Singapore has built one of the most comprehensive ecosystems of tax incentives, grants and government support programmes designed to help businesses expand internationally.

For companies seeking to enter new markets, establish overseas operations, or pursue cross-border acquisitions, a range of schemes can help reduce expansion costs, improve cash flow, and manage investment risks.

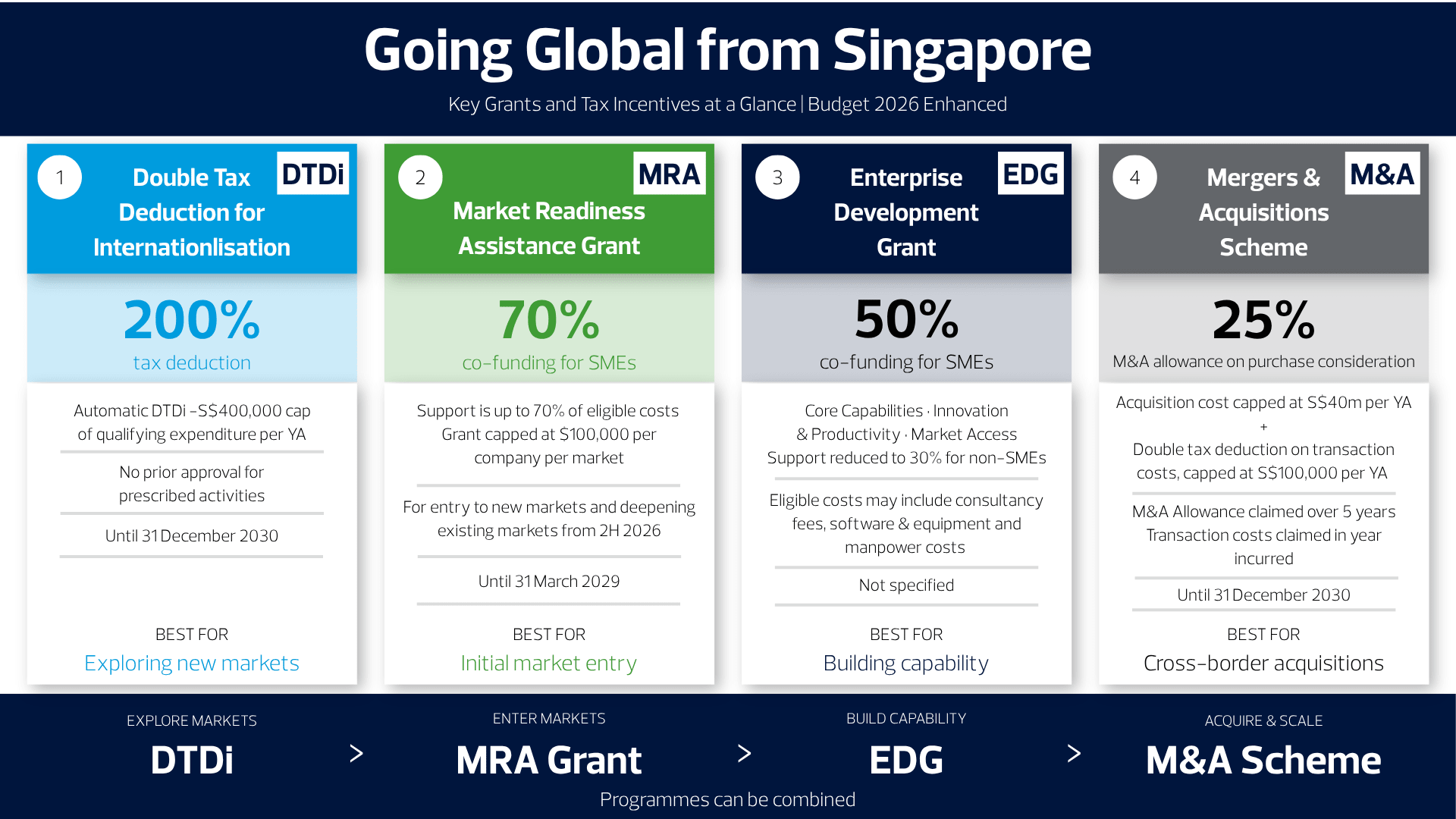

This article highlights four key programmes that Singapore companies can consider when planning international expansion.

Tips: Each programme serves a different purpose but they can often be combined as part of a broader expansion strategy — reducing costs at every stage from initial market exploration through to acquisition.

Double Tax Deduction for Internationalisation (DTDi)

The Double Tax Deduction for Internationalisation (DTDi) scheme provides companies with a 200% tax deduction on qualifying expenses incurred for international market expansion and investment development activities. The scheme has been extended to 31 December 2030, reaffirming the Government's commitment to supporting Singapore businesses in accessing global markets.

Budget 2026 further enhanced the automatic DTDi cap. With effect from YA 2027, companies can claim a 200% deduction on the first S$400,000 (up from S$150,000) of qualifying expenditure per year of assessment without requiring prior approval from Enterprise Singapore (EnterpriseSG) or the Singapore Tourism Board (STB).

Activities qualifying for automatic DTDi | |

| Market Preparation | • Design of packaging for overseas markets • Product/ service certification approved by EnterpriseSG • Market surveys/ feasibility studies New - Budget 2026 |

| Market Exploration | • Overseas market development trips/ missions • Overseas trade fairs • Local trade fairs approved by EnterpriseSG or STB • Virtual trade fairs approved by EnterpriseSG |

| Market Promotion | • Overseas advertising and promotional campaigns • Corporate brochures for overseas distribution New - Budget 2026 • Advertising in local trade publications approved by EnterpriseSG • Overseas business development New - Budget 2026 |

| Market Presence | • Master licensing and franchising New - Budget 2026 • Overseas investment study trips/ missions • Investment feasibility/ due diligence studies New - Budget 2026 |

Activities requiring EnterpriseSG approval

Other internationalisation activities may also qualify for DTDi, but are subject to prior approval from EnterpriseSG:

- Overseas trade office establishment and maintenance

- E-commerce campaign expenses targeting overseas markets

By effectively doubling the tax deduction on qualifying expenditure, DTDi significantly reduces the after-tax cost of exploring and developing overseas markets.

Tips: For qualifying expenses incurred from YA 2027 which exceed S$400,000 per YA, companies must apply to EnterpriseSG for approval before project commencement. Retrospective claims for non-automatic DTDi activities are not permitted. Companies should maintain all supporting documentation — IRAS reserves the right to disallow the claims if not supported with relevant documentation.

Market Readiness Assistance (MRA) Grant

The MRA Grant is the primary first-step grant for Singapore Small and Medium Enterprises (SMEs) expanding into overseas markets. Budget 2026 has significantly enhanced the scheme — raising the co-funding rate to 70% of eligible costs up till 31 March 2029, and, for the first time, removing the restriction that the market must be new to the company.

The MRA remains an SME-only grant. An SME is defined as a company, incorporated and operating in Singapore, with at least 30% local equity, held directly or indirectly by Singapore citizens or permanent residents. In addition, the company (or its group) must not have annual operating revenue exceeding S$100 million or employ no more than 200 employees.

What the MRA Grant covers

| Activity | Support Cap S$ |

| Overseas market promotion | 20,000 |

| Overseas business development | 50,000 |

| Overseas market set-up | 30,000 |

Eligible expenses include

- Overseas market entry strategy consulting

- Participation in overseas trade fairs

- Business matching services

- Legal and regulatory compliance costs

- Market feasibility studies

Budget 2026 enhancements — what changed

| Features | Before Budget 2026 | After Budget 2026 (from 1 April 2026) |

| Support level | Up to 50% of eligible costs | Up to 70% of eligible costs. Effective from 1 April 2026 to 31 March 2029 |

| Eligibility criteria | New markets only | Annual sales in target market must not exceed S$100,000 in any of the preceding 3 years. From second half of 2026, “new to market” criterion will be removed. Applicants can include eligible costs incurred to deepen presence in existing overseas markets. |

| Total Grant cap per company per market | S$100,000 | S$100,000 (unchanged) |

| Scheme duration | Will expire on 31 March 2026 | Enhanced booster period - 1 April 2026 to 31 March 2029 |

Tips: The removal of the “new market” criterion means that in practice, from the second half of 2026, a Singapore SME that already has a presence in an overseas market (e.g. Malaysia) but wishes to deepen its commercial activities or strengthen its brand in that market can now access MRA funding for those activities. Previously, once a company had entered a market, MRA support for that market was no longer available (unless sales remained below S$100,000).

Enterprise Development Grant (EDG)

The Enterprise Development Grant (EDG) supports business entities registered and operating in Singapore who are undertaking projects that help them upgrade, innovate, grow and transform their business including overseas market expansion.

The applicant entity must have at least 30% local equity held directly or indirectly by Singapore citizens and/or Permanent Residents, determined by the ultimate individual ownership, and be in a financially viable position to start and complete the project.

Qualifying projects undertaken by local SMEs will receive EDG of up to 50% of eligible project costs. For non-SMEs, the support is up to 30%.

EDG projects typically fall under the following three main categories.

| Category | Examples of In-scope Projects |

| Core Capabilities |

|

| Innovation and Productivity |

|

| Market Access |

|

Qualifying costs may include

- Third-party consultancy fees

- Software and equipment purchases

- Internal manpower costs associated with the project

Unlike the MRA scheme, EDG supports larger and more strategic transformation projects, including those involving international market expansion.

Mergers & Acquisitions (M&A) Scheme

Organic expansion (i.e. setting up a new office, hiring local (foreign) staff and building a customer base from scratch) is not always the fastest or most effective route to gain entry into a foreign market. Many Singapore companies have realised that acquiring an established local (foreign) business enables faster market access, helps in gaining an immediate customer base, and grants access to necessary local business licences and management talent that might otherwise take years to build.

The M&A scheme in Singapore was designed to support this organic growth path through strategic acquisitions, helping companies expand market presence, enhance capabilities and gain a competitive edge in global market. Recently extended to 31 December 2030, the scheme provides meaningful tax relief on the cost of qualifying share acquisitions, reducing the after-tax cost of overseas deals and improving the financial case for M&A -driven internationalisation.

Qualifying conditions

A qualifying share acquisition is one that results in the acquiring company owning:

- 20% to 50% of ordinary shares of the target (if less than 20% was owned prior to the acquisition); or

- More than 50% of ordinary shares of the target (if 50% or less was owned prior to the acquisition).

Tax benefits under the M&A scheme are granted to an acquiring company in respect of a qualifying share acquisition, subject to both the acquiring company and the target meeting all the respective conditions mentioned in the table below.

| The acquiring company must: | The target (or its wholly owned subsidiary) must: |

|

|

Tax benefits under the scheme

| Tax Benefits | Details |

| M&A allowance on purchase consideration |

|

| Double tax deduction on transaction costs |

|

An illustrative example

| A Singapore company acquires an overseas target | Amount/Tax Benefits S$ |

| Acquisition value | 20,000,000 |

| M&A allowance | |

| M&A allowance at 25% | 5,000,000 |

| Claim of M&A allowance per year of assessment | 1,000,000 |

| Annual tax savings -at 17% | 170,000 |

| Total tax savings from M&A allowance for 5 years | 850,000 |

| Double tax deduction on transaction costs | |

| Total transaction costs for the acquisition deal, say | 100,000 |

| Double tax deduction -200% x S$100,000 | 200,000 |

| Tax savings at 17% | 34,000 |

| After-tax transaction costs -S$100,000 less S$34,000 | 66,000 |

The M&A allowance coupled with the double tax deduction for qualifying transaction costs will help ease cashflow and reduce financial burden associated with M&A transactions. These tax benefits can meaningfully reduce the effective cost of qualifying strategic acquisitions.

Bringing It All Together

While each programme serves a different purpose, they can often be combined as part of a broader international expansion strategy.

For Singapore companies looking to grow internationally, leveraging these schemes effectively can significantly lower expansion costs, improve investment returns, and reduce execution risk. To summarise: