The Commissioner of Taxation (the Commissioner) has now issued the much-anticipated legislative instrument setting out the alternative decline in turnover tests that can be applied by an entity as part of satisfying the eligibility criteria for the JobKeeper payment scheme.

While many entities will benefit from these alternative tests (eg start-ups and rapidly growing businesses), it is very disappointing to see that there is no alternative test that applies to corporate groups that employ staff in a service entity structure.

Given the service entity issue is one which has received much attention and has been raised with Treasury and the Australian Taxation Office, the non-inclusion of a specific service entity alternative test indicates a deliberate policy decision by the Government to not widen the scope of the JobKeeper scheme to groups operating with a service entity structure unless they would otherwise qualify under the basic decline in the turnover test.

In our view, this is not in keeping with the intention of the scheme as many businesses will fail to qualify merely by virtue of having an alternative, but perfectly legitimate, legal structure. Of course, it is ultimately the employees of those businesses that will suffer the consequences.

Why is the decline in turnover test relevant?

To recap, in order to be eligible to receive JobKeeper payments, an entity needs to satisfy a decline in the turnover test. Under the basic test, an entity is entitled to choose one of the nine “turnover test periods” between March and September 2020 and compare that to its equivalent “comparison period” in 2019. For example, an entity using a test period of the month of April 2020 would compare the GST turnover in April 2020 to the GST turnover in April 2019 to determine the percentage decline.

The Treasurer’s Rules, which outlines the basic test, acknowledges that the basic test could be inappropriate and unfair to certain classes of entities and allows for the Commissioner to issue a legislative instrument setting out alternative tests that an entity may satisfy instead.

What are the alternative tests?

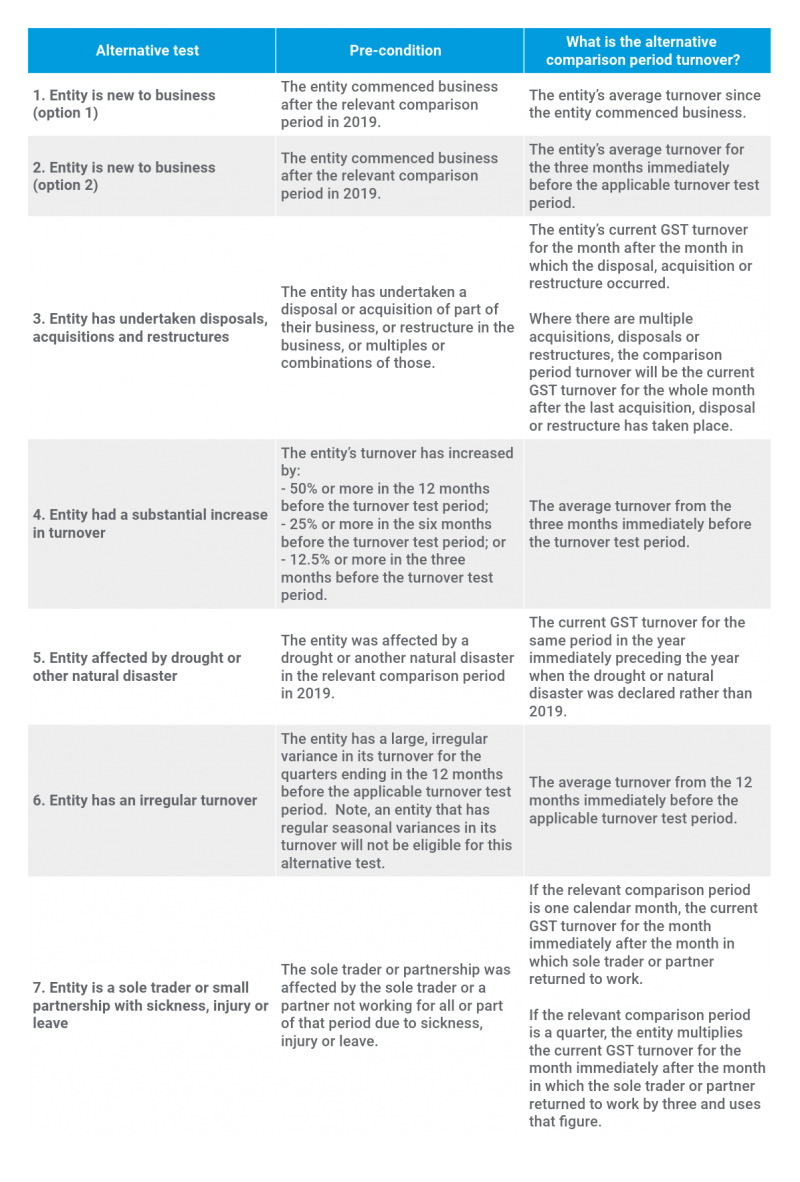

The Commissioner has set out the following seven alternative tests:

Click the below table to enlarge.

Other points to note

- For the sake of clarity, the Commissioner confirms that an entity only has to satisfy either the basic test or at least one of the alternative tests to have satisfied the decline in the turnover test. Therefore, if an entity satisfies the basic test, it does not need to consider or satisfy, one of the alternative tests.

- There are allowances made within the alternative tests for two scenarios:

- Where an entity qualified for the ATO’s Bushfires 2019-2020 lodgement and payment deferrals, the months which were affected by the bushfires will be excluded from the calculation of the comparison period turnover, unless there no other appropriate months; and

- Where the entity received Drought Help concessions provided by the ATO, the months which were affected by the drought will be excluded from the calculation of turnover, unless there are no other appropriate months.

- The alternative tests are not discretions and do not require an application or submission to the Commissioner. Instead, an entity is required to self-assess its own eligibility to apply one of the alternative tests.

- The record-keeping requirements that apply to an entity using the basic test will also apply to an entity using an alternative test. Therefore, entities need to ensure they have robust and reasonable turnover calculations on file in the event that the Commissioner undertakes a review or audit of their JobKeeper payment eligibility.

Grappling with turnover? How to get it right for the Jobkeeper payment eligibility.

If you require assistance in determining JobKeeper payment eligibility using the alternative test, please do not hesitate to contact your local RSM office.