A Practical Guide to Tax-Efficient Wealth Creation

As a medical professional embarking on your career in Australia, developing a sound understanding of superannuation strategies can provide you with significant financial advantages, both for first home ownership and long-term wealth accumulation.

The Australian super system offers unique avenues, such as the First Home Super Saver (FHSS) Scheme and personal super contributions, to optimise your tax position. Furthermore, even high-income earners subject to Division 293 tax can benefit from the concessional treatment of super contributions. This article explores these strategies in depth, equipping you with practical insights and worked examples to inform smarter financial choices.

As a medical professional embarking on your career in Australia, developing a sound understanding of superannuation strategies can provide you with significant financial advantages—both for first home ownership and long-term wealth accumulation.

Key benefit: If your goal is to purchase and live in an Australian property, the First Home Super Saver (FHSS) Scheme stands out as a powerful tool. By allowing you to make voluntary contributions into super (typically taxed at a lower rate than your marginal income tax), the FHSS enables you to build your deposit more efficiently and withdraw these funds, plus associated earnings, when you’re ready to buy your first home to live in. This means you can accumulate savings faster and enjoy tax advantages not available through ordinary savings accounts, making home ownership more achievable for newcomers to Australia.

The Australian super system offers unique avenues, such as the FHSS and personal super contributions, to optimise your tax position. Furthermore, even high-income earners subject to Division 293 tax can benefit from the concessional treatment of super contributions. This article explores these strategies in depth, equipping you with practical insights and worked examples to inform smarter financial choices.

Understanding the FHSS Scheme

The First Home Super Saver (FHSS) Scheme allows individuals to make voluntary contributions to their superannuation fund and later withdraw a portion to help purchase their first home. For medical professionals new to Australia, this presents an appealing path to home ownership by leveraging the tax advantages of super.

Key Advantages of FHSS

- Lower Tax Rate on Contributions: Voluntary concessional contributions are generally taxed at 15%, which is often significantly lower than your marginal tax rate.

- Additional Earnings: You can also withdraw associated deemed earnings on your contributions, further boosting your deposit.

- Higher Net Savings: By receiving a tax offset (30%) on assessable FHSS withdrawals, your effective tax rate on withdrawal is reduced.

- Annual and Lifetime Caps: You can contribute up to $15,000 per year, with a maximum of $50,000 over all years.

Disadvantages and Considerations of FHSS

- Eligibility Restrictions: You must be a first home buyer and intend to live in the property.

Risk Mitigation: Confirm your eligibility through the ATO’s official guidelines before making contributions. Consulting a financial adviser can help ensure you meet all requirements and avoid unintended ineligibility. - Timing and Access: The process involves requesting a FHSS determination, a release, and strict timing related to purchasing your home, which can complicate property transactions.

Risk Mitigation: Plan your home buying timeline carefully, allowing extra time for processing requests and releases. Engage your super fund and seek professional guidance early to help coordinate the timing of your withdrawal and property purchase. - Investment Risk: Returns on your super contributions depend on your fund's performance and the notional earnings calculation, not guaranteed investment returns.

Risk Mitigation: Choose a diversified investment option within your super fund to help smooth returns and reduce potential volatility. Regularly review your super fund’s performance and adjust your investment strategy accordingly. - Limitations on Property Types: FHSS cannot be used for houseboats, motor homes, or vacant land unless for home construction.

Risk Mitigation: Check property eligibility criteria prior to entering into contracts and discuss your plans with your super fund or a qualified adviser to confirm compliance with FHSS rules.

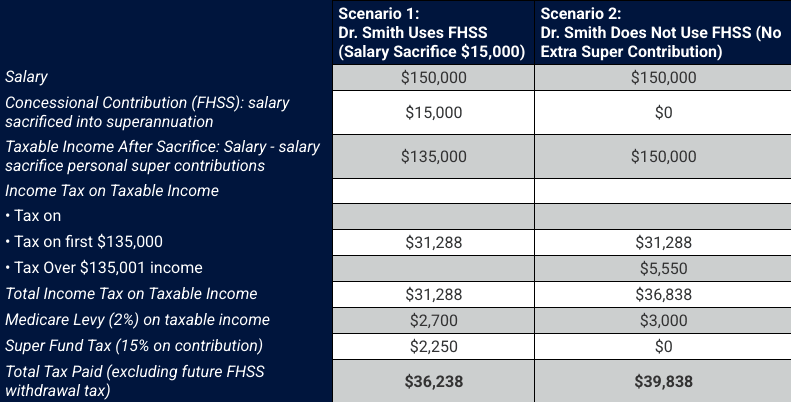

Comparison: Tax on taxable income with and without FHSS Contributions

Summary Table

- With FHSS: $36,238 total tax (incl. super fund tax, excl. FHSS withdrawal tax)

- Without FHSS: $39,838 total tax

- Immediate Tax Saving: $39,838-36,238 = $3,600

Notes & Considerations

- When Dr. Smith later withdraws the FHSS amount, tax applies at their marginal tax rate minus a 30% offset. This may reduce some of the upfront tax benefit, but the overall tax efficiency typically remains favourable compared to not using FHSS for eligible first home purchases.

- The example assumes Dr. Smith’s salary and marginal tax rate remain constant and does not account for investment returns or future changes to superannuation rules.

If Dr. Smith decides not to withdraw the FHSS amount, the funds will simply remain in their superannuation account, continuing to benefit from the concessional tax environment and compounding investment returns until they become eligible for access under the general superannuation rules.

Maximising personal super contributions

Beyond FHSS, making personal contributions to your super can further reduce your taxable income and build long-term savings, especially important for high-earning medical professionals.

Advantages of personal super contributions

- Tax deductibility: You can claim a tax deduction for personal contributions, reducing taxable income.

- Low tax environment: Contributions are taxed at 15% in the fund, often lower than your marginal tax rate.

- Compound growth: Funds grow tax-effectively within super.

- Access to government offsets: Lower-income partners may also access super co-contributions or the low-income super tax offset.

- Potential for increased return on investment if the fund performs well

Disadvantages of personal super contributions

- Preservation age: Contributions generally cannot be accessed until reaching preservation age (currently 60 for most).

- Contribution caps: Annual concessional cap is $30,000; exceeding it leads to extra tax.

- Deduction process: You must notify your fund and receive acknowledgment before claiming a deduction.

- Reduced return on investment if the fund underperforms.

Example: Tax saving through personal super contribution

| Tax at $210,000 (before contribution): | $64,838 |

| Tax at $190,000 (after contribution): | $58,438 |

| Net tax saving: | $6,400 |

Division 293 Tax: Still beneficial for high-income earners

Many medical professionals worry that if their income exceeds $250,000, the Division 293 tax—an extra 15% on concessional super contributions—negates any tax benefit. This is not the case.

Even at high income levels (e.g., $190,000+), super remains a tax-effective savings vehicle. Here’s why:

Division 293 tax only increases the effective tax rate on concessional contributions to 30%, which is still lower than the top marginal tax rate (up to 45% plus Medicare levy).

Comparison: $300,000 income with and without $30,000 super contribution with Division 293 tax effect

Summary of outcomes

| With $30,000 super contribution: Total tax paid | = $102,038 |

| No super contribution: Total tax paid | = $107,138 |

| Net benefit of contributing to super: $107,138 - $102,038 | = $5,100 |

Even after Division 293 tax, making concessional contributions to super is still more tax-effective for high-income earners compared to receiving the amount as salary, thanks to the lower effective tax on super contributions.

If you’re liable for Division 293 tax, the Australian Taxation Office will send you an assessment, and you can pay this tax directly or choose to have it released from your super fund by lodging a release authority.

Summary Table: 2024–25 Australian Resident Tax Rates (2025-26)

| Taxable income | Tax on this income |

|---|---|

| 0 – $18,200 | Nil |

| $18,201 – $45,000 | 16c for each $1 over $18,200 |

| $45,001 – $135,000 | $4,288 plus 30c for each $1 over $45,000 |

| $135,001 – $190,000 | $31,288 plus 37c for each $1 over $135,000 |

| $190,001 and over | $51,638 plus 45c for each $1 over $190,000 |

Medicare levy: 2% of taxable income (all calculations above include this).

From 1 July 2024, the concessional contributions cap is $30,000.

At RSM, we understand that as a busy medical professional, your time is precious, and your financial landscape is uniquely complex. Our dedicated team of experts specialises in supporting healthcare practitioners like you with tailored financial strategies, ensuring you maximise your after-tax income, optimise your superannuation contributions, and grow your personal wealth—all while remaining compliant with Australia’s ever-evolving tax regulations.

From navigating Division 293 tax implications to structuring your superannuation and investments tax-effectively, RSM offers end-to-end solutions to simplify your financial affairs. We stay ahead of legislative changes, proactively identifying opportunities and potential risks so you can focus more on patient care and less on paperwork.

With RSM as your trusted adviser, you benefit from personalised advice and advanced planning that aligns with your career goals and life ambitions. Our support empowers you to take full advantage of every benefit available within the Australian tax system, turning tax compliance from a chore into a strategic wealth-building opportunity.

Connect with our team today by contacting your local RSM office to get personalised guidance tailored to your career and goals.