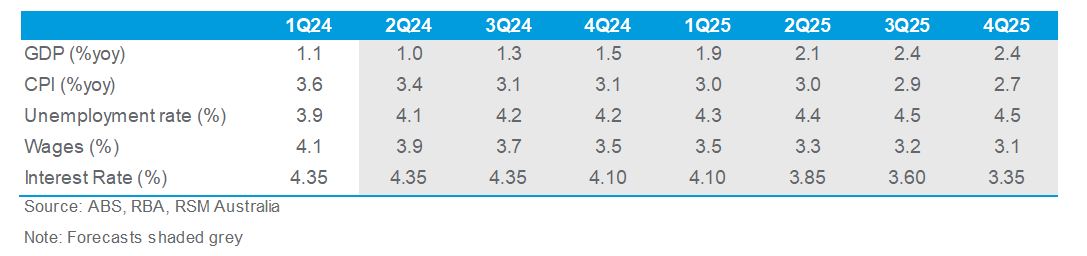

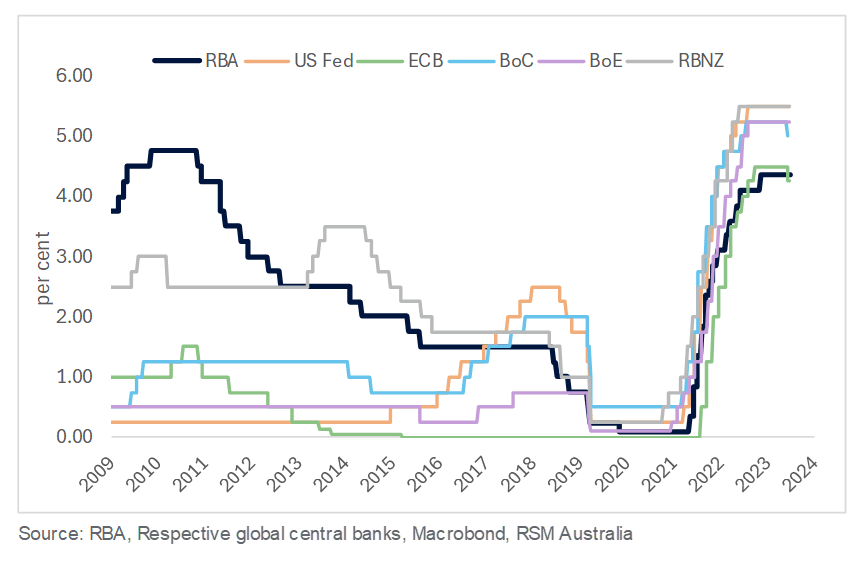

The Reserve Bank of Australia (RBA) is expected to maintain its interest rate at 4.35% until November 2024.

Inflation is projected to ease to 2.5% in 2026, with unemployment anticipated to rise to 4.5% by mid-2025.

The economic recovery is expected to be a gradual and extended process.

The Australian economy has stayed afloat due to population growth, but it has faced five straight quarters of decline per capita. High borrowing costs and a slower pace of price normalisation have led consumers to cut back on spending, making it harder for businesses to operate.

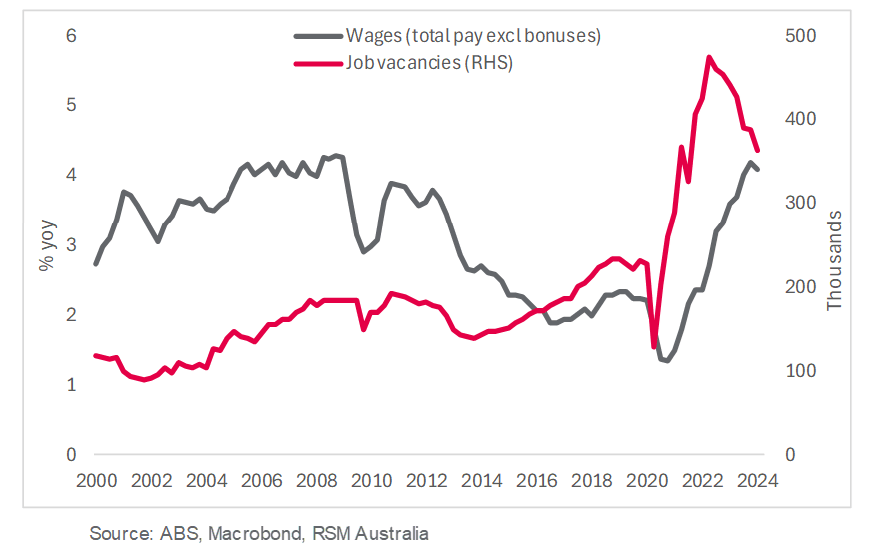

Inflation meanwhile continues to trend down at a glacial pace, with a 1.0% rise in the first quarter of 2024, driven by domestic demand and wage pressures amid weak productivity. The labour market remains tight, with unemployment at historic lows, yet underutilisation shows many people are not fully employed.

The Reserve Bank of Australia (RBA) is likely to delay immediate action by holding rates steady at 4.35% until November. The RBA’s cautious approach is sensible, considering potential inflationary impacts from recently announced budget measures. It's important to remember that we are still in a pandemic-aligned economic cycle. The final stages of controlling inflation have proven to be challenging globally, so being cautious is necessary.

A data-dependent approach is the need of the hour, even if it means short-term pain (“higher-for-longer” policy rates) for long-term gain.

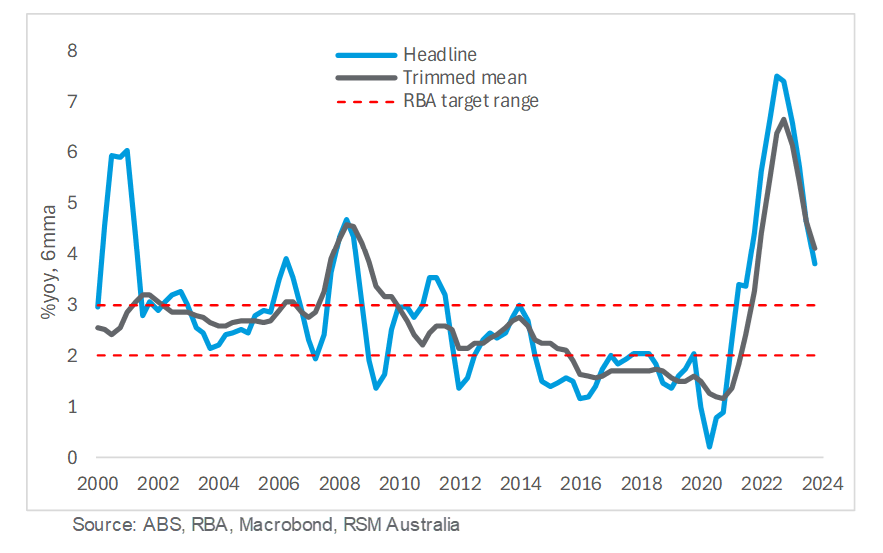

We can expect price pressures to ease faster in 3Q24 and 4Q24 once cost-of-living measures announced in the Federal Budget are implemented. We expect headline inflation to come down to 3.1% by end of this year and gradually reach the Reserve Bank of Australia's (RBA) target level of 2.5% in 2026.

It is important to remember that inflation is a lagging indicator i.e. falling inflation is a result of the RBA’s policy action through most of 2022-23 and its cautious hold well into this year. A restrictive hold is good insurance while rate hikes done previously continue to pass through and work towards bringing inflation down in the coming quarters.

In 1Q24, inflation, both headline and trimmed mean, while falling on a year-ago basis, rose 1.0%qoq led by non-tradable goods and services. RBA Governor Michele Bullock has often referred to domestic demand as a key concern for the central bank.

At 3.6%yoy, inflation may have more than halved from its peak in December 2022, however, it remains much higher than the RBA’s desired target range of 2%-3%. Price pressures in the essential categories do not seem to be receding fast enough. Rents and insurance featured prominently in the 1Q24 inflation print. Factors such as population growth, demand for rentals and undersupply of housing are structural challenges. Additionally, in areas such as the insurance market, costs have been rising due to unforeseen events like weather disruptions and increasing challenges in the residential market following builder insolvencies.

Concerns among policymakers about persistent inflation are well-founded. Recent developments in the rest of the world emphasise the need for caution in the late stages of combating inflation. It is particularly important to be careful in Australia where significant rebates have been and will be instrumental in keeping actual prices muted in the months ahead. Broadly, we expect goods inflation to continue to normalise at a much faster rate than services inflation. Rents and labour costs will likely continue to be areas of concern in the near term.

While we do not place much emphasis on the monthly fluctuations in employment figures, we remain vigilant about the underlying tightness. At present, the labour market still seems unusually tight, especially for a period of prolonged economic weakness. There are approximately 600k unemployed people, however, that is still 110k fewer people than in March 2020, just before the pandemic.

The Reserve Bank of Australia (RBA) is anticipated to maintain its stance at 4.35% well into the latter part of 2024. We project a pivotal shift by the RBA, with the potential for the first and sole rate cut in November, bringing interest rates to 4.10% by year-end. Demand-driven inflationary pressures, a tight labour market and a rather stimulatory Federal Budget pose a risk; that of another rate hike before the anticipated cut. The RBA's stance of "not ruling anything in or out" has transitioned our certainty from when to if, and now, if at all, regarding the easing of monetary policy.

We anticipate the RBA to seek a balanced approach to its dual mandate of maintaining price stability and labour market strength. Despite advancements in some areas, challenges persist, primarily led by population growth due to record migration levels contributing to inflationary stickiness, notably in the housing market. Recognising that certain structural challenges exceed the scope of monetary policy intervention, the RBA aims for a long-term perspective in decision-making, therefore, we think they would seek two more quarterly inflation prints before reconsidering its policy course.

Meanwhile, the government's primary emphasis remains on addressing cost of living pressures, as was evident in the Federal Budget delivered mid-May this year. The fiscal subsidies could possibly make the RBA’s job of bringing inflation down to target harder. What we mean is, the fiscal measures outlined in the Budget, while targeted towards bringing down headline costs, risk stoking demand-driven inflation if Australian households do not show restraint in spending the extra cash. With Australia still emerging from pandemic aligned economic cycles and an upcoming election in 2025, the interplay between monetary and fiscal policy is key. While the government aims to achieve "sustainable" growth along with inflation control, the RBA remains focused on its mandate to manage prices, necessitating a restrictive policy stance.

The rapid transmission of policy adjustments to the average Australian household via the mortgage channel limits the scope for the RBA to go much higher and we are comfortable in our call for the RBA to deliver its first rate cut in November, though we do not anticipate the start of an easing cycle. This rate cut, reducing the policy rate to 4.10%, is expected to be the only adjustment this year, aiming to bolster confidence among consumers and businesses and support the fragile economy. We foresee the central bank maintaining the rate at 4.10% until the second quarter of 2025, before easing consistently in the following quarters as price pressures come under control.

Risks

Significant uncertainty clouds the economic outlook due to sluggish GDP growth, persistent albeit moderating inflation, and a job market that is slower to normalise. Despite temporary budget relief measures, inflation risks remain, and sustained productivity growth is crucial to support the Reserve Bank of Australia's (RBA) efforts to control inflation.

Domestically, consumption is likely to gradually improve in line with growth in real disposable incomes as inflation falls.On the tradable side of things, uncertainty around China and the prolonged geo-political situation in the Middle East pose inflation risks by potentially disrupting trade channels.

In our view, the household sector is key to the overall economic outlook. On the upside, there is a risk that federal and state subsidies encourage people to start spending again, reversing the progress made so far on inflation. Furthermore, Australian homeowners are likely to get “wealthier” as the surge in house prices continues unabated, boosting confidence and spending, forcing the RBA to potentially hike. The downside risk is that should the weak sentiment among households extend its run and result in persistent spending lags, business revenue and labour markets would markedly suffer.

In times of falling consumption, high interest rates and labour market mismatches, businesses, particularly in the middle market, face a unique set of challenges.

First, decreased consumer spending directly impacts revenue, making it difficult for businesses to maintain sales and profits. With customers tightening their purses, we can expect businesses to continue to struggle over the next six months. It is likely going to be harder to sustain market position, particularly as cash flow problems will reduce the ability to invest in growth or innovation.

Second, high interest rates increase the cost of borrowing, which can be particularly burdensome for middle market businesses that rely on loans for working capital or expansion. The higher cost of capital means that these businesses must carefully evaluate any investments or expenditures, as the cost of financing can quickly outweigh the potential returns.

Third, the labour market poses significant challenges due to a mismatch between the skills employers need and what is available. Many businesses find it difficult to recruit and retain workers with the right skills, leading to gaps in productivity and efficiency.

In such a contractionary environment, a good strategy would be to explore alternative financing options, such as government grants, which can be more favourable than traditional loans. Smaller businesses might also benefit from renegotiating terms with existing lenders or looking for opportunities to consolidate debt at lower interest rates. Businesses can further mitigate risk and reduce costs by diversifying supply chains, ensuring more competitive pricing.

To address the skill mismatch, businesses need to invest in training and development programs to upskill their current workforce, ensuring they have the necessary skills to meet future challenges. Partnering with educational institutions or participating in apprenticeship programs can also help create a pipeline of skilled workers tailored to the businesses’ needs.

In summary, while the current economic environment presents significant challenges for businesses, adopting a proactive approach to cost management, exploring flexible financing solutions, and addressing skill gaps through training and development can help businesses survive till the outlook improves.

Devika Shivadekar

Devika Shivadekar is an Economist for RSM Australia based in our Sydney office.

She has a wealth of experience in macro-economic and financial research, spanning both public and private sectors, and a deep understanding of the APAC region. She follows key macroeconomic indicators such as growth, inflation, central bank decisions and the labour market to assess the overall health of an economy.

less reason to panic than the March print, but not enough reason to relax. The unwind in fuel has pulled headline CPI lower, yet the lift in trimmed mean inflation confirms that domestic price pressures remain sticky beneath the surface.")