Whilst contractors have long been a focus of state revenue authorities, we have seen a significant increase in audit activity over the last 6 months, as well as a much more analytics-based review of contractor populations.

In addition, the need to have supporting material for contractor positions taken is more important than ever with revenue authorities casting a wide net over contractor populations in the first instance, and only reducing the population where detailed support is provided.

The purpose of this article is to:

- Outline the steps an organisation should take to determine if payroll tax is payable on an independent contractor;

- Confirm what levels of support would be appropriate where a relevant contract exemption is being sought; and

- Provide an overview of how an analytics-based approach can assist in compliance, particularly where a number of contractors have been engaged during a financial year.

Dealing with contractors*

The first consideration is to first determine whether the worker should actually be considered an employee for payroll tax purposes, or whether the treatment of the worker as a contractor is appropriate.

The determination of employee versus contractor is quite a detailed consideration so for the purposes of this article we will focus on the engagement of a bona fide contractor.

However, if you want to learn more about the employee versus contractor considerations please refer to our previous thought leadership article here.

For payroll tax purposes, when engaging a contractor an organisation should first consider what they have engaged the contractor for.

If the contract is one for which the organisation has engaged with the contractor to provide labour to a client of the organisation, it may be the case that the organisation is deemed to have entered into an employment agency arrangement. Where this is the case payroll tax will be payable and there are no exemptions.

Where on the other hand the engagement is one where the contractor provides services to the organisation specifically, it is likely to constitute a ‘relevant contract’. Where a relevant contract is in place payments to the contractor would prima facie be subject to payroll tax however, there are a number of exemptions available for payroll tax.

*The Pay-roll Tax Assessment Act (Western Australia) does not contain relevant contract provisions. Where the worker is determined to be a bona-fide contractor payroll tax will not apply in Western Australia.

Relevant contract exemptions

There are three specific exemptions and six general exemptions that can be applied to contractors in most states and territories.

The treatment for contractors under the Payroll Tax Act is harmonised across all states beside Western Australia (WA) and in some cases Australia Capital Territory (ACT).

THE THREE SPECIFIC EXEMPTIONS UNDER LEGISLATION THAT MAY BE APPLIED ARE THE FOLLOWING:

| Specific exemption | Detail | Required support (example) |

1 | Services provided by an owner-driver | The contractor’s main purpose for work is conveyance and the vehicle is not owned or leased by the employer. Note: courier cyclists are not regarded as owner-drivers. | Copy of the contract/invoice detailing the work undertaken |

2 | Services provided by door-to-door sales agent | The contractor is hired by the employer to sell domestic goods. Note, the goods must be sold to the public and be sold at the buyer’s home or work. | Copy of the contract/invoice detailing the work undertaken |

3 | Services relating to selling insurance | The independent contractor is hired by an insurance company to sell insurance. Note, the contractor must hold an Australian Financial Services licence. | Copy of the contract/invoice detailing the work undertaken |

THE SIX GENERAL EXEMPTIONS UNDER LEGISLATION THAT MAY BE APPLIED ARE THE FOLLOWING:

| General exemption | Detail | Required support (example) |

1 | 90-day exemption | The independent contractor provided the same or similar services under a relevant contract to the employer for 90 days or less in a financial year. Note: The 180-day exemption in no way extends the 90-day exemption. Example: A contract security officer works for Company A for 50-night shifts (on non-consecutive days) in total for a financial year. The security officer works from 9pm to 5am in each shift. This means one shift is considered to be 2 days. Therefore, the security officer has worked for 100 days. Payments made by Company A to him are liable for payroll tax. | Invoices, timesheets

Accounts Payable Ledger (showing the period that the payments cover)

Using the ‘replacement method’ under PTA 035v2 undertake an assessment of the days worked based on the estimated remuneration for 90 days service. |

2 | 180-day exemption | For this exemption the focus is on the particular type of service required by the principal, and whether these services are of a type ordinarily required by the business for less than 180 days in a financial year. In this respect more than one contractor can provide the service at the same time. | A clear position outlining what the particular services were and why it is that the business only requires them for less than 180 days in a year. Where necessary, Invoices, timesheets, and relevant accounts payable information. |

3 | Exemption for contractors ordinarily rendering services to the public | Contractors hired to provide services to the public are exempt from payroll tax. If a contractor working for you provides similar services to the general public, you can apply for an exemption.

Note there is an exemption available from the Chief Commissioner without making a specific application where the contractor provided the services to two or more principals during the financial year and the contractor worked an average of 10 days or less per month (where they were engaged for at least one day in a particular month).

For example, a computer programmer provided their services to Principal A and Principal B and worked for 108 days throughout 12 months for Principal A. Payments made by Principal A to the computer programmer are exempt from payroll tax as they worked an average of 9 days per month. However, if the contractor worked 108 days throughout 6 months within the financial year for Principal A, payments made by Principal A are subject to payroll tax. | Confirmation from the contractor in writing that he or she has provided services of that type to two or more businesses A copy of an invoice issued to another business (outside of your tax group if applicable) Invoices, timesheets issued to you Accounts Payable Ledger (showing the period that the payments cover) |

4 | Engaging others | The contractor engages with others to provide the services or/and 2 or more people fulfilled the purpose of the relevant contract. For example, a plumber was hired by a business where they completed the work, and their significant other was doing the invoicing. The exemption cannot be claimed as one person did the actual work of the contract. The invoicing is not the purpose of the contract. | Copy of the applicable invoice to the extent this details two or more are involved. Copy of the agreement in place Confirmation from the contractor in writing |

5 | Services not ordinarily required | Services provided by the contractor are not ordinarily required or associated with the employer’s main area of business. In order for this exemption to apply, your business must not ordinarily require this service, the contractor must provide these services to other clients, and the contractor must derive less than 40% of their gross trading income from the principal. | Confirmation from the contractor in writing that he or she received less than 40% of their trading income from you Invoices, timesheets issued to you A basis for why these services are not ordinarily required by your business |

6 | Services ancillary to the supply of goods | An exemption may apply where the contractor is primarily engaged for the supply of the goods rather than the supply of labour or services. Note, employers can use the “working guide” to determine if the provision of labour is ancillary to the supply of goods where over 50% of the total contract amount goes toward to the contractor for providing the materials or equipment. | Copies of invoices/contract to show that the contractor supplies materials/equipment as part of the contract |

Once you have determined which contractor payments should be included, you should only include the GST exclusive value as subject to payroll tax. In addition, where the contract contains both labour and non-labour components, employers may deduct an approved non-labour component from their taxable wages

BELOW IS AN EXAMPLE OF HOW MUCH CAN BE DEDUCTED FROM CERTAIN CONTRACTOR TYPES:

Type of contractor | Deduction from gross payments to contractor |

Architects, Computer programmers, Draftspersons, Engineers | 5% |

Painters (who do not provide their own paint) | 15% |

Wall and ceiling plasterers | 20% |

Blind Fitters, Building Supervisors (who provide their own vehicles and inspect more than six sites per week), Carpenters, Carpet layers, Electricians, Fencing contractors, Plumbers, Roof tilers, Tree fellers, Wall and Floor Tilers | 25% |

Bricklayers, Cabinet Makers / Kitchen Fitters, Painters (who provide their own paint) | 30% |

Resilient floor layers / vinyl layers | 37% |

Implementing a sound contractor assessment process

In implementing a sound contractor assessment process it is our view that the process should commence at the initial engagement of the contractor.

The organisation should have clear oversight of the contractors engaged in the business, as well as the relevant contract exemption they feel is most likely to apply. This can then drive the information requirements needed, including confirmations required from contractors engaged.

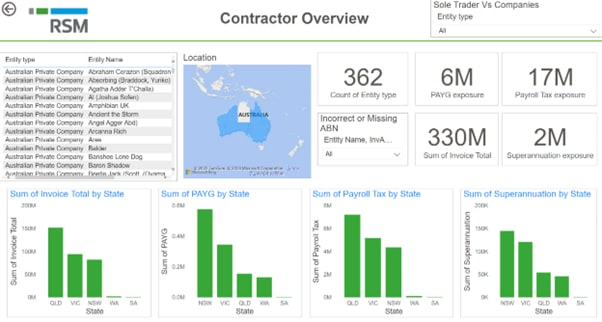

Particularly where there is a significant amount of AP data, we recommend a data analytics based approach to identifying the appropriate contractor position.

RSM have significant experience in assisting clients in managing contractor obligations, and implementing robust processes for ensuring compliance, including the use of data analytic tools where required.

For more information

For more information on payroll tax and/or contractor issues, please contact Rick Kimberley (National Employment Tax Leader).