The Australian Securities & Investments Commission (“ASIC”) recently issued a media release on 19 May 2025 outlining the financial reporting and audit focus areas for 30 June 2025 and subsequent year-ends

The key financial reporting focus areas emphasise matters that often involve significant judgement by preparers of financial statements, and reflect those areas where ASIC financial reporting surveillance will focus.

Ralph Martin, RSM Australia’s National Technical Partner stated: “ASIC’s Focus Areas highlight the importance of exercising care in making key estimates and judgements, especially in light of recent economic uncertainty around global trade, and the resulting capital market volatility. While several areas have recurred for many years, preparers may need to take a fresh look at them,

The financial reporting focus areas include:

Enduring focus areas for financial report reviews

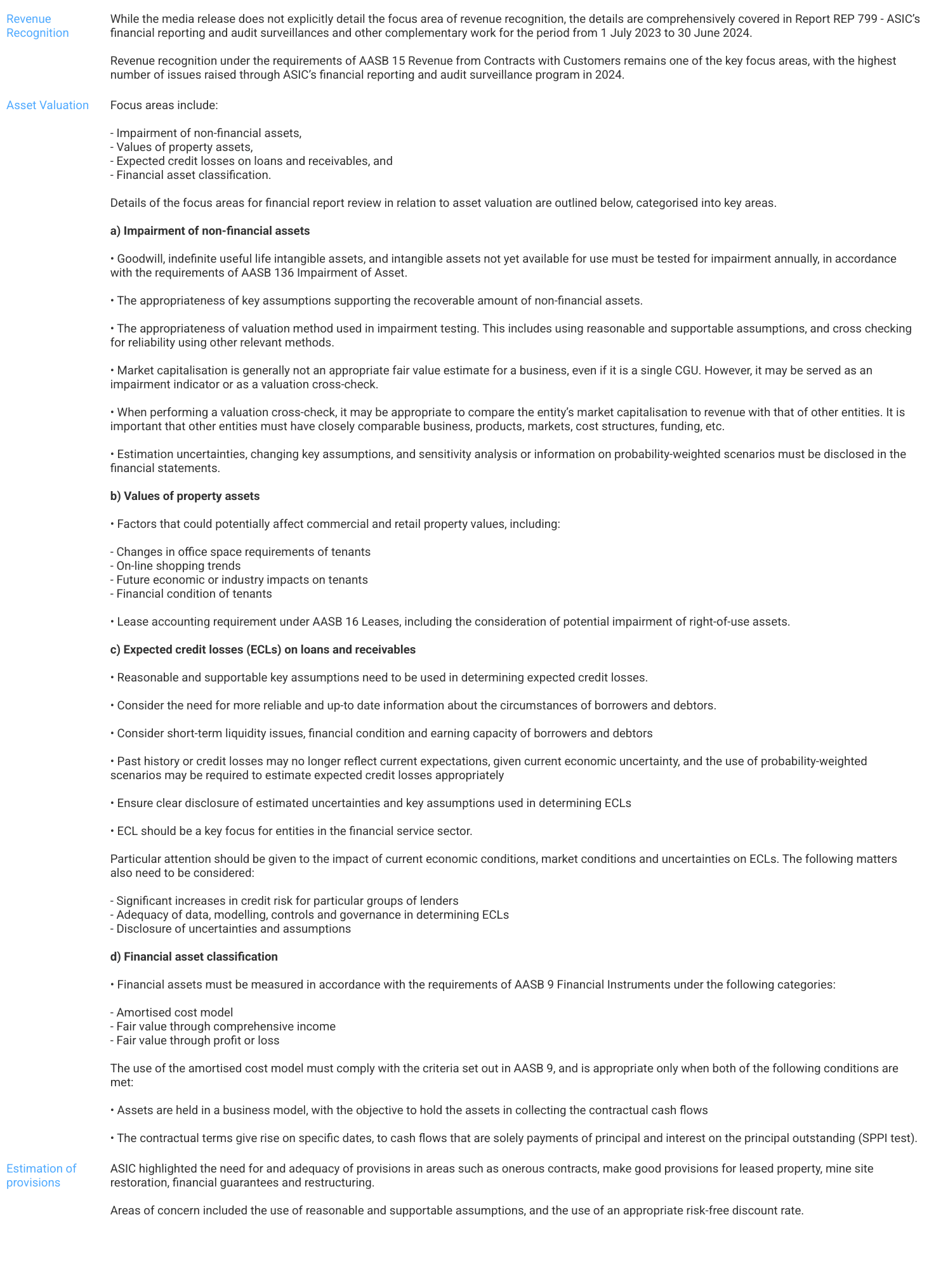

- Revenue Recognition

- Asset Valuation

- Estimation of provisions

In addition, ASIC focus area also include specific aspects of financial statements disclosures.

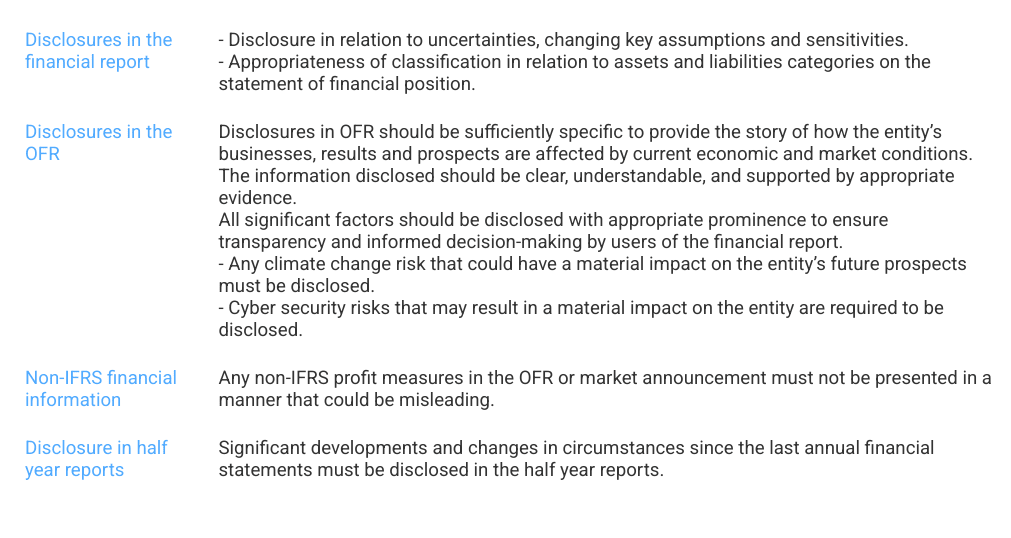

These include general disclosures in the financial report, as well as disclosures in the Operating and Financial Review (OFR).

Particular emphasis is placed on the disclosure of subsequent events, highlighting the importance of reviewing events occurring after year end and before the financial statements is finalised.

Financial statements’ Disclosure

Following are the key focus areas in relation to the financial statement’s disclosure:

Audit focus areas

In addition to its ongoing focus areas, ASIC has highlighted the following specific matters as audit focus areas. A selection of audit files will be reviewed as part of ASIC’s 2025 to 2026 surveillance program:

- Registrable superannuation entities

- Previously Grandfathered entities

- Sustainability reporting standards

- Auditor conflicts of interest

- Consolidated entity disclosure statement.

Registrable superannuation entities

Due to the changes of the regulations, Registerable superannuation entities (“RSE”) were required to lodge audited financial statements with ASIC for the first time in FY 2024.

Two focus areas have arisen from ASIC surveillance activities on RSEs:

1. The measurement and disclosure of investment portfolios

2. Disclosure of marketing and advertising expenses

In the 2025 to 2026 surveillance program, ASIC will continue to review the remaining RSE financial statements and a selection of RSE audit files.

Financial reports of previously grandfathered entities

In August 2022, a legislative exemption provided to large grandfathered proprietary companies were removed due to the Senate amendments made to the Treasury Laws Amendment (2022 Measures No.1) Act 2022. RSM’s article provides further details.

As a result of the legislative amendments, large grandfathered proprietary companies with a reporting year end on or after 10 August 2022 were no longer exempt from lodging the financial statements with ASIC. Consequently, compliance with this requirement has become a key focus area for ASIC.

ASIC has noted that some of the affected companies have still not lodged their financial statements since the exemption was lifted. ASIC has indicated it will continue to monitor compliance in this area and take appropriate action where necessary.

Sustainability reporting standards

The mandatory sustainability reporting requirements will be introduced in different phases, with entities categorised as Group 1, Group 2, and Group 3 based on specific thresholds and criteria. For Group 1 entities, sustainability reporting will be mandatory for financial years commencing on or after 1 January 2025.

ASIC confirmed that it will review a selection of sustainability reports for the reporting period 31 December 2025 as part of the 2025 – 2026 surveillance program, to assess compliance with the new reporting requirements.

RSM’s guide provides an overview of readiness for mandatory sustainability reporting.

Consolidated Entity Disclosure Statement

Consolidated Entity Disclosure Statements were required for the first time for 30 June 2024 year-ends.

Information Sheet 284 (INFO 284) Public Companies to include a consolidated entity disclosure statements in their annual report has been updated. The update is relevant to all public companies for financial years commencing on or after 1 July 2024, with the first applicable reporting period being YE 30 June 2025.

These include the recent legislative amendments of the clarification of the tax residency disclosure requirements, as outlined below:

- Entities that are Australian tax residents and also tax residents in one or more foreign jurisdictions are now required to disclose all applicable foreign tax residencies.

- For the purposes of the Consolidated Entity Disclosure Statement, the term of “Australian resident” is now defined for partnerships and trusts.

Further information

If you would like to discuss about the topics discussed in this article, please contract your local RSM office.