This article answers the following questions:

- What is a tax loss?

- How to utilise a tax loss?

- What impacts the likelihood of a tax loss being utilised?

Over the course of a company's financial year, numerous economic events occur, having a diverse impact on its financial standings. It's important to remember that the consequences of these events are not always identical under tax and accounting law. These discrepancies stem from the differing objectives of the two regimes, differing principles for valuing assets and liabilities, and the functions these two sets of regulations perform. As a result, temporary differences (taxable and deductible) are recorded in the documentation, leading to the creation of deferred tax assets or liabilities. How should they be utilised?

The best way to identify discrepancies in an entity's records is to compare the carrying amount with the tax base and then determine which of these differences are permanent and which are temporary.

Detected temporary differences are the basis for the creation of deferred tax assets and provisions, which are then shown on the company's balance sheet and reflected in the statement of financial position.

What is a tax loss?

A tax loss occurs when tax-deductible costs exceed taxable revenues. According to Polish regulations1:

- tax loss can be carried forward over the next five tax years,

- 50% of the loss value can be utilised in a given tax year (the tax loss can therefore be fully utilised within two years, at the earliest),

- If a tax loss is not utilised within five years, the right to deduct it expires.

Since 2019, Polish legislation has allowed taxpayers for a one-time tax loss utilisation of up to PLN 5 million. Only the excess of this amount is utilised based on principles that allow for the deduction of a maximum of 50% of the loss in a single year.

This means that if the entity earns sufficiently high income from the same source from which the loss was incurred (and the loss itself exceeds PLN 5 million), the entity will make the full deduction within two tax years at the earliest (deducting 50% each year).

Similarly to deductible temporary differences, an entity may create a deferred tax asset on a tax loss incurred, provided that the entity is able to reliably demonstrate in its documentation that it will generate sufficient taxable income in subsequent years for the loss to be utilised against it.

Learn more about our services

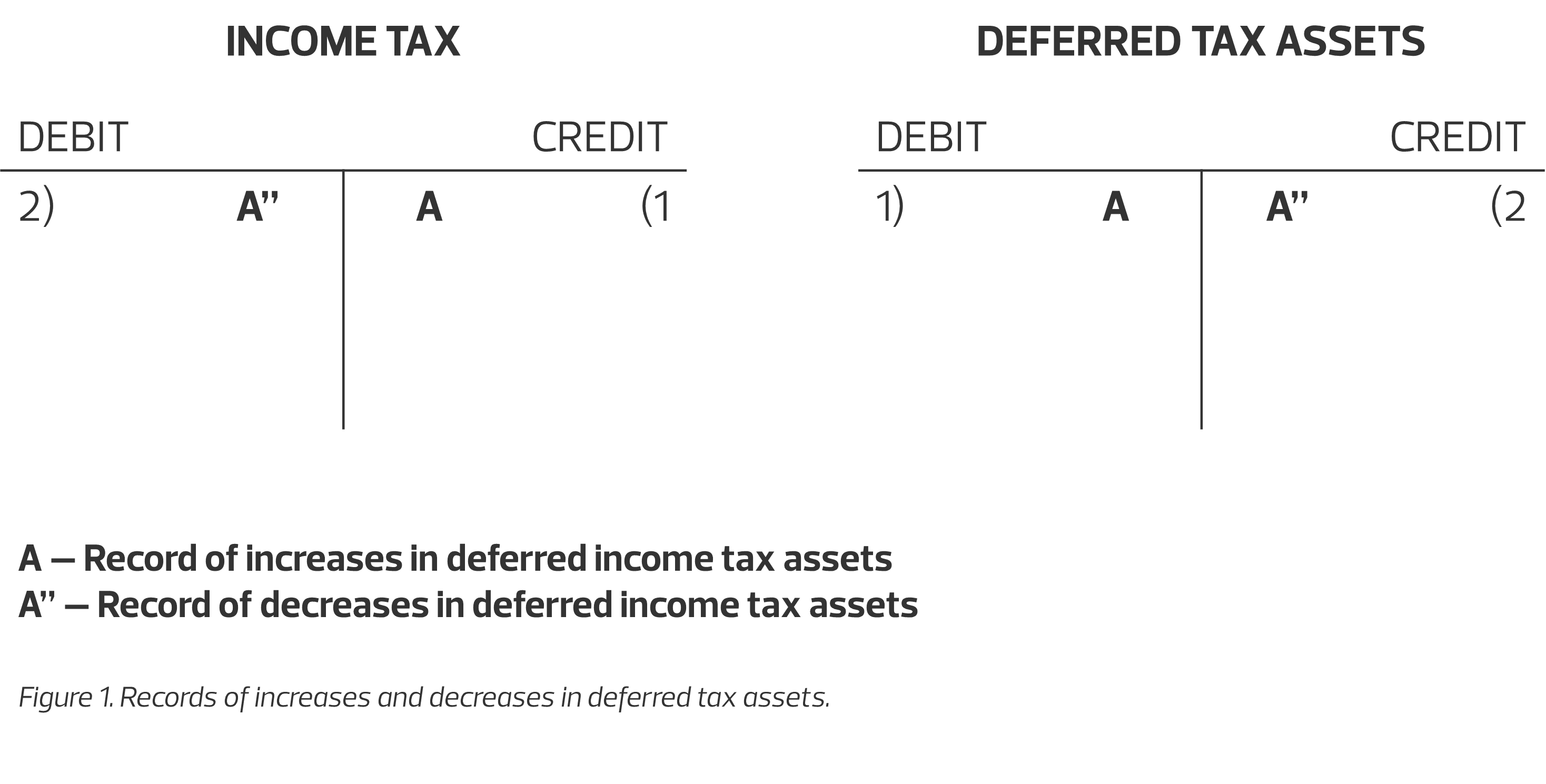

Accounting records of deferred tax assets

How should accountants recognise deferred tax assets in accounting ledgers when there is an increase or decrease?

- An increase in assets (creation of an asset on a tax loss) is recorded in the books on the debit side (left) – of the asset account; at the same time, it is recognised as a decrease in income tax on the credit side (right), in the statement of financial position.

- A decrease in assets occurs at the time of tax loss utilisation – the asset is then redeemed, which leads to an increase in tax on the balance sheet.

How to utilise a company's tax loss?

Activation of an entity’s tax loss involves the creation of an asset by the accounting team, and its amount is determined using the formula specified in the regulations:

tax loss × expected income tax rate

The so-called "activated loss" constitutes a company asset and can only be recognised in that portion of the assets for which there is a realistic probability of the loss being utilised. In practice, this means that accountants must (either on their own or with the help of tax advisors) carefully analyse whether the company will generate sufficient taxable income over the next five years.

The probability of utilising a loss is affected by, among others:

- the nature of the events causing the loss (e.g. incidental, one-off costs will increase the chances of future income),

- the scale of taxable temporary differences that will increase the tax base in the future,

- tax planning capabilities of the business.

It is worth emphasising that similar tax loss utilisation principles apply not only in the Polish legal system – they are also stated in International Accounting Standards (IAS)2. According to these standards, deferred tax assets may be recognised in the accounting ledgers only if there is a reasonable expectation that they will be utilised in the future.

When utilising a company's tax loss, consider the support of specialists

Proper tax loss utilisation and tax planning allow businesses operating in Poland to maintain liquidity and manage their finances more effectively, translating into tangible business gains. However, understanding domestic and international regulations requires expertise and insight into ever-changing legal regulations.

Therefore, we encourage you to take advantage of the support offered by RSM Poland's tax advisory and audit teams. Our experts provide professional assistance tailored to the specific needs of each entity, helping Polish and foreign businesses optimise their internal tax and financial processes.

Sources:

1 Article 7(5) of the Corporate Income Tax Act of 15 February 1992.

2 International Accounting Standard /IAS 12, paragraphs 14, 34-36.