The relevance of Environmental, Social, and Governance (ESG) factors for both companies and governments has significantly increased in recent years, driven by growing stakeholder expectations and an evolving regulatory framework. Taxation, once primarily a matter of compliance, is now recognized for its strategic role in achieving sustainability objectives.

Investors, regulators, employees, and the public are increasingly scrutinizing companies' tax practices as a measure of social responsibility and good governance. This article analyses the role of environmental and green taxes, with a specific focus on European, and particularly Dutch, tax legislation, as concrete examples of how these divergent approaches manifest in policy measures.

This article is written by Dick Brinkhof ([email protected]) and Mario van den Broek ([email protected])). Dick and Mario are part of RSM Netherlands Tax, with a focus on International Tax and Global Tax Policy.

Tax policy has become a crucial instrument for promoting ESG goals, particularly in the environmental sphere, through both incentives and disincentives. Taxation serves as a tangible demonstration of a company's commitment to ESG principles, with financial mechanisms driving behavioral change. The current geopolitical context is marked by divergent approaches. The European Union (EU) is focused on the legally binding goal of climate neutrality, while the United States (US), with its "Make America Great Again" agenda, has historically leaned towards deregulation and prioritizing national economic interests, potentially at the expense of environmental protection. These differing geopolitical perspectives lead to varying regulatory frameworks for companies operating in both regions, increasing the complexity of aligning ESG and tax strategies on a global scale.

2. Understanding the Interplay Between ESG and Taxation

Tax policy can significantly influence various aspects of ESG. Environmentally, taxes on carbon emissions, incentives for renewable energy, and levies on pollution or resource use can encourage sustainable behavior. Environmental taxes operate on the principle that the polluter pays, internalizing the external costs of environmental damage into corporate decision-making. By increasing the cost of polluting activities, companies are incentivized to adopt cleaner technologies and practices, contributing to ecological sustainability.

Socially, tax benefits for companies promoting diversity and inclusion, incentives for employee well-being, and the contribution of corporate tax to society play a role. Taxation is recognized as a vital mechanism for companies to contribute to the societies in which they operate, fostering trust and social responsibility. Paying a "fair share" of taxes is increasingly viewed as a societal responsibility, supporting public services and infrastructure that benefit the community.

In terms of governance, relevant aspects include measures for tax transparency, codes for tax management, and the alignment of tax strategy with overall corporate values. Transparency in tax matters builds stakeholder trust and is considered integral to good corporate governance. By openly communicating tax policies, payments, and structures, companies demonstrate a commitment to ethical behavior and responsible financial management, enhancing their reputation.

We conducted extensive research, and various authors emphasize the symbiotic relationship between taxation and ESG. Ignoring this connection could be a detrimental strategy. Taxation is poised to become a crucial element within ESG, gaining increasing attention from stakeholders and acting as a powerful policy tool.

The socioeconomic and legislative landscape is shifting towards greater emphasis on tax transparency and sustainable tax practices, making taxation an integral part of the ESG agenda.

The growing importance of tax transparency within the broader ESG reporting landscape is driven by legislative changes, such as the EU's public Country-by-Country (CbC) Reporting Directive and voluntary disclosure frameworks. ESG reporting offers an opportunity to redefine tax reporting as a positive contribution to society, thereby strengthening trust and extending a company's purpose beyond mere compliance. By publicly disclosing their tax footprint and strategy within an ESG context, companies can provide a more complete picture of their societal role and build stronger stakeholder relationships.

3. The European Union's Commitment toClimate Neutrality: A Tax-Driven Approach

The European Green Deal is an ambitious plan aiming to significantly reduce greenhouse gas emissions and achieve climate neutrality by 2050, with interim targets for 2030 and 2040. The EU's commitment to climate neutrality is a legally binding objective, requiring a comprehensive and integrated approach with various policy instruments, including taxation. The European Climate Law enshrines the net-zero emission goal, providing a strong mandate for developing and implementing supportive policies, including green taxes. The EU has implemented several key legislative instruments for green taxation.

- The Energy Taxation Directive is currently under revision to better align with climate and energy objectives, aiming to link tax rates to energy content and CO2 emissions and reconsider exemptions for aviation and maritime transport. The revision indicates the EU's intention to modernize its energy tax framework to more effectively stimulate environmentally friendly behaviour across all sectors. Recognizing the limitations of the current directive, the EU aims for a more coherent and impactful energy taxation system that supports its climate goals.

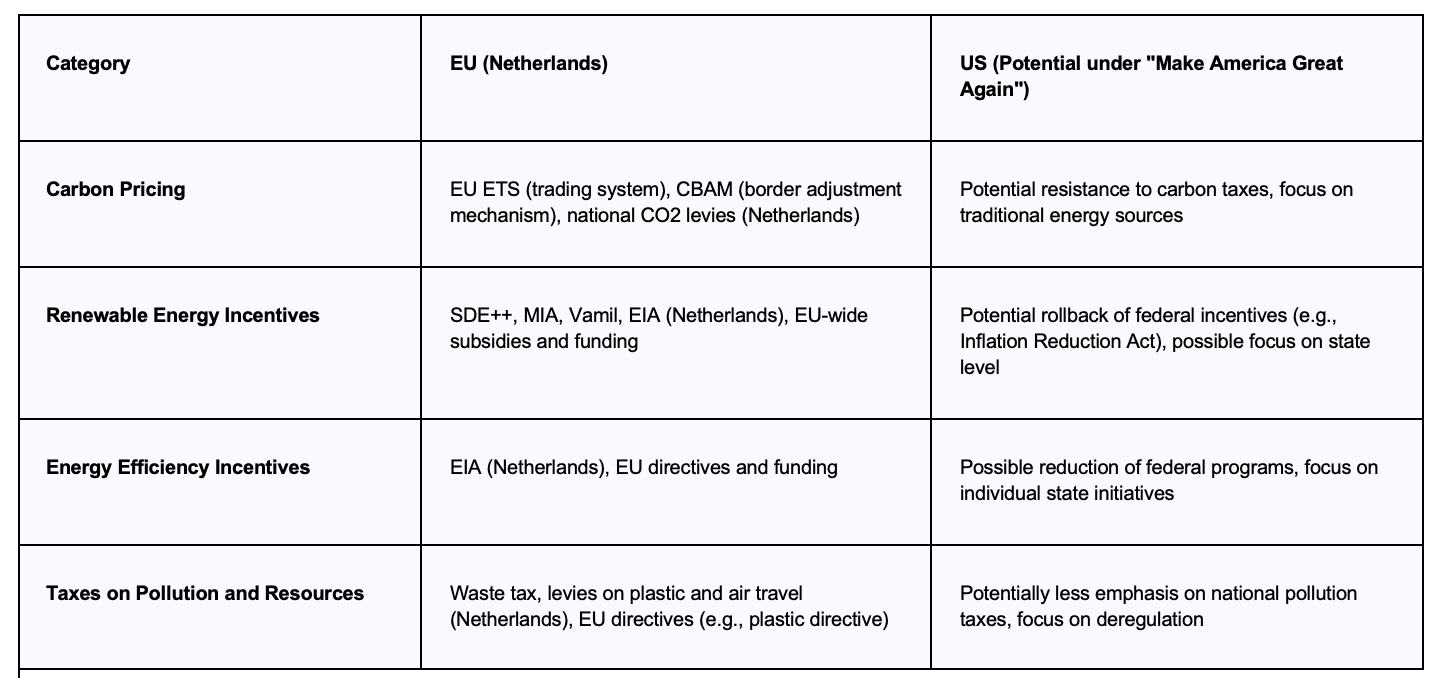

- The EU Emissions Trading System (EU ETS) is a cap-and-trade system for greenhouse gas emissions from energy-intensive industries and power generation, being expanded to other sectors. The EU ETS creates a carbon price, incentivizing emission reductions by making pollution more expensive and rewarding investments in cleaner alternatives. By limiting the total allowed emissions and permitting the trading of emission allowances, the ETS establishes a market-based mechanism to promote decarbonization.

- The Carbon Border Adjustment Mechanism (CBAM) imposes a levy on the embedded carbon emissions of certain imports from countries with less stringent climate policies, aiming to prevent carbon leakage and stimulate global climate action. CBAM represents a significant step towards ensuring a level playing field for EU companies and promoting higher global climate ambitions by addressing the risk of carbon leakage. By applying a carbon price to imports, the EU intends to encourage producers in other countries to reduce their carbon footprint.

Other relevant EU initiatives include the EU Taxonomy, a classification system defining environmentally sustainable economic activities and including tax compliance as a minimum safeguard. The EU Taxonomy links tax behavior to the definition of sustainable investments, emphasizing the importance of responsible tax practices for achieving environmental objectives. By setting criteria for ecologically sustainable activities, the taxonomy guides investment decisions and promotes transparency in green finance. The Corporate Sustainability Reporting Directive (CSRD) expands the scope and requirements for sustainability reporting by companies operating in the EU, including tax-related information. CSRD mandates greater transparency on a wide range of ESG factors, including taxation, making companies more accountable to stakeholders for their sustainability performance. By requiring comprehensive and standardized sustainability reporting, CSRD aims to improve the availability and comparability of ESG information.

4. Netherlands: An In-Depth Analysis of National Environmental Taxes and Green Taxes

The Netherlands has implemented specific tax measures to promote environmental sustainability. The SDE++ (Stimulering Duurzame Energieproductie en Klimaattransitie) scheme provides subsidies for large-scale renewable energy and CO2 reduction projects. The Spring Memorandum indicates that the government expects it will likely be possible to open the SDE++ subsidy scheme in 2026 through a budget shift. SDE++ demonstrates the Dutch government's commitment to financially supporting the transition to a more sustainable energy system. By offering operating premiums, the scheme reduces the financial risk associated with investments in renewable energy technologies.

The MIA (Milieu-investeringsaftrek) and Vamil (Willekeurige afschrijving milieu-investeringen) offer tax deductions and accelerated depreciation for investments in environmentally friendly technologies. MIA and Vamil incentivize companies to invest in green technologies by reducing their taxable profits and improving capital efficiency. These allowances make sustainable investments financially more attractive through direct tax benefits. In the Spring Memorandum 2025, it is proposed to increase the budget reserve for the MIA by €35 million. The budget reserve for the VAMIL will be reduced by the same amount. The EIA (Energie-investeringsaftrek) allows companies to deduct a percentage of their investment costs in energy-efficient assets from their taxable profits. EIA is specifically aimed at improving energy efficiency and encourages companies to reduce their energy consumption and related environmental impact. By lowering the cost of energy-efficient technologies, EIA promotes their adoption across various sectors.

The Netherlands also employs several green taxes. The CO2 levy for industry and greenhouse horticulture is being steadily increased to stimulate long-term decarbonization. The rising CO2 levy creates a clear economic incentive for energy-intensive sectors to reduce their carbon emissions. The gradual increase provides companies with a predictable framework for planning and investing in emission reduction technologies. The afvalstoffenbelasting (waste tax) has recently been clarified to prevent deductions for CO2 emissions from waste incineration. This clarification aims to ensure the tax effectively discourages waste production and promotes recycling and reuse. By closing loopholes, the government strengthens the intended environmental impact of the tax. Levies on plastic and air travel have also been introduced to discourage environmentally harmful practices in packaging and transport. These specific levies target key areas of environmental concern, such as plastic pollution and the carbon footprint of air travel. By making these activities more expensive, the government hopes to stimulate more sustainable alternatives.

Recent and future changes in Dutch tax legislation regarding sustainability include phasing out the netting scheme for small-scale energy producers and introducing a separate, lower tax rate for hydrogen and lowering the energy tax with € 200 million for the years 2026 up and till 2028. The phasing out of the netting scheme and the introduction of a hydrogen tax rate reflect the Netherlands' evolving energy policy and increasing focus on promoting hydrogen as a clean energy carrier. These changes are intended to adapt the tax system to support the transition to a more decentralized and diversified energy landscape.

5. The United States' "Make America Great Again" Agenda: Implications for Environmental Taxes

The "Make America Great Again" agenda in the United States, particularly under a Trump administration, suggests a potential rollback of environmental regulations and a prioritization of traditional energy sources, which could significantly impact environmental taxes and ESG efforts. This agenda emphasizes domestic energy production and economic growth, potentially leading to a less supportive environment for green taxes and incentives compared to the EU. There is a potential for reversing incentives for clean energy and environmental protection, including rescinding unspent funds from the Inflation Reduction Act and terminating EPA regulations aimed at reducing emissions. Such actions could undermine the growth of the clean energy sector in the US and hinder efforts to combat climate change by reducing or eliminating crucial financial and regulatory support mechanisms. The potential dismantling of clean energy and environmental protection incentives could slow the transition to a low-carbon economy in the US.

The US approach to environmental taxes under this agenda contrasts sharply with the proactive stance of the EU and the Netherlands, highlighting the ideological and policy differences in addressing climate change and promoting sustainability through taxation. Where the EU and the Netherlands view taxes as a significant driver for sustainability, the US approach under this agenda tends to prioritize economic growth and energy independence, potentially leading to a weaker emphasis on environmental taxes.

6. Comparative Analysis of Environmental Taxes and Green Taxes: EU (Netherlands) vs. US

The EU, particularly the Netherlands, adopts a more integrated and proactive approach to using tax policy to achieve specific environmental objectives, while the US approach under the "Make America Great Again" agenda may prioritize economic growth over environmental considerations in tax policy decisions. This difference arises from fundamental disagreements regarding the urgency and approach to climate change and ecological sustainability. The long-term effectiveness of these different tax approaches will likely depend on factors such as policy consistency and longevity, the extent of investments in green infrastructure and innovation, and the global competitiveness of companies operating under these regimes. A stable and predictable regulatory environment with clear long-term goals is crucial for achieving meaningful change.

Table 1: Comparison of Environmental Taxation Approaches

7. Forward looking thoughts

The analysis demonstrates that the intersections between ESG and taxation in the current geopolitical climate differ significantly between the EU (with a focus on the Netherlands) and the US. The EU has a clear and ambitious strategy to achieve climate neutrality through a broad range of tax instruments and regulations. The Netherlands is at the forefront of this, with concrete incentives and green taxes aimed at stimulating sustainable behaviour across various sectors. In contrast, the "Make America Great Again" agenda in the US may lead to a shift in environmental policy and taxation, potentially emphasizing energy independence through the promotion of fossil fuels and deregulation. This could result in a less supportive environment for green taxes and incentives compared to the EU.

For companies operating in both regions, these divergent regulatory and policy environments are important. It necessitates adaptable and globally aware ESG and tax strategies. Multinational corporations must develop sophisticated strategies that account for the different tax and ESG landscapes in the EU (Netherlands) and the US to ensure compliance, optimize financial performance, and meet stakeholder expectations. This requires a deep understanding of local regulations, potential future policy shifts, and the integration of tax considerations into broader ESG strategies.

Despite geopolitical differences, the trend towards integrating ESG considerations into tax policy is likely to continue globally, albeit at varying paces and with different approaches, as the urgency of addressing climate change and sustainability challenges increases. The increasing focus on sustainability from investors, consumers, and regulators will continue to drive the integration of ESG into business practices and government policies, including taxation.

RSM is a thought leader in the field of international taxation consulting and technology innovation. We provide frequent insights through training and thought leadership, leveraging our deep knowledge of industry developments and practical experience working with clients. If you would like to know more about how the Tax Innovation Lab approach could benefit your organization, please contact one of our consultants.