Private equity will remain active in 2023

As we look into 2023, it’s remarkable the types of mixed messages that one receives about private equity (PE) and whether this group of investors will be active or not.

Uncertainty over where the economy is headed is understandably delaying some decisions. The economic headwinds have suggested to some investors that they hold back on making offers until the prices of the targeted assets have come down, and the recent surge in the stock markets (the FTSE 100 reached an all-time high in early February) could suggest that corporates might be less pressured to sell some of their assets in order to shore up their balance sheets.

However, as was set out in our last market perspectives, about capital availability, there is a significant amount of capital available for private equity investors to deploy. Globally there is $1.2tn (near an all-time high) of what we call private equity ‘dry powder’ that must be deployed by these investors, and any slow down in their investment cadence could jeopardise their ability to invest all the funds that they have committed to do.

Also, as Warren Buffet once said, ‘A market downturn doesn’t bother us. It is an opportunity to increase our ownership of great companies with great management at good prices.’

In that context, we expect PE investors to continue to be active investors in 2023 and any companies seeking capital and strategic partners to navigate the current economic climate and make the most of the opportunities that it represents (there is always opportunity in a crisis!) should engage these potential partners.

Below are details of the types of investments we expect private equity to be making.

Going forward, the type of deals will remain the same in some respects…

Add-on acquisitions will continue as a key theme of the market

We expect that the high rate of acquisitions by PE-backed businesses, as discussed in this analysis of these deal types where it was shown that add-ons made up 72% of all PE buyouts in 2022 in the UK and even more in the US, will continue. There are three reasons behind this.

- The high levels of dry powder available that can be channelled via existing portfolio companies to make acquisitions.

- We are being increasingly approached by owner-managed businesses exploring an opportunity to realise their investment or partner with deep-pocketed strategic partners to help weather this economic storm. There are multiple reasons for this now, including that they need capital for expansion – or just to survive. Many simply don’t want to deal with another pandemic-style disruption, while others are looking for a private equity partner to enhance their resilience. This point is equally valid for platform/primary deals as owner-managed businesses can be sold as such.

- There are nearly 1,800 UK-based, PE-backed UK businesses that have been within a PE portfolio for three years or more – that’s 49% of the portfolio company base. Considering that PE’s typical holding period is three to five years, many of these companies will be seeking new backers and a sale to a PE-backed company is a key consideration.

Primary/platform deals continue to be a feature of the market, though volumes are declining

Our PE clients continue to pursue platform/primary acquisitions – these are buyouts where the PE firm makes an acquisition, and there is no pre-existing portfolio company which that business will be integrated into, i.e. buyouts that are not add-ons.

Their activity will be enabled by the dry powder pool they have available and because prices will be under pressure due to the weakened economy, which creates the motivation to make investments. In addition, we expect there to be fewer competitors for assets, as large, listed corporates, who are normally active acquirors, will be under pressure themselves so will have diminished capacity to make acquisitions.

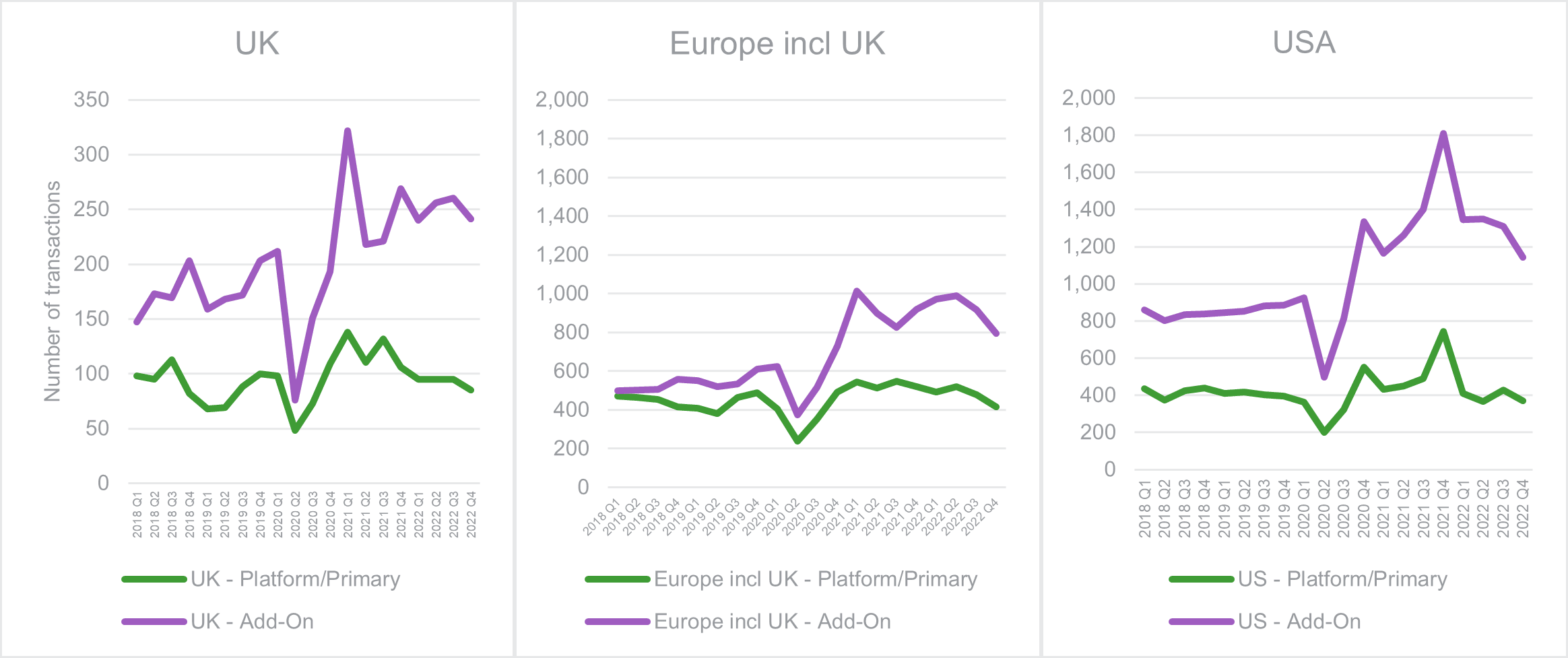

With that said, platform/primary-related activity has slowed due to a reduction in debt availability from banks and high interest rates, which are impacting the larger, typically more highly leveraged transactions. More on this can be found here. In the UK in 2022 Q4 there were 85 platform/primary deals, while the quarterly average in 2019 was 81, that’s a rise of 5%. Europe, including the UK, is slightly behind by 4%. The US is however down by 9% to 370 in 2022 Q4.

Companies that have identified acquisition opportunities, including competitors, or companies in upstream, downstream and/or adjacent markets should consider approaching private equity backers to use that company as an acquisition platform. Further, as was shown in our previous research on these deal types, PE firms have been paying higher valuations for businesses that they will go on a consolidation journey with.

PE buyout activity: Add-on acquisitions are a key component and remain ahead of pre-pandemic levels, while platform/primary transactions are slowing but steady

Source: PitchBook Data Inc, RSM UK. Note the different Y axis scale of UK vs Europe and USA

Summary of changes in number of PE buyout transactions: Pre-pandemic vs Latest Quarter

Source: PitchBook Data Inc, RSM UK

…and change in others

Pressured disposals of VC-backed businesses, or stakes therein

We are seeing Venture Capital (VC) backed businesses that are no longer able to draw in further capital from their existing funders. Multiple reasons are cited, including funds concentrating their dry powder on their most promising assets who still require significant capital before they reach break-even.

If these 'stranded’ businesses slow down their growth rate and focus more on preserving cash, they in effect become less suitable for the high risk/high return profile of a VC portfolio and more appropriate for PE backers. Those exits could be in full, or partial where PE takes a stake alongside VC in what is known as a growth capital investment. The latter is attractive for the incumbent shareholders as it still gives them access to future growth and upside and helps them realise some returns, while for the growth capital investor they have a lower exposure and other parties will share the burden of possible future capital needs. Private equity typically takes majority stakes so we expect most of these deals will involve a full exit by the VC firm.

Corporate carve outs, forced selling and reports of rapid sales are appearing

Listed and non-PE backed larger businesses are under pressure, as are their capital reserves due to the economic headwinds. While it’s too early to tell in transactions data, PE funds are expecting this to translate into increased carve-out disposals and take-privates. Off-market deals – accelerated transactions with only one buyer engaged – are set to rise too if companies are faced with unexpected shocks, e.g. the sudden loss of a key customer.

Emergence of distress and restructuring

PE firms will be keeping a look out for distressed sales. Sectors that are energy and people intensive and dependent on discretionary consumer spend will be the key source of these opportunities. Since the end of the first coronavirus lockdown in 2020, after which most economies were buoyant, there were few distressed assets coming to market – companies had access to low-cost debt and government support. The transition to a capital constrained environment represents a good opportunity for PE firms specialised in these types of deals as they have the capital and expertise to make a success of those investments.

As we head further into 2023, where companies will continue to face a host of economic challenges, we expect private equity to be an active space.

There will be some pressure on the sector with regards to further capital raising by funds which will negatively impact transaction volumes and amount deployed, however financial sponsors will still seek to deploy the significant and near-record levels of capital they have raised.

These investors will be making a variety of acquisitions, of profitable and growing companies through to distressed.

Companies seeking capital backing will experience competition for funding and will find themselves increasingly in a buyers’ market, but companies with strong and profitable prospects that have laid out a growth plan will be able to attract these professional and highly capable investors to enable that.

Looking to engage private equity investors but don’t know where to start?

Each private equity house has a unique investment appetite and approach, with preferance variances in areas like investment size, type of situation, sector, geography and percentage stake.

RSM is highly active in the private equity sector. We have a deep insight into and relationships with hundreds of private equity firms in the mid market, so please contact us to discuss the perfect fit for your needs.