025 are divided across three types of assets:

- Bank and savings deposits and cash: 1.44%*

- Investments/other assets: 5.88%

- Debts: 2.62%*

*Concerns preliminary deemed return rates for 2025.

The tax due in box 3 is determined by deducting the deemed return on your debts (3) from the deemed return on your assets (1 and 2). The value of real estate assets (on which the fictive return is calculated) is based on the WOZ value, which is determined annually by the municipality where the real estate is located. The deemed return on your assets minus the deemed return on debts is taxed at a flat rate of 36% in 2025. Additionally, the tax-free allowance in box 3 must be considered. In 2025, the tax-free allowance is €57,684 for a taxpayer without a fiscal partner and €115,368 for a taxpayer with a fiscal partner.

The counterevidence scheme in box 3 allows taxpayers to prove that their actual return on assets is lower than the deemed return used by the Tax Authorities. If successful, the tax will be calculated based on the actual return instead of the deemed return. As of March 2025, it is known that the Tax Authorities will make a form available from summer 2025 to enable taxpayers to provide this proof.

However, the exact method for calculating the actual return according to this form is not yet known. The counterevidence scheme applies to tax years from 2021 onward.

Companies

Introduction

Rental income is taxed as corporate income.

Liability to tax

Rental income earned by companies is subject to corporate income tax as corporate income.

Basis to tax

Corporate income up to EUR 200,000 is taxed against a tax rate of 19%. For profits of more than EUR 200,000 are taxed against a tax rate of 25,8%.

Capital gains

Individuals

Introduction

In principle, realized capital gains by individuals are not subject to income tax. Real estate is generally taxed under box 3, where a deemed return is taxed at a flat rate of 36%. (Un)realized capital gains may, however, play a role in determining the actual return in relation to the counterevidence scheme in box 3.

Liability to tax

Individuals are subject to income tax.

Box 1

In certain circumstances, realized capital gains by individuals may be subject to income tax in box 1. This applies, for example, when an individual engages in a certain level of labor or entrepreneurial activities. In such cases, the realized capital gain is subject to income tax in box 1, with a progressive tax rate of up to 49.5%.

Companies

Introduction

Capital gains realised by companies are subject to corporate income tax.

Liability to tax

Corporate income up to EUR 200,000 is taxed against a tax rate of 19%. For profits of more than EUR 200,000 are taxed against a tax rate of 25,8%.

Exemptions

Legal entities can, under certain conditions, defer taxation on capital gains by creating a reinvestment reserve (HIR). If reinvestment occurs within three years in a similar business asset, the value of the reinvestment reserve is deducted from the value of the new asset. As a result, future depreciation costs are lower, leading to higher taxable profits in later years due to the deferred tax liability. If reinvestment does not take place within three years, the reinvestment reserve becomes immediately taxable, without the possibility of further deferral through depreciation costs.

Dutch VAT & transfer taxes

VAT (Value-Added Tax)

Individuals who qualify as entrepreneurs for VAT purposes

Introduction

Value-added tax is a tax based on the increase in value of a product or service at each stage of the supply the chain.

Liability to tax

An entrepreneur who carries out a commercial or professional activity for a customer is, in principle, required to charge VAT to the customer. However, when a business or an independent part thereof is transferred, this is not considered a supply (transfer of a going concern).

Basis of tax

The supply and rental of real estate is, in principle, exempt from VAT. However, there are exceptions: the supply of new real estate (transfer within two years of initial use) and the supply of building land are subject to VAT. A special provision is the option for taxable rental/supply. The supplier and recipient can opt for VAT-taxed rental or supply of real estate. The applicable VAT rate is 21%. For standard residential rental, VAT can never be applied.

Interaction with transfer tax

If VAT has been charged by the seller in relation to the supply of new real estate or the supply of a building plot, the purchaser is not liable for transfer tax.

Companies

Within VAT regulations, no distinction is made between individuals (natural persons) and legal entities. The key criterion is entrepreneurship. As a result, the same rules apply to legal entities.

Transfer Taxes

Individuals

Introduction

Transfer tax is a tax on the transfer of real estate from one person or company to another. This also applies to limited rights to which real estate is subject such as leasehold or a right of superficies.

Liability to tax

Real estate transfer tax is due upon the acquisition of legal ownership or, subject to specific exemptions, the economic ownership of Dutch real estate. The buyer is responsible for paying the transfer tax.

Additionally, transfer tax is also due on the acquisition of a qualified interest in a so-called real estate entity (e.g., a private limited company (BV) holding real estate). A business qualifies as a real estate entity if at least 50% of its assets, based on market value, consist of real estate, of which at least 30% is located in the Netherlands. Furthermore, the company's primary activity must involve acquiring, selling, and/or operating real estate. This means that at least 70% of its activities must be focused on the acquisition, disposal, or exploitation of real estate.

For the transfer of real estate shares, a transfer tax rate of 4% or 10.4% may apply.

Basis of tax

The real estate transfer tax is calculated based on the market value of the property, which is at least equal to the sales price. The 2% tax rate applies to the transfer of residential properties if the buyer intends to use the property as their primary residence. The 10.4% tax rate applies to other real estate, including residential properties held as second homes or investment properties.

There is also a first-time buyer exemption in transfer tax. Individuals aged between 18 and 35 years who purchase a home with a maximum value of €525,000 can claim a one-time exemption, provided that the property will be used as their primary residence.

If a property is transferred again within six months, the tax base of the second transaction is reduced by the tax base of the initial transaction. This provides a tax advantage for the subsequent buyer.

Exemptions

There are various exemptions available. For example, an exemption from transfer tax applies to the acquisition of newly constructed real estate or a building site, in respect to which VAT (21%) is due. Furthermore, there are several exemptions related to (de)mergers and/or internal reorganisations. However, various detailed conditions apply.

Companies

No distinction is made between individuals (natural persons) and legal entities in real estate transfer tax. As a result, the same rules apply to legal entities.

However, legal entities, except for housing corporations, are subject to the 10.4% transfer tax rate on all real estate, including residential properties, except for real estate share transactions, where the 4% rate applies in specific situations.

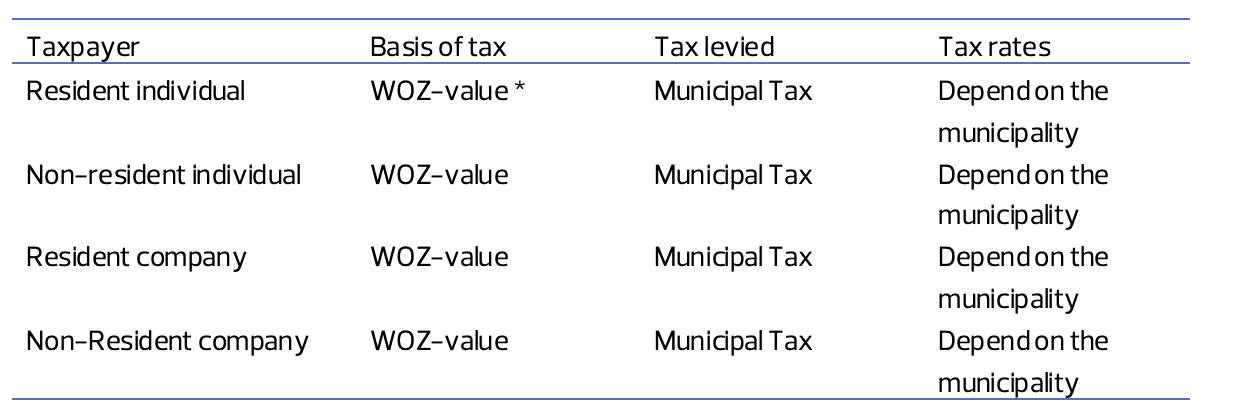

Dutch Local taxes

* There are specific rules for determining the WOZ value in relation to local taxes. Each municipality determines this value independently. An objection can be filed against the assessed value.

Introduction

Every municipality levies an annual municipal tax on Dutch real estate.

Liability to tax

Every owner or user of residential or commercial buildings in the Netherlands is liable to local municipal tax.

Basis of tax

The municipal tax is based on the WOZ value, which is determined by local authorities. For commercial real estate, the WOZ value is based on market value, but certain legally prescribed assumptions apply, which may cause the WOZ value to differ from the (economic) market value. Each municipality applies its own tax rate.

Dutch wealth tax / net worth tax

Individuals

The Netherlands does not have a wealth tax in a legal sense. Generally, when referring to wealth tax, it pertains to box 3 taxation. In box 3, a deemed return on a taxpayer’s assets is taxed based on annually determined return rates for bank deposits, debts, and other assets (such as real estate, shares, etc.). We refer to the previously discussed rental income section for a detailed explanation of this system.

Companies

The Netherlands has no wealth tax on assets of legal entities.

Vehicles for Dutch real estate

Commonly used vehicles for Dutch real estate

Corporate entities

The private limited company (BV) is the most commonly used business structure for owning real estate. The equity of the BV is divided into shares, and shareholders are, in principle, not personally liable for the company's debts.

Individuals who own 5% or more of the shares in a Dutch legal entity have a so-called substantial interest in the BV. Income derived from this substantial interest is subject to personal income tax (box 2) at a step-up rate of 24.5% on amounts up to €67,000 and 31% on amounts exceeding €67,000. Profits earned by the BV are subject to corporate income tax at a rate of 19% on taxable profits up to €200,000 and 25.8% on taxable profits above €200,000.

Transparent vehicles

Investments in real estate can also be made on a collective basis, involving both entities and individuals. The Netherlands does not distinguish between partnerships and joint ventures. In certain cases, a limited partnership (CV) or a general partnership (VOF) can be structured in a way that they are considered tax-transparent. When classified as transparent for tax purposes, the profits and losses of these entities are directly allocated to the underlying participants/partners. As a result, these participants/partners are not subject to dividend tax, which helps avoid taxation at multiple levels. Examples of transparent entities include the CV and the FGR (fund for joint account).

A CV must have at least one general partner and one limited partner. In principle, both CVs and FGRs are considered fiscally transparent. However, if a real estate investment CV or FGR qualifies as an investment institution under the Financial Supervision Act (Wft), it may be classified as non-transparent for tax purposes.

If the ownership in a real estate investment CV or FGR can only be transferred to the CV or FGR itself, it is considered fiscally transparent entity. Otherwise, barring additional conditions, it will be considered subject to corporate income tax.

Trusts

The concept of the trust is not known under Dutch law. For tax purposes, the assets and liabilities of a trust are allocated to the trustor as personal income. Profits realised by the trusts will be taxed by the trustor as personal income tax.

Foreign partnership

The residence of a partnership is determined by the place (country) where the decisions are made. Usually, the residence is the place where all partners meet.

In case a foreign partnership carries an enterprise in the Netherlands, the partnership is subject to Dutch corporate income tax or the partners are subject to Dutch personal income tax. The foreign partnership qualifies as a permanent establishment in the Netherlands by owning Dutch real estate. The partners are subjected to Dutch personal income tax.

Specific real estate vehicles for Dutch real estate

Under Dutch law, there are no specific real estate vehicles.

Fiscal investment institution

Before January 1, 2025, it was possible to invest directly in Dutch real estate through a Fiscal investment institution (FBI). The FBI is a special business entity designed for portfolio investments, which are not limited to real estate. The FBI is subject to various detailed conditions. Additionally, it must distribute its profits to shareholders within 8 months after the end of the financial year in which the profits were generated. Furthermore, no single shareholder may own more than 5% of the shares in an FBI.

The applicable corporate income tax rate for an FBI is 0%. However, dividends distributed by an FBI are subject to dividend tax.

From January 1, 2025, fiscal investment institutions (FBIs) can no longer invest directly in Dutch real estate. However, indirect investments in Dutch real estate or investments in foreign real estate remain permitted.

More information?

For more detailed information and questions please contact your trusted RSM advisor.