Is the capital pool big enough to sustain private equity investment activity in 2023 and beyond?

Introduction

Notwithstanding the current economic headwinds, private equity funds look set to continue investing in 2023 and beyond. This is largely driven by the amount of capital the industry has to deploy.

This piece forms the second in a series looking at the private equity industry and how it is changing. The first article provides an insight into the types of transactions being undertaken, with a specific look at acquisitions by private equity-backed businesses, referred to as add-ons. The core message for owner-managed businesses in the first piece was that private equity could be a good partner if there’s an opportunity for industry consolidation, and that a company’s attractiveness will be bolstered if it has already identified targets to acquire.

In this second article, the take home message is that the considerable amount of capital available to be spent should be very welcome news for owner managed businesses.

A large private equity capital pool, ready to be deployed

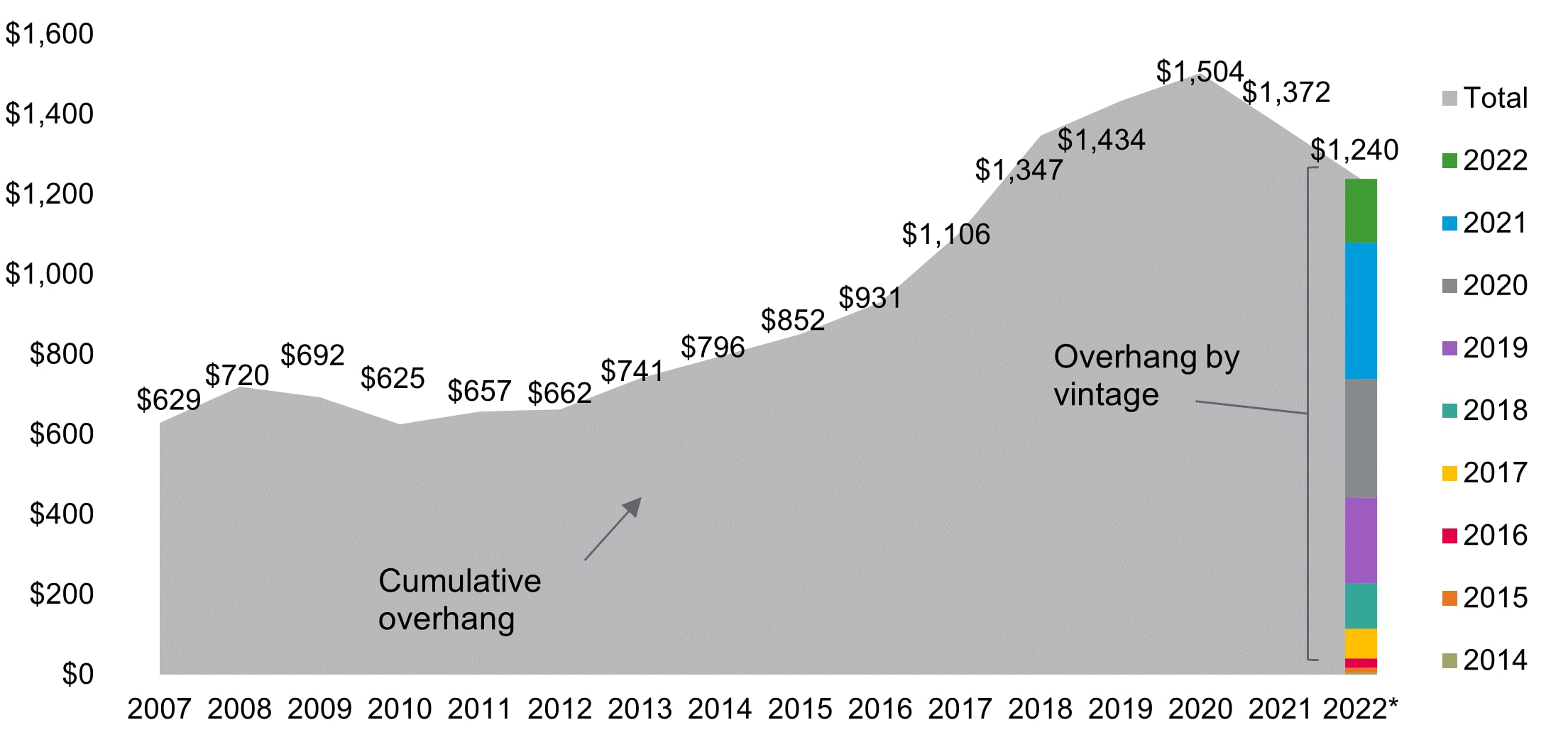

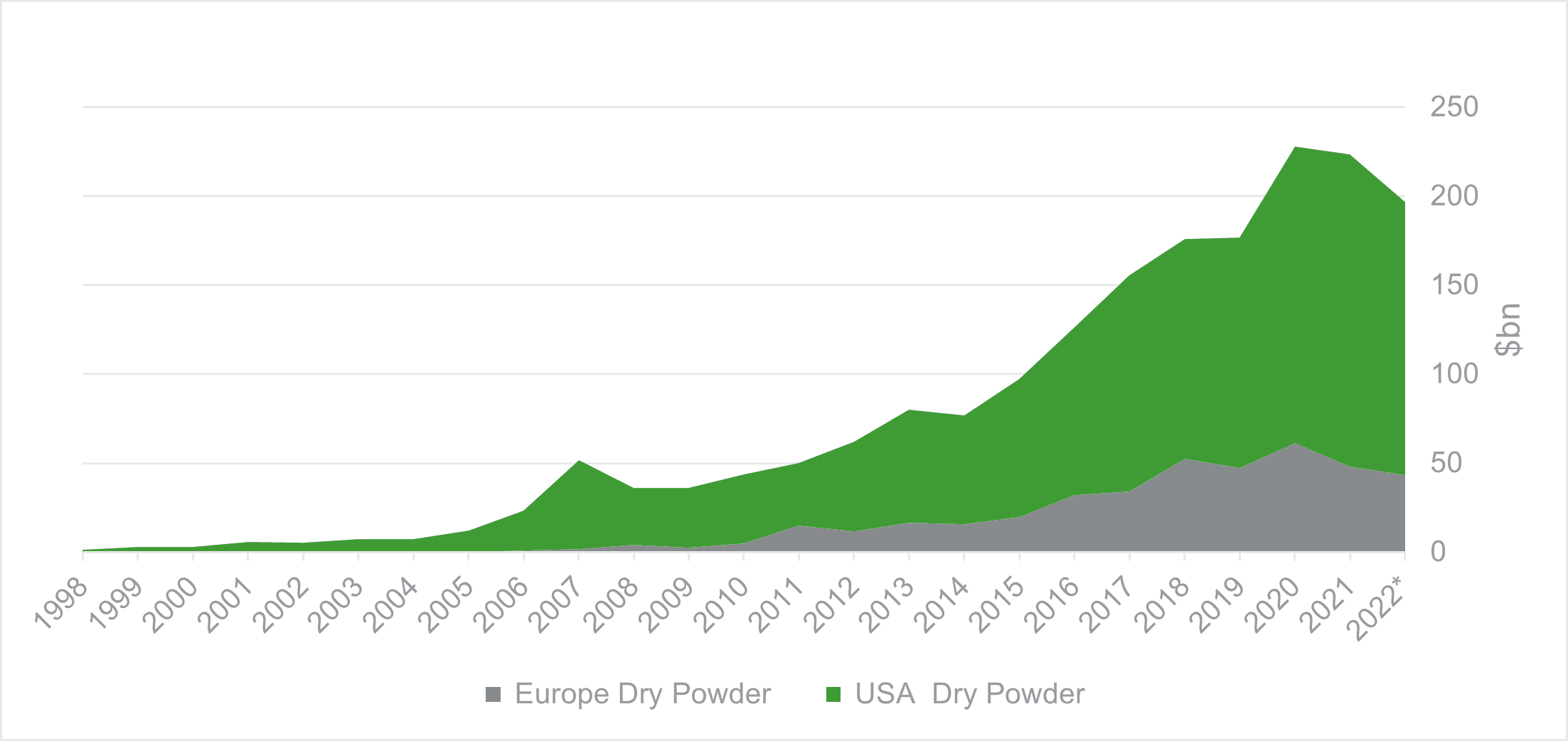

The levels of private equity dry powder - the capital that institutional investors have committed to private equity funds but has not yet been deployed into investments - are close to an all-time high, sitting at $1.24 trillion globally. The majority of this dry powder is located in the US (approximately $700 billion), followed by Europe (approximately $250 billion).

63% of the global pot has been raised since 2020. Considering that the typical ambition is to deploy funds within 3-5 years, with the proceeds returned typically within 10 years, the relative ‘youth’ of the pool will be reassuring to those involved in the private equity market. It is especially good news for companies seeking investment, as there are strong incentives for private equity firms to deploy capital, rather than return it uninvested.

To give context to how big this pool of capital is, we calculate that it would take approximately three years for that dry powder to be depleted, if no further fund raising occurs, which is unlikely (more of that below). Put another way, a meaningful investment purse will endure.

The dry powder pool is close to an all time high

Global private equity dry powder pool ($b)

Source: Pitchbook Data Inc, to 30 September 2022

Source: Pitchbook Data Inc, to 30 September 2022

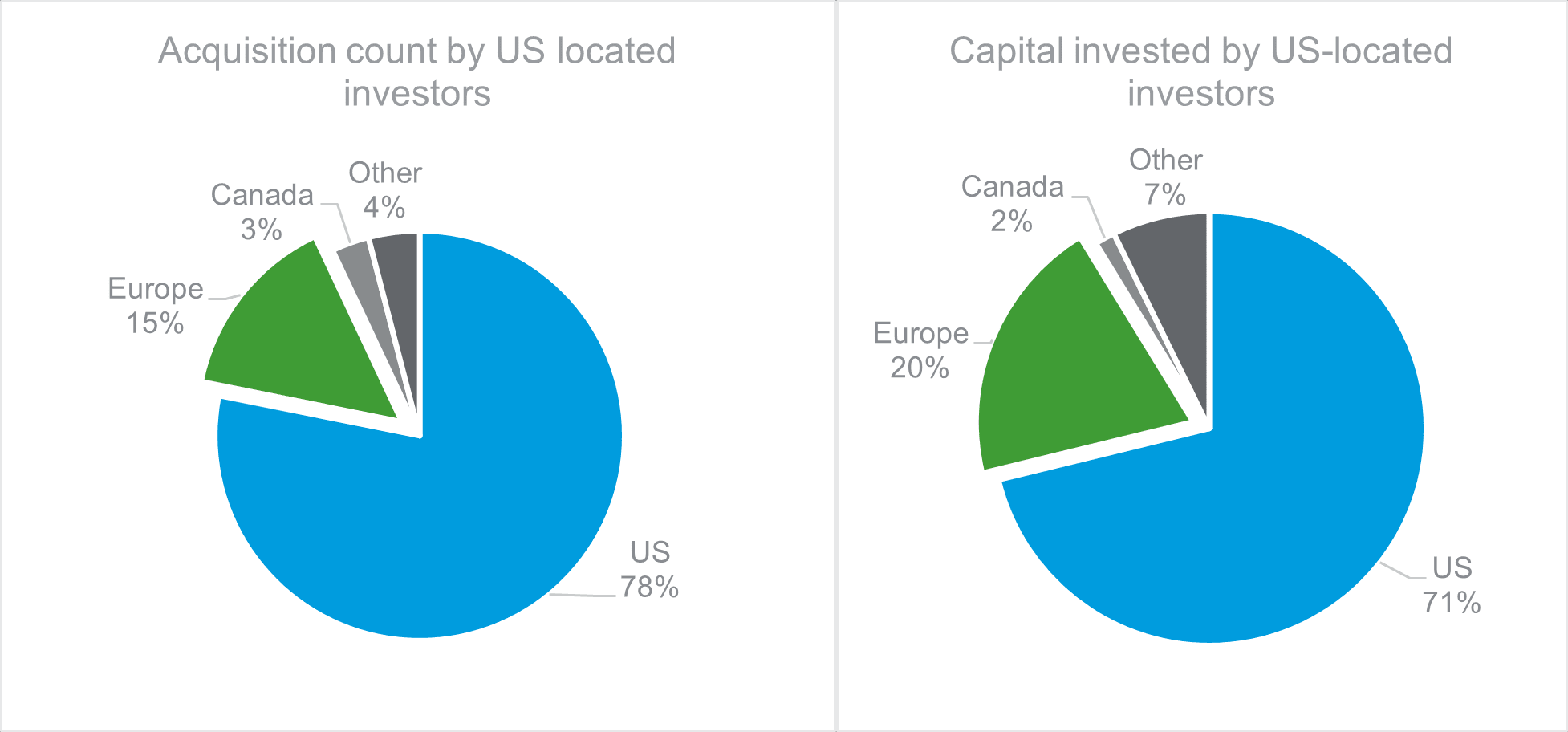

European companies have access to US based private equity capital

For European based companies considering whether they are disadvantaged by the lower capital pool they have access to, it’s worth bearing in mind that while US located funds will primarily invest in US based companies, they can, and do, invest elsewhere. From 2021 to Dec 2022, 15% of deals by count and 20% by value of acquisitions made by US based investors or their portfolio companies were based in Europe.

For European-based companies, this translates to them having access to a private equity capital base of over $300 billion.

US investors are active in Europe

Source: PitchBook Data Inc, 2021 to 5 Dec 2022

Private equity capital raising is continuing, but is slowing down

The sharp decline in public markets in 2022 meant that most investors could not increase or even maintain their investment allocations to private equity. This was exacerbated by the typical move away from illiquid assets, like private equity funds, during market turmoil.

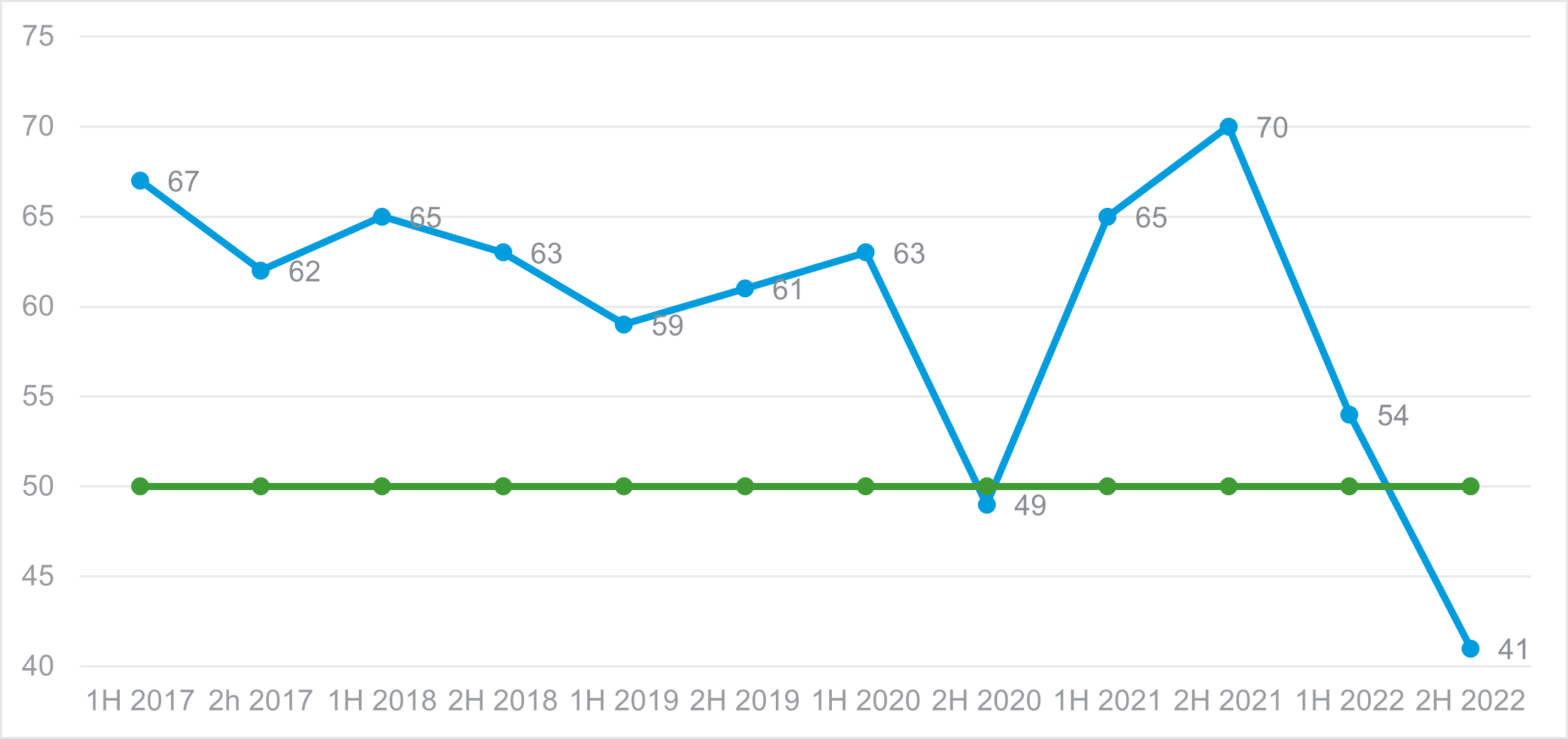

To illustrate, the REDE Liquidity Index, which tracks limited partners’ (institutional investors) sentiment towards private equity fund raising, i.e. how keen they are to invest in private equity, hit an all time low in H2 2022 of 41. A figure of 50 and above indicates the intention to invest more.

REDE Liquidity Index - Tracking Limited Partners’ sentiment towards Private Equity

Source: REDE, Nov 2022

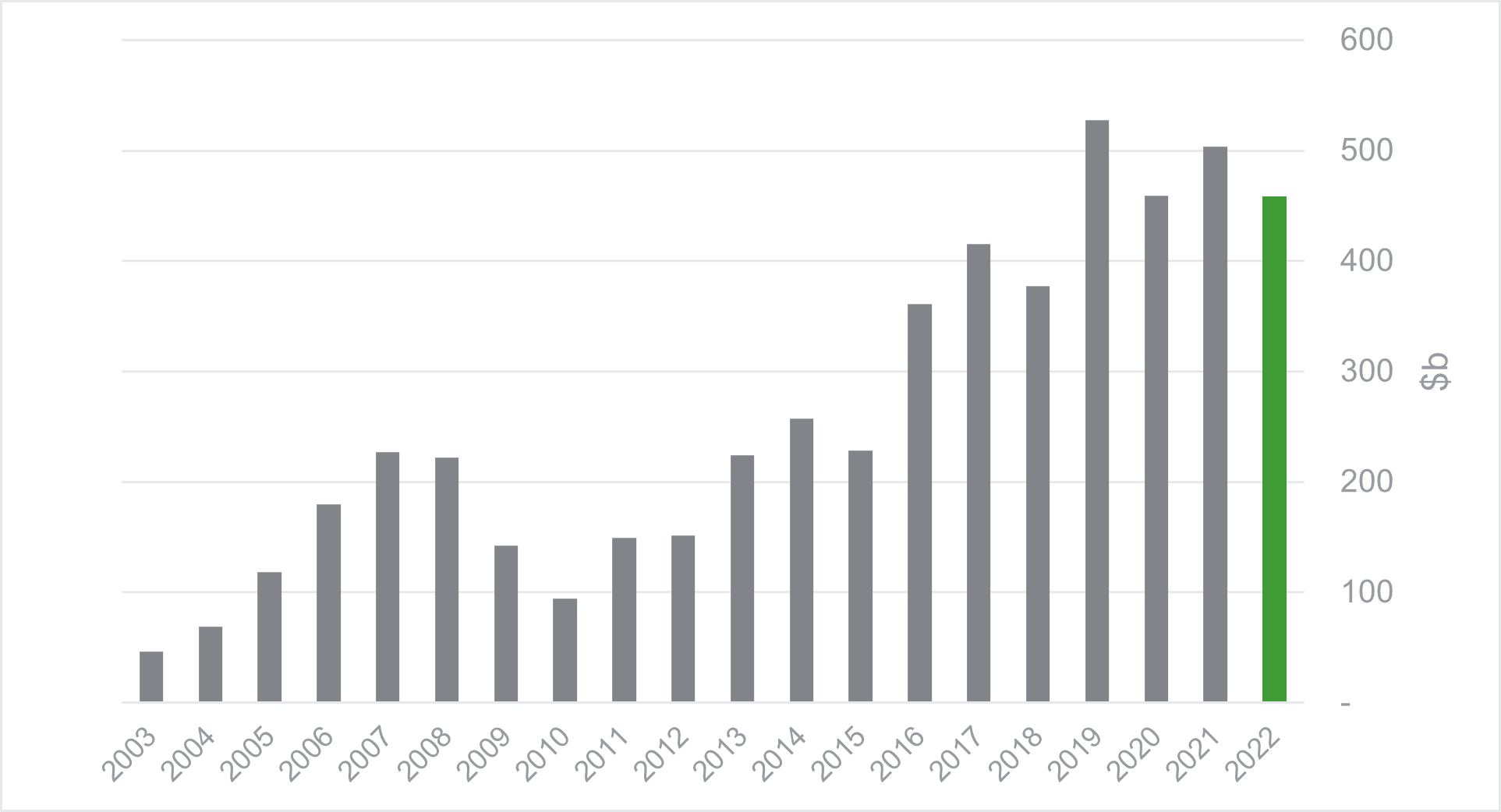

As a consequence, fundraising slowed in 2022, with a nine percent drop since 2021.

But, importantly, it was still close to the highest year in history, at $458 billion globally.

Private Equity fund raising (global)

Source: PitchBook Data Inc, 6 Jan 2023

Dry-powder runway to 2030, at least: Looping current fund raising activity back to the dry powder pool, which we said would last for three years if there was no additional fund raising, if we then include fund raising, even if it was just 50% going forward compared to 2022 (this is a low road scenario) and funds deployment continued at 2022’s pace (close to an all time high), then that dry powder pool would last as far forward as 2030.

Concentrated fund raising in 2022 – the gravitational pull of the largest funds

Resolving for the seeming discord between a weakening sentiment towards private equity and the relatively high levels of capital raised, this is, in part, a function of a lag in the impact of changes in sentiment on fund raising. Fund raising can take longer than 12 months and some processes would have started in 2021 when markets were stronger.

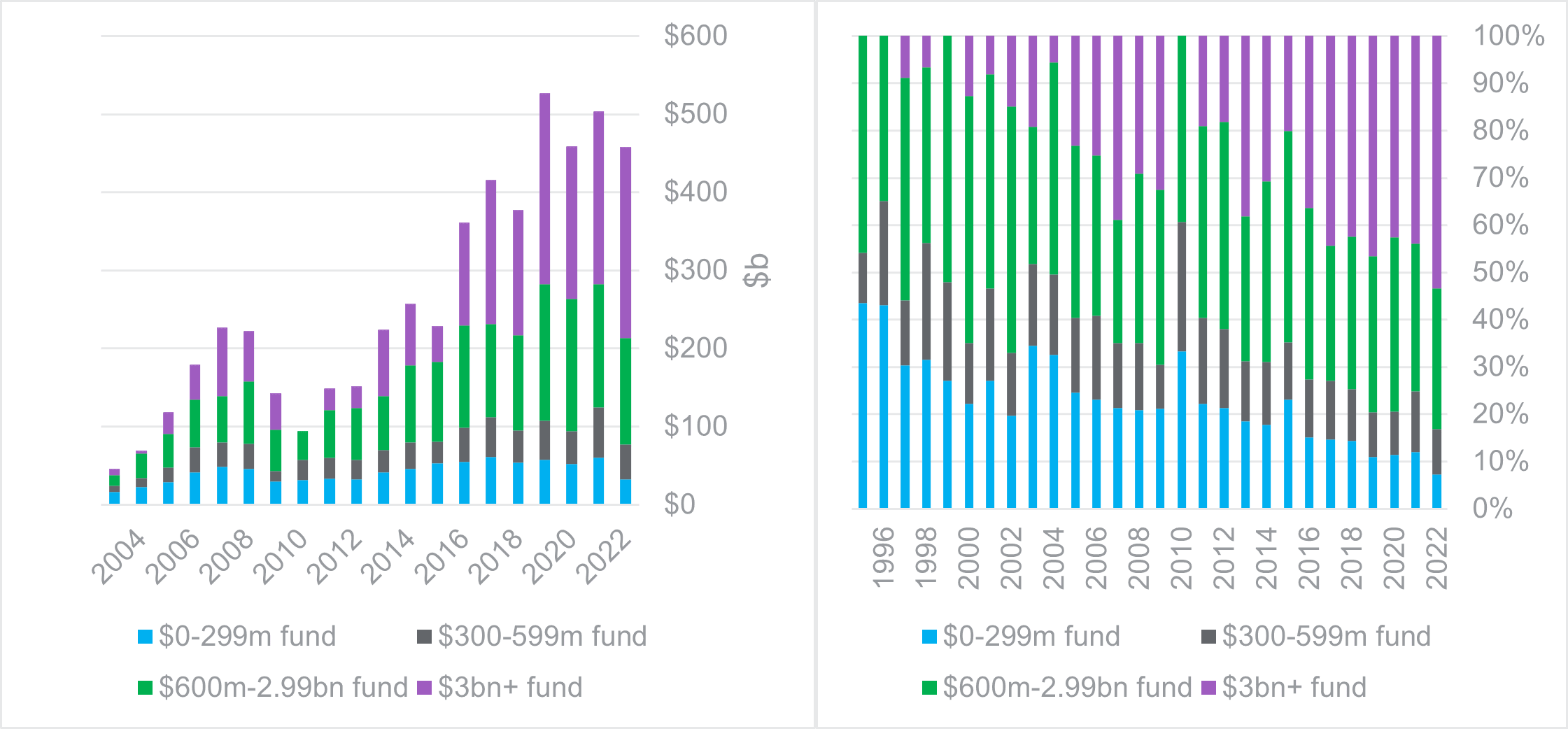

A further explanation lies in increasing concentration into the larger fund end of the market, at the expense of the smaller end.

The funds totalling $3 billion+ make up 53% by value of funds raised in 2022, an increase from 43% in 2021. Funds under $599 million only accounted for 17% of capital raised in 2022 compared to 25% in 2021.

Increased fund raising, and concentration into larger funds

Amount raised by different sized PE funds (Global)

Source: PitchBook Data Inc, at 6 January 2023

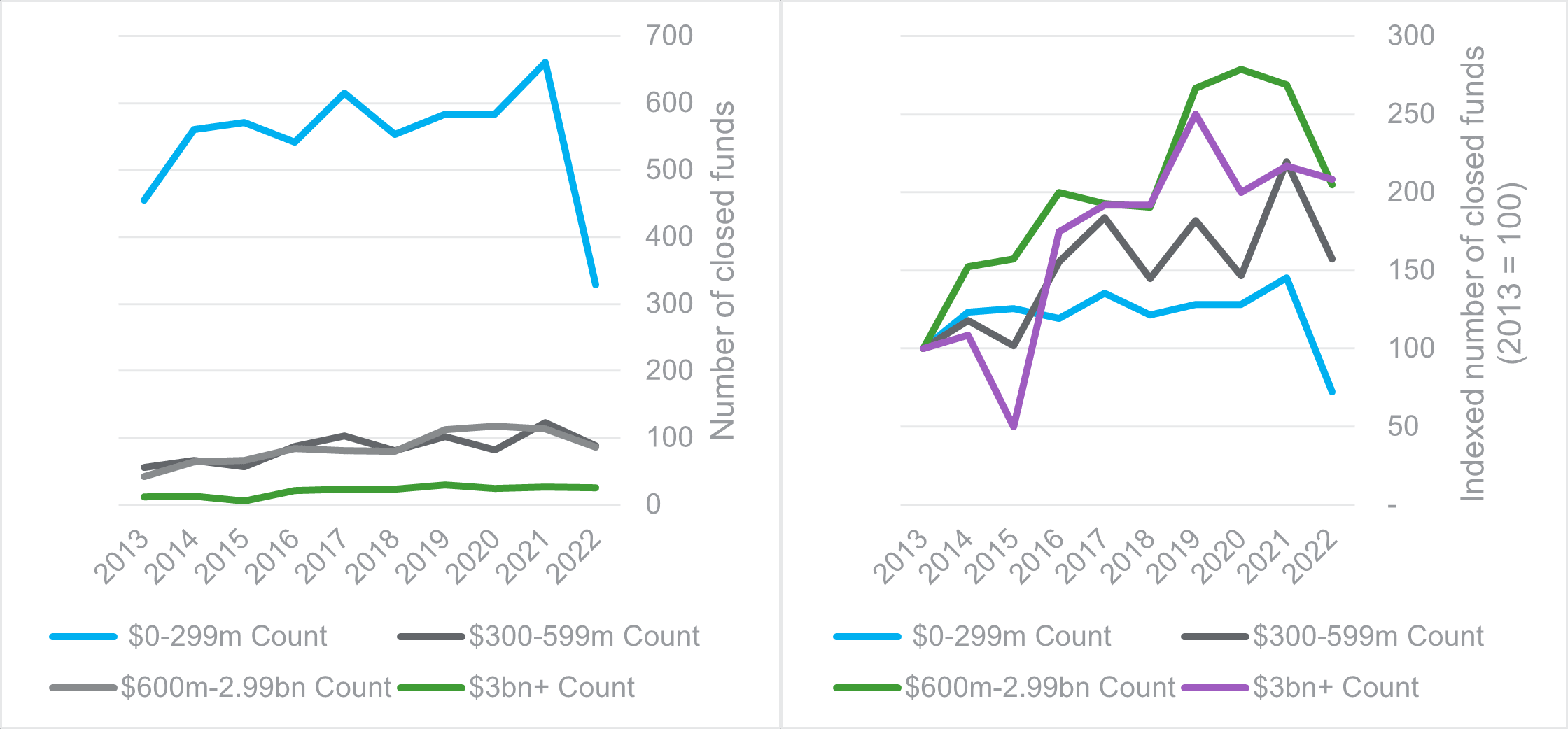

By number of funds closed, the lion's share is taken up by the smaller funds (62% accounted for by the $0-299 million cohort). However, all fund size groups saw a decline in the number of raised funds from 2021 to 2022, with the largest drop experienced by the smallest cohort of funds which went from 661 in 2021 to 328 in 2022 (50% down). The largest fund grouping ($3 billion+) reduced slightly from 26 to 25 (4% down).

Decline in number of funds raised in most fund sizes

Number of funds closed by different sized PE funds (Global)

Source: PitchBook Data Inc, at 6 Jan 2023

Summary of the changes for the different cohorts between 2021 and 2022:

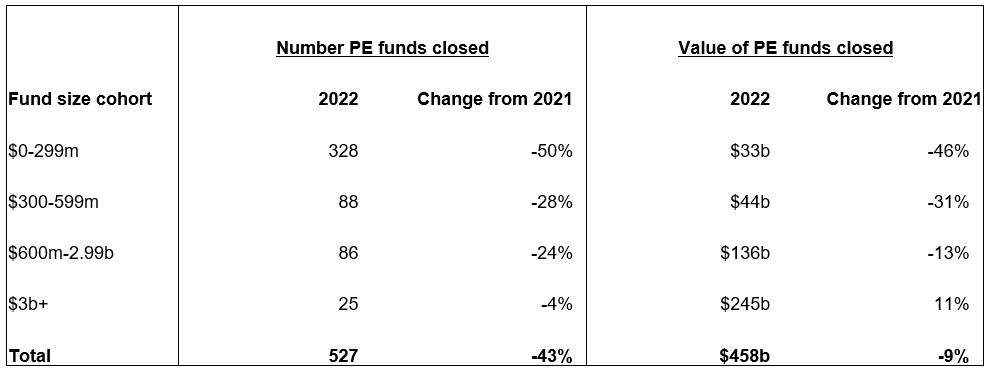

The larger the fund the lower the decline has been from 2021 to 2022

Summary of amount of PE capital raised and number of funds

Source: PitchBook Data Inc, at 6 Jan 2023. Analysis by RSM UK

Due to the lower levels of disclosure within private equity market vs. public markets, and in the smaller end in particular where the data is harder to collect, the data for those smaller funds might lag more or be less complete than the larger funds. These numbers are therefore subject to change.

Explaining the relative success in fund raising by larger funds

The concentration into larger funds during this ‘risk-off’ phase can be attributed to a range of factors, including their lower risk profile. There is a general understanding that small businesses are more risky than big businesses. So big private equity firms that invest in big businesses are lower risk than small funds that invest in small companies. Also, large private equity funds have all grown from being small firms – so are generally more established and stable organisations than small firms – and therefore lower risk in the eyes of an investor. To extend the theme, a first time venture capital fund is therefore the riskiest bet of them all.

It is also a function of the most efficient allocation of funds by the institutions. For example, according to Private Equity International, CALPERS (the California Public Employees’ Retirement System), which on average has deployed $12 billion per annum in private equity funds since 2018, has to deploy that capital in batches of at least several hundred million dollars – it would otherwise take too long and they can’t manage that many investments.

So, unless a mid market private equity fund is a top performer, e.g. in the top quartile, they will struggle to attract investment in the current climate compared to the larger funds with the same performance levels. This scenario is relevant during both buoyant or pressured fund raising environments, but is exacerbated when there’s heightened risk.

For any company engaging with private equity investors, it’s key that they understand each potential partner’s:

- Historical fund performance;

- Dry powder pool; and

- Prospects for future fund raising. These are among the key ingredients for the success of a PE fund and can effect their ability to support their portfolio companies.

Private debt becomes a key capital pool

Before the 2008 financial crisis fundraising by private debt funds barely existed, especially in Europe. The private debt dry powder pool is now close to an all-time high, at $153 billion and $43 billion in USA and Europe respectively.

Private Debt dry powder is close to an all time high

Source: PitchBook Data Inc. Comprised of Debt - General; Direct Lending; Credit Special Situations; Distressed Debt; Fund Status: Closed Funds. At 5 Dec 2022

Borrowing from private debt funds, as opposed to bank debt, typically offers higher leverage capability, a bullet maturity and more flexibility around both financial and non-financial covenants. For larger companies, borrowers are additionally attracted to private debt as there is a speed and certainty of access that is limited with public markets, where volatility can negatively impact capital availability.

Companies engaging with private equity should expect that leverage will continue to be a key component of the deals, but that the source of the debt and the nature thereof will be different to that from most banks.

The cost of debt has risen, but alternative arrangements are being made

The rise in the cost of debt has impacted the investment thesis of many private equity deals as many of these deals, especially the larger ones, are highly leveraged in order to maximise equity returns. This will impact the number of transactions undertaken. Already there are reports of abandoned deals, such as Darktrace which was to be delisted by Thoma Bravo in September 2022. But many deals will remain viable by using different debt products, especially considering that mid market sized deals are typically less leveraged than larger ones, or use no debt at all.

While all-equity deals are common in the smaller end of the private equity market, and for distressed assets, they have traditionally been almost unheard of in the larger end. According to Bloomberg there were at least five such deals in the last few months of 2022, with Francisco Partners, Thoma Bravo and Stonepeak Partners cited as the investors doing these types of deals. For example, KKR’s acquisition of French insurance broker April Group announced on 25 Nov 2022 for €2.3 billion.

We are also starting to see different deal structures used, in order to reduce risk in the context of lower returns. Examples include some of the consideration being contingent on future milestones and/or deferred over a period rather than immediately on Day 1.

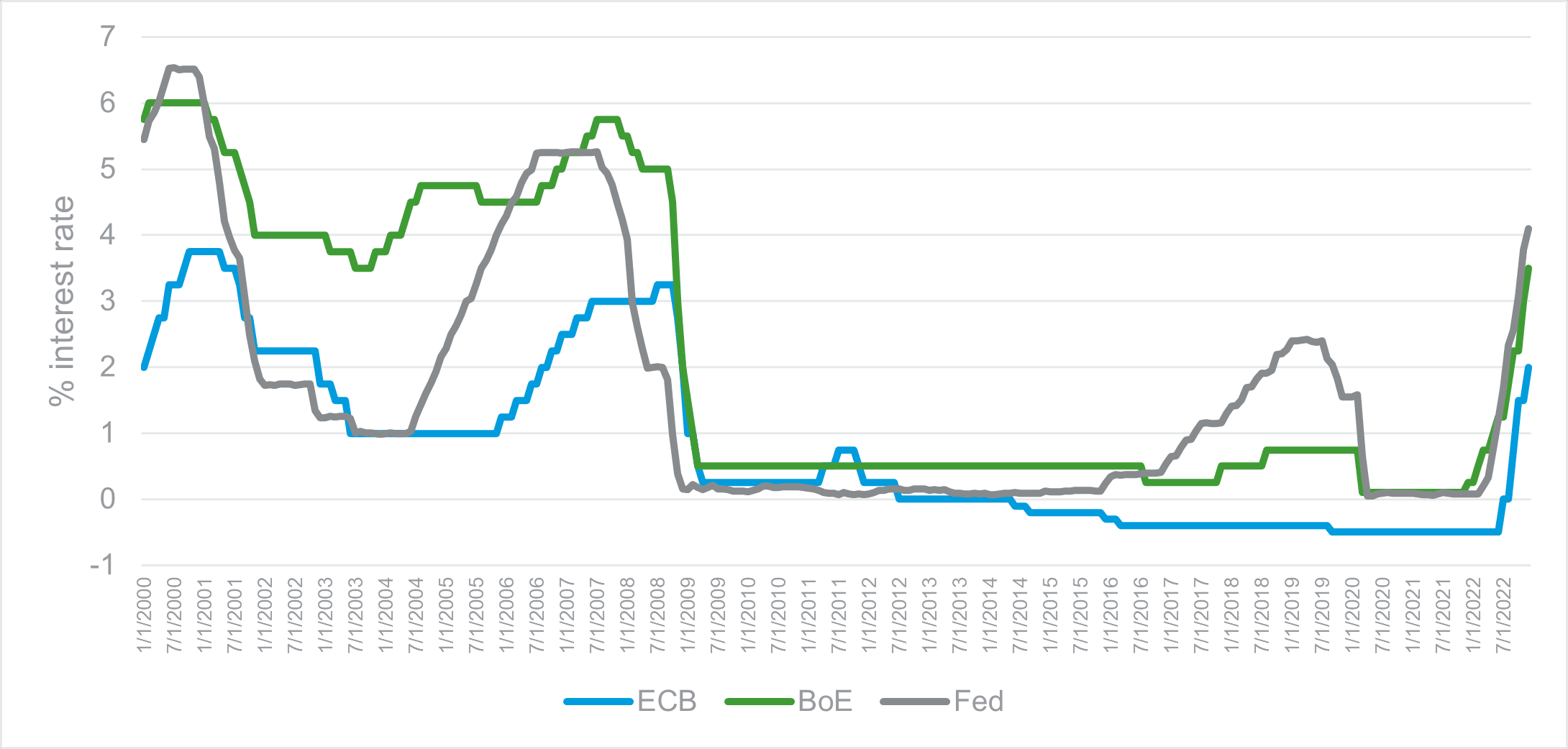

Another way to look at this is to adjust expectations of what good returns look like. One could argue that returns were hyper inflated by the low cost of capital that has prevailed during the era of quantitative easing, and that we are now back to ‘normal’.

Central bank interest rates moving back to ‘normal’?

Source: Bloomberg, to 31 Dec 2022

As we enter 2023, even with its host of economic challenges, private equity should continue to be an active space.

There will be pressure on the sector with regards to further capital raising by funds, especially the smaller funds, and supporting debt, which will negatively impact transactions volumes and amounts invested. However, financial sponsors will still seek to deploy the significant and near record levels of capital they have raised and will be creative in structuring deals to do so.

Companies seeking capital backing will experience competition for that funding and will find themselves increasingly in a buyers market, but companies with strong and profitable prospects, that have laid out a growth plan and are open minded to the terms of the deal will be able to attract these professional and highly capable investors to enable that.