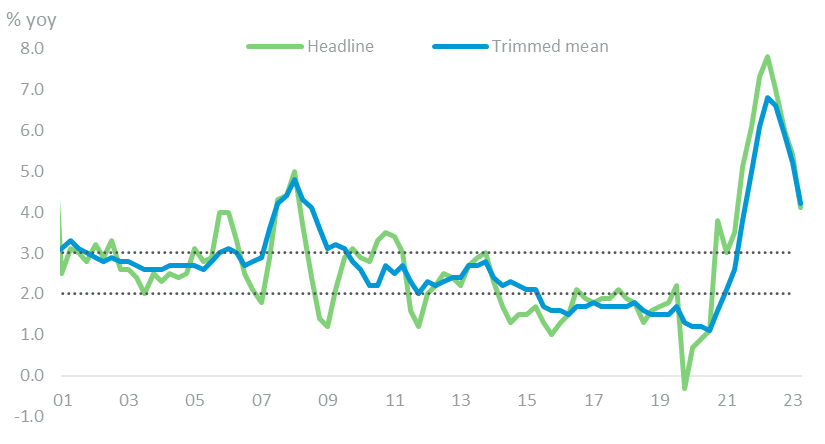

Today’s figures from the Australian Bureau of Statistics (ABS) reveal a 0.6% increase in the Consumer Price Index (CPI) for the December 2023 quarter, signaling a 4.1% annual rise, falling below market expectations.

The uptick in headline prices is the lowest sequential increase since 1Q21. Meanwhile, trimmed mean inflation, designed to eliminate price movement volatility, grew at 0.8%qoq and 4.2%yoy.

Although still above the Reserve Bank of Australia’s (RBA) desired target levels of 2%-3%, today’s print has undershot the Reserve Bank of Australia’s (RBA) latest expectations (4.5%yoy according to the Nov-23 Statement of Monetary Policy), which should be a source of satisfaction for the central bank.

EXHIBIT 1: Inflation trending down

Source: Australian Bureau of Statistics (ABS), Reserve Bank of Australia (RBA), RSM Australia

Monetary Policy Implications

The Reserve Bank of Australia finds itself in an increasingly comfortable position as overall inflation continues to ease. Regardless, we anticipate the RBA will exercise prudence before initiating any monetary easing measures. We argue for a pause at next week’s meeting due to the relative persistence of domestically driven price pressures. In addition to a decision around the levels of policy rates, 6 Feb will also be the day the RBA releases its Statement on Monetary Policy (SMP) that will have updated forecasts from the central bank and will give us a clearer picture around the RBA’s outlook.

We expect the RBA to maintain its current stance until the third quarter of 2024. Despite the easing of inflationary pressures, the central bank would also like to carefully manage inflation expectations, mitigating a potential surge in consumer spending, especially on discretionary items, in response to cost-of-living relief measures. Existing rebates like the Commonwealth Rent Assistance and Energy Relief Funds have notably eased household expenses.

Furthermore, the implementation of tax cuts scheduled for July 2024 introduces an element of uncertainty. Therefore, the RBA would prefer a cautious approach and remain on a watchful hold to verify that inflation indeed continues trending down and that the impact of tax cuts remains minimal.

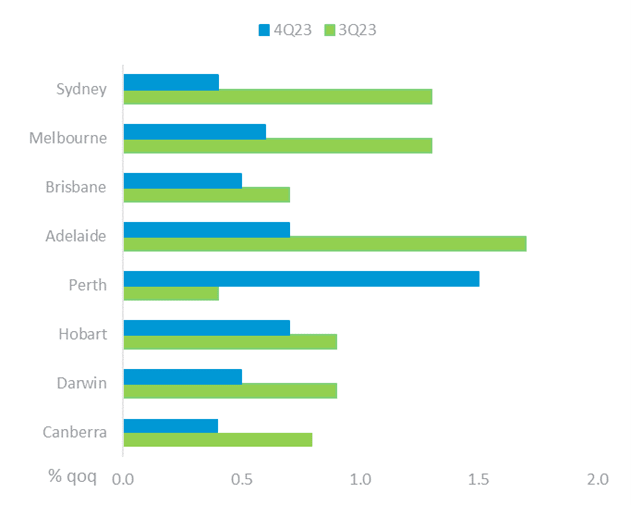

4Q23 CPI Movers and Shakers

In the December quarter, housing prices witnessed a notable 1.0% sequential increase, driven by a 1.5% surge in new dwellings purchased by owner occupiers, alongside a 0.9% rise in rents and a 0.6% uptick in utilities. Insurance and financial services experienced a quarterly increase of 1.7%, attributed largely to elevated premiums across various insurance categories taking the annual increase in premiums to 16.2%, the highest since March 2001.

Food and non-alcoholic beverages recorded a 0.5% uptick, marked by increases in eating out and takeaway foods (0.9%), which was partly offset by meat and seafood price declines of 1.2% due to increased supply. Annually, food inflation eased to 4.5% from 4.8% in 3Q23. Meanwhile, alcohol and tobacco prices saw a sharp 2.8% quarterly rise, led by a significant 7.0% increase in tobacco following excise indexation.

By capital cities, Perth led the charge with prices increasing 1.5% sequentially, driven by a substantial surge of 56.7% in electricity prices. This rise was following the conclusion of the first instalment of the Energy Bill Relief Fund rebates introduced in July 2023, partially offset by the introduction of the second instalment for all households starting from December 2023.

EXHIBIT 2: Capital city comparison in price increases

Source: ABS, RSM Australia

FOR MORE INFORMATION

If you would like to learn more about the topics discussed in this article, please contact your local RSM office.