As a part of the Norwegian tax authority’s modernization project for VAT, a new VAT return will be implemented from 01.01.2022, replacing the current form-based VAT return. There will be no transitional arrangement, nor will there be any opportunity to apply for dispensation. This means that VAT liable businesses in Norway will have to submit VAT returns in the new format from 01.01.2022, which will be when filing the VAT return for the 1st VAT period, due on 10.04.2022.

Background and purpose

The purpose of the new VAT return is that the Norwegian tax authorities want to re-use the machine script for SAF-T (Standard Audit File-Tax). The tax authorities also wish through this to gather more information, increase the data quality on underlying accounting data, and to reduce the number of manual processes. The current VAT regulations covering the length of VAT periods, submission deadlines and due dates, will not be changed, nor will there be any changes in which person who can fill in and submit the VAT returns.

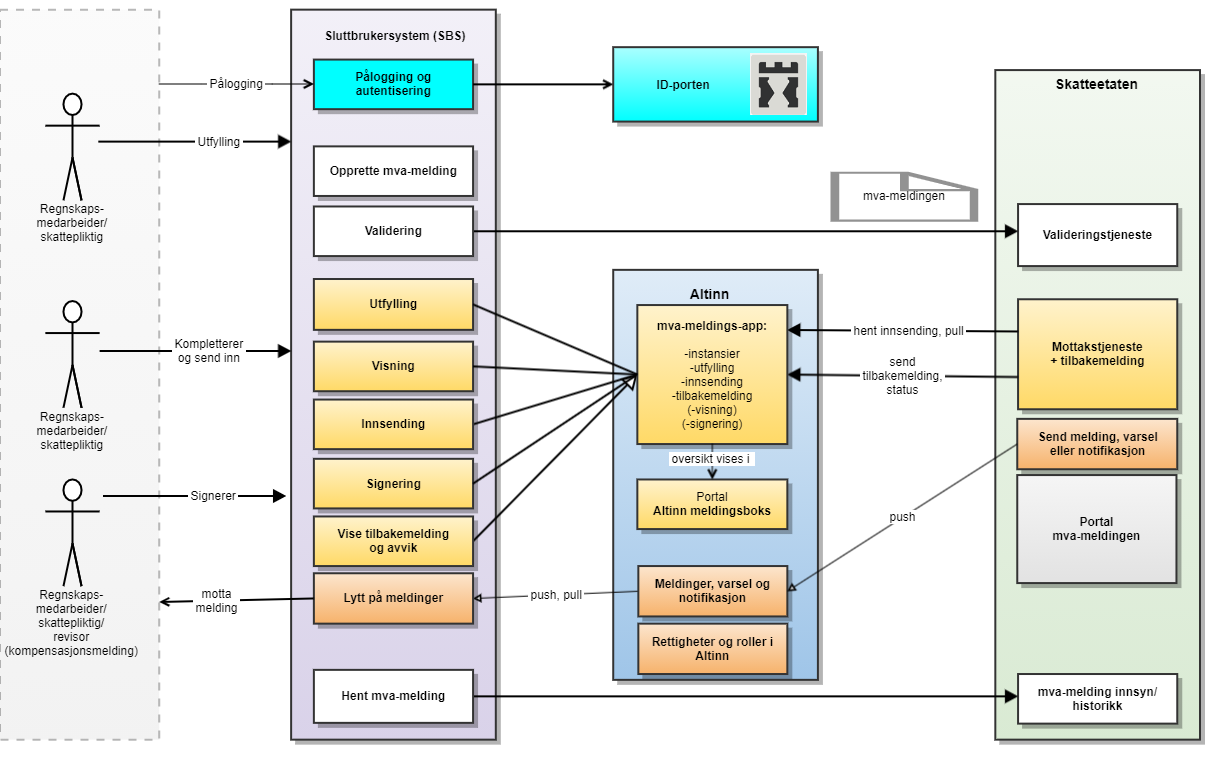

The Norwegian tax authorities prefer that the filing is done from «system to system», via a direct integration from the businesses accounting system and Altinn. However, it will still be possible to file the VAT return manually by logging on to the tax authority's portal and filing the VAT return from there. It is too early to say anything about how this will work, since the solutions have not yet been published. We expect however, that the manual solution will involve more work than the automatic submissions from the accounting system.

What should the businesses do to prepare themselves?

The tax authorities require that the accounting system for a business liable to book-keeping can create and submit the new VAT return. A relatively up-to-date accounting system from the major Norwegian system operators and/or -suppliers for accounting systems, is expected to have all the necessary functionality to deliver these VAT returns directly as said, including SAF-T, on the Norwegian Tax authorities reporting portal called Altinn. However, we strongly recommend that all businesses verify this with their system operators/suppliers in due time.

If the accounting system is ready for a new VAT return, and the VAT codes have already been mapped to the standard codes in SAF-T, the necessary preparations are done. Businesses that have not done the mapping exercise are basically already more than a year overdue (since this was a requirement already). Thus, they should complete the mapping exercise asap, including make sure that the chart of accounts against SAF-T is ready for a new VAT return, so that this is at least within time for a possible inspection by the Tax authorities.

If the accounting system does not have the opportunity to file the VAT return via the accounting system, it will as said still be a possibility to file the VAT returns manually by logging on to the tax authority's portal Altinn, and to fill in and submit the VAT return from there. A mapping of the VAT codes against SAF-T is however still a requirement, to report correct figures.

Changes in the VAT return

The Norwegian tax authorities are aiming to re-use the standard codes in SAF-T. This implies that the mapping of the VAT codes in the accounting system towards SAF-T is also used in the set-up of the new VAT return. The numbered entries in the current VAT return will be replaced by a report with specified lines for the standard VAT codes from SAF-T (SAF-T codes). SAF-T codes that have entries in the accounts for the relevant term, are the codes that will be reported. Thus, the number of lines in the VAT return reported and filed, may vary between the VAT periods, and from return to return.

The reported figures will be aggregated figures per SAF-T code, but business can choose to use more lines per code if specifications or remarks are required. Other updates are that withdrawals, losses on claims, VAT adjustments, and refund of VAT cf. The Norwegian VAT act section 9-6 and 9-7, must be specified. The Norwegian tax authorities have published a matrix (in Excel), which shows valid combinations of predefined notes (standardized additional information) and SAF-T code for the individual note.

The new VAT return also consists of an integration with Altinn including a validation and receipt service. The submission is validated and checked immediately, so that the business is quickly notified if the submission has been accepted or not.

{kind=link}

The submission of the VAT return should, as earlier mentioned, preferably go directly from the accounting system to Altinn via integration. This differs from SAF-T files that are extracted from the accounting system and then sent to the Norwegian tax authorities. However, it is in any case required that there is accordance between the figures in the VAT return and the SAF-T file for corresponding periods.

Further information about the SAF-T codes can be found here.

Increased specification requirements

As mentioned, there is a new requirement that transactions related to withdrawals, losses on claims and VAT adjustments (related to capital goods), must be specified. This will provide the tax authorities with more detailed information and provide them a better basis for more accurate audits/inspections.

Correction of previously submitted returns

It will still be possible to correct previously submitted VAT returns, however the current solution that opens for additional notifications will be abolished. A complete, new, and corrected VAT return must be submitted instead. Since the VAT return is to be produced in the accounting system, the book-keeping must be corrected accordingly, to change the VAT return. This ensures consistency between the SAF-T file and the VAT return.

Comments and attachments

If the predefined notes are not considered sufficient in certain cases it will be possible to provide in-depth comments related to specific VAT related information, when filing the VAT return. Furthermore, the system opens for uploading of up to 50 attachments per return, with a size of up to 25 MB per file.

New validation solution and test of the new VAT return

As mentioned, the new validation solution performs, upon submission, an automatic check of the content, and the coherence between the different elements in the VAT return. If there is a discrepancy in the notification, it will either be rejected, or a feedback will be given automatically, which states if the return has been submitted as a «deviating tax return».

To avoid challenges the last days before the first filing deadline in April 2022, the Norwegian tax authorities is said to be working on a solution where the new filing system can be tested. It is yet uncertain exactly when this solution will be available.

We assume that the new validation solution is not equated with a limited control/inspection by the tax authorities. Thus, a VAT return should be possible to resubmit without the risk of surtax.