AUTHORS

At a glance: What impacted Australian MNE Groups need to focus on now:

• Confirm in scope status and group composition - Before anything else, MNE Groups must formally determine whether they are within the scope of the Pillar Two GloBE Rules—including identifying all constituent entities, confirming consolidated revenue thresholds, and understanding any joint venture or stateless entity implications.

• Assess eligibility for the Transitional CbC Safe Harbours - Conduct a jurisdiction by jurisdiction assessment of the Transitional Safe Harbours, ensuring eligibility in the first year to preserve access.

• Evaluate potential top up tax exposures - affected taxpayers should begin modelling ETR outcomes, identifying jurisdictions that will require full GloBE calculations, and considering cash tax and provisioning impacts

The long anticipated impact of the OECD’s Global Anti Base Erosion (“GloBE”) Rules has now become a pressing reality for impacted multinational (“MNE”) groups, with the first Pillar Two reporting obligations due on 30 June 2026 (in respect of the 31 December 2024 Fiscal Year).

Relatedly, on 16 February 2026, Treasury issued the draft instrument Taxation (Multinational - Global and Domestic Minimum Tax) Amendment (2026 Measures No. 1) Rules 2026 (Exposure Draft), which proposes to amend Australia’s GloBE rules to accord with administrative guidance issued by the OECD so as to ensure Australia’s implementation of the GloBE Rules achieves qualified status.

Given the looming deadline and substantial level of work required to adequately assess the impact of the rules, we have set out below the top three areas that MNE Groups should be looking at finalising over the next few months to prepare. Additionally, we have provided a brief summary of the upcoming lodgement requirements of the amendments being proposed to Australia’s GloBE rules.

A quick (very simplified) overview of the GloBE Rules:

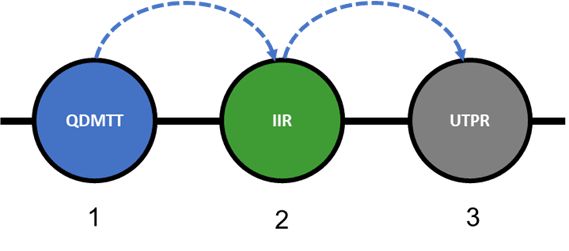

The GloBE Rules provide for a coordinated system of taxation intended to ensure MNE Groups are subject to a global minimum tax rate of 15% in each jurisdiction where they operate. In the event the effective tax rate (ETR) in a jurisdiction is less than 15% - a top-up tax liability may crystallise. This is achieved via three main mechanisms, being;

- Qualified Domestic Minimum Top-up Tax (“QDMTT”) – if the ETR of an entity or entities in that jurisdiction is less than 15%, the jurisdiction in which those entities are resident can allocate the top-up tax to those entities. Australia has a QDMTT.

- An Income Inclusion Rule (“IIR”) – if the ETR of an entity or entities in a jurisdiction is less than 15%, the top-up tax is allocated to either a direct or indirect parent entity (highest up the chain parent first) that has an IIR. The parent entity may be entitled to a tax credit for any top-up tax paid under a QDMTT. Australia has an IIR.

- Under Taxed Profits Rule (“UTPR”) – if the ETR of an entity or entities in a jurisdiction is less than 15%, there is no QDMTT in force and no direct or indirect parent entity is located in a jurisdiction with an IIR, then the top-up tax is shared between all entities in the group that have a UTPR. The allocation is based on a substance test prescribed in the GloBE Rules. Australia has a UTPR.

For a more detailed overview of the GloBE Rules please click here.

Given the complexity involved, there are transitional safe harbours (largely based on an MNE Group’s CbC reporting data) which, subject to satisfying the eligibility criteria, will greatly reduce the additional compliance burden.

Here are the top three areas affected taxpayers should be focusing on right now:

The following three topics should be key focus areas for MNE Groups that have established that they are within the scope of the GloBE Rules (i.e., established which entities form part of their MNE Group, and whether that Group has had €750 million in consolidated revenue or more in two of the prior four fiscal years). If an in-scope assessment has not been undertaken, then this analysis should be performed as soon as is possible prior to considering the below.

1. Transitional Country–by-Country Safe Harbour Assessment

- If not already done, a group assessment of the Transitional CbC Safe Harbours (“CbC TSH”) (a system of safe harbours that, if available, can significantly reduce the compliance burden faced by impacted MNE Groups) is required to be undertaken as a matter of priority to ensure they can be relied on. Where an entity (or entities) in a jurisdiction satisfies (satisfy) the eligibility criteria for the CbC TSH, the top tax-up tax required for that jurisdiction is deemed to be nil.

- If a MNE Group is intending to rely on the CbC TSH, the eligibility criteria MUST be satisfied in the first year of applying the rules or it becomes permanently unavailable.

- The eligibility criteria are assessed on a jurisdictional basis (as opposed to an entity-by-entity basis) Any jurisdictions that fail the eligibility criteria will be required to prepare detailed GloBE calculations.

- Australian entities should be looking to formally document how they satisfy the eligibility criteria. If something has been prepared at a group level by an overseas parent, this analysis should be requested and kept on file locally. Penalties apply specifically for failing to keep and maintain adequate documentation on file.

2. Assessment of tax adjustments under the IIR and UTPR

IIR

- The IIR applies to Fiscal Years ending on or after 31 December 2024 (Fiscal Year refers to the financial year of the ultimate parent entity of the MNE Group).

- If an affected Australian taxpayer has subsidiaries offshore, a top-up tax under the IIR may be required. This applies where the relevant jurisdiction has not met the CbC TSH criteria and its ETR is less than 15%. If this is the case, the top-up tax needs to be calculated and assessed now.

UTPR

- The UTPR will be applicable for the first time in respect of Fiscal Years ending on or after 31 December 2025. This should be front of mind while the work for 31 December 2024 is being conducted.

- If applicable, the UTPR is designed to result in additional cash tax expense via the denial of income tax deductions that would otherwise be available. This can result in the accelerated use of carry forward tax losses.

- For any tax provisioning work being undertaken, this should be taken into account.

- Whilst not determinative, the risk of the UTPR applying to Australian entities is heightened where the ultimate parent entity is located in a jurisdiction that has not implemented the GloBE Rules.

3. Administrative Matters

The following administrative matters also warrant consideration:

- (For US owned groups) the new Side-by-Side Package (“SBS Package”) published by the OECD/G20 Inclusive Framework only applies for years starting on or after 1 January 2026. From 1 January 2026, this will mean that for US owned groups, the IIR and UTPR will not apply. However, for the 31 December 2024 and 31 December 2025 income years, subsidiaries of US owned groups will have to apply the full suite of the rules. More detail on the Sbs package can be found here.

- Finding out where the GloBE Information Return (“GIR”) be lodged?

- What are the Australian reporting deadlines if the Australian entity has a financial year that differs to that of the ultimate parent entity of the MNE Group?

- Will an Australian entity be lodging the GIR on behalf of other entities?

- Are there any joint ventures in Australia or stateless constituent entities with a nexus to Australia that need to be separately assessed under the GloBE Rules?

New Lodgement Requirements for affected MNE Groups

Consistent with the GloBE Rules, there will be four new lodgment requirements for affected MNE Groups. These are:

- GIR

- Foreign lodgment notification

- Australian IIR/UTPR Tax Return (AIUTR)

- Australian DMT Tax Return (DMTR).

As of the date of publication, the ATO is in the process of developing the forms required for the lodgement obligations outlined above. As these forms are not yet available for review, we encourage affected Australian taxpayers to ensure they have completed the necessary preparatory work (e.g., addressing the items noted above) so they are ready to provide the required information once the forms are released, thereby minimising any last minute pressure

While the ATO has indicated its intention to support affected MNE Groups in achieving a “soft landing” in relation to the application of the GloBE Rules, its ability to provide administrative relief is limited by the multinational nature of the regime. Consequently, the Commissioner can only extend the deadlines (subject to their being a good cause for the extension) for the AIUTR and DMTR - being the more Australian oriented aspects of the lodgement obligations - but is unable to grant extensions for the GIR or the foreign lodgement notification.

Treasury Amendments:

Broadly, the proposed changes that are open for consultation seek to:

- clarify the operation of Australia’s domestic minimum tax in relation to stateless entities with an Australian nexus

- provide clarification on the allocation of domestic top-up tax amounts in the context of an income tax consolidated group

- ensure covered taxes are allocated consistent with the allocation of GloBE income for certain entities (e.g., Joint Ventures)

- add a foreign currency translation rule to provide a prescribed method for translating foreign denominated top-up taxes into Australian dollars.

- ensure Australia’s domestic minimum tax legislation functions properly

FOR MORE INFORMATION

If you have any questions or require assistance with any of your Pillar Two obligations, a list of our Pillar Two working team, their respective offices and contact details are below: