On November 3, 2022, the Dutch State Secretary of Finance published a new decree (“Decree”) on the interpretation of the Dutch anti-hybrid rules ("ATAD2"). This Decree addresses, amongst others, a specific overkill situation resulting from the Dutch implementation of ATAD2, which mainly impacted certain specific US groups with cost-plus structures including companies in the Netherlands.

With this Decree the State Secretary of Finance provides the long-awaited guidance on the interpretation of ‘dual inclusion income’ in the context of ATAD2, especially in respect of cost-plus remuneration structures with US Corporations paying such remuneration to Dutch entities (BVs) which have elected to be treated as disregarded entities for US tax purposes (and whereby no blocker entities are interposed).

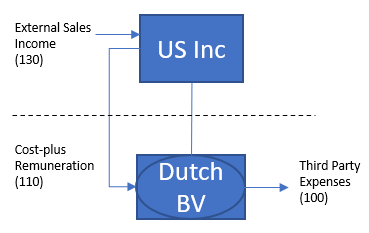

- It is now reasoned by the State Secretary of Finance that the Cost-plus Remuneration in this case should be considered as ‘double inclusion income’ in the context of this legislation as:

- the Third Party Expenses of BV (100) are double deducted both in the Netherlands and US,

- the limitation in deduction of the 100 would lead to double taxation, namely the External Sales Income at the level of US Inc. (130) is taxable in the US and the Cost-plus Remuneration (110) is taxable in the Netherlands at the level of BV,

- the Cost-plus Remuneration (110) paid by US Inc is not deductible for US tax purposes and this Cost-plus Remuneration is taxable in the Netherlands.

- Consequently, the Third Party Expenses of BV (100) should not be limited in deduction at BV level due to the application of the ATAD2 legislation. As a result, such structures could remain in place as the outcome should be in line with the objectives pursued.

The above interpretation applies as from January 1, 2020.

We would be happy to discuss the potential impact / benefit of this new Decree for your structure.