Many businesses use innovation to grow, however the challenge and failure of many companies that carry out innovation projects is to inadequately budget for the innovation.

This failure is normally not because the company does not undertake a budgeting process, it is primarily because the company does not incorporate the full cost of innovation into the budget. In fact, existing, well run businesses, often have good budgeting and financial management practices in place, unfortunately innovation projects require considerations that the business has not previously taken into account.

To assist address this common problem, we have broken up the budgeting process into a number of steps that we believe will make a significant positive difference to the management of the financial challenges intrinsic to innovation.

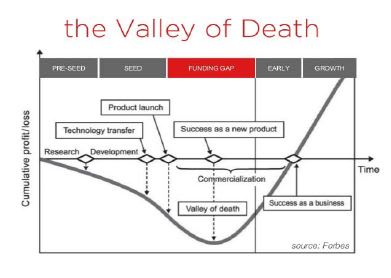

STEP 1 - THE VALLEY OF DEATH

Reviewing the “valley of death” graph, see below, should be the first step a company carries out during the assessment and budgeting process for a new innovation project. The valley of death is normally related to the fund raising gaps and challenges that start-ups have in taking their project from idea into full commercial operation. The same financial challenges and concepts apply to existing businesses that undertake an innovation project. In fact, it is more difficult in an existing business to manage the cost blow outs of innovation as the full costs of the project are often “lost” in the regular business operational costs and are not recognised until it is too late.

For example, existing businesses may decide that a project needs to be carried out to develop a new product to expand their market reach. The company applies its normal (and to date a proven successful) project costing methodology to the innovation project, which includes an estimate of time and materials to design, manufacture and test the new product. This process is doomed to failure from the beginning as it does not take into consideration the issues we will identify below.

STEP 2 - TRIPLE THE BUDGET

An analysis of the valley of death shows that approximately the first 1/3 of the funding cycle is the product development and testing, the rest of the funding cycle is the feedback modifications and full commercialisation time/costs for the project. The budgeting process in existing business uses normally only takes the first 1/3 of the total innovation costs into account.

Therefore, the second step in the budgeting process is to consider the differences between the normal budgeting needs versus the budgeting needs of innovation. One of the main reasons for under budgeting is failing to recognise that innovation projects normally require extra or different marketing and sales. For example, a company may undertake its new product innovation due to requests from potential clients. The company believes that because it has had direct queries from potential clients, the marketing and sales of the new product will be the same as its existing products. This basic assumption very rarely becomes reality as the promotion and sales of innovative products will require additional/new marketing and sales budgets. In addition, the time frame for selling innovation into the market almost always takes significantly longer than anticipated. Significant management theory has been written on the difference between the early adopter market and the mass market. Companies that mistake the early adopters for the mass market do not adequately budget for the innovation process.

Sales and marketing budgets should be extensive and cover all the direct and indirect costs, such as:

- Extra website development;

- Expo costs;

- Travel needs;

- Consumables and ancillary costs associated with demonstrations.

STEP 3 - MULTIPLE VERSIONS AND TRIALS ARE NECESSARY

Continuing from Step 2, another common budgeting mistake is the assumption that the “first version” will be the final version. Most innovation goes through a feedback and redevelopment loop, this needs to be addressed and incorporated into the budget process. In particular, a company should consider how agile its project development process is and be prepared to carry out more small stage testing during the early technical development process. The mistake is often that the technical pathway in innovation changes but the budget assumes a fixed pathway.

Innovation projects should also budget for “real world” testing and feedback changes that early clients will have. Many projects are budgeted up to the release of the first version, however in innovation the first version is rarely the last version.

Budgets should also include the costs of the trials, i.e. travel and accommodation that might be required to go to a client site for testing.

STEP 4 - FEATURE CREEP AND BESPOKE

If companies don’t get caught out at Step 3 they get caught in the big problem of “not finishing” the product. What happens for many technical experts is that they get caught up in continuing to improve and modify the product. While it is important to understand Step 3 it is equally as important to know when to stop developing and start selling.

STEP 5 - THE MANAGEMENT TEAM

Most innovation projects require substantial input from the most experienced staff of a company. It is often the case that many of these people are seen as overheads and not added into a budget. For innovation, these people will often be required significantly to assist with the innovation, from: technical, financial or commercial perspectives. It is important to add their time into the budget for two reason:

- Obviously their time is a cost to the business and should be considered: and

- While working on the innovation they will not be able to work on the existing business.

Point 2 is very important, what often happens is that the management time gets taken up significantly into the innovation and when it is not budgeted for they either don’t work enough on the innovation and it suffers OR they stop doing the normal/core business work and the existing business suffers.

Therefore, it is important to ensure that the budget includes the management team and appropriate measures are put in place to address their lack of time on other business.

And don’t forget to include the budgeting and reporting time/costs for innovation as they can often be more compared to other aspects of the business.

STEP 6 - ALL THE COSTS

It is now time to add up all the direct and indirect costs, including time, for the entire project. All of the costs of the project should take into consideration:

- Intellectual property needs;

- Legal & insurance requirements;

- If fund raising is required, how much will that cost and how long will it take;

- Step 2, 3, 4 and 5; and

- Business overheads.

What a company should now be able to do is assess the innovation project in a more realistic way and to consider if it has the resources, including time, to carry the project all the way.

STEP 7 - STRATEGIC ASSESSMENT

Now that the budget is complete the critical step should be to reassess whether the project should go ahead. The strategic assessment must take into account:

- Cashflow and financing needs;

- Impact of the innovation budget on the rest of the business;

- An assessment of the likelihood that the long term market success will be appropriate; and

- Confirm that the innovation aligns with the strategy and vision of the business.

STEP 8 - TRACKING AND ONGOING ASSESSMENT

Once an innovation project has commenced, the business must ensure sufficient management oversite is maintained. It is critical that management and strategic reviews are made at regular interval during the project. This will ensure that:

- Financial discipline and accountability for the project are maintained;

- Confirm that appropriate testing from a technical and market perspective is taking place;

- leadership direction and support is provided; and

- a connection between the existing business and innovation is retained.

This article first appeared in the Australian Manufacturing Technology magazine’s October/November 2016 edition.