AUTHORS

Common control transactions are a difficult and subjective area of financial reporting, as there is presently no accounting standard that deals with them.

In this article, we consider how they are usually treated, and also look at the proposals of the current IASB project to standardise accounting for common control transactions.

How should you account for common control transactions?

Many groups of companies enter into agreements to restructure their group. This can occur for various reasons, including taxation, structuring, limitation of liability, or business simplification.

When these restructuring agreements are entered into, it is important to know whether common control exists or not as this determines the appropriate accounting treatment.

A transaction between two entities which are owned by the same ultimate parent is usually referred to as a “common control transaction.” Common control transactions are specifically scoped out of AASB 3 Business Combinations, which states that “a business combination involving entities or businesses under common control’ is a business combination in which all of the combining entities or businesses are ultimately controlled by the same party before and after the combination, and that control is not transitory.”

Australian Accounting Standards, and IFRS, do not currently specify how to account for common control transactions. In the absence of specific requirements, companies tend to provide relatively little information about such combinations, and report on them using one of several commonly accepted methods.

When does common control exist?

Two entities are commonly controlled when they have the same ultimate ownership. This ultimate control can be held by any of the following:

- A company or other entity

- An individual

- A group of shareholders that has an agreement to act collectively

- A family group which acts collectively (even where there is no formal agreement to do so).

While common control is easily determined where one party owns a controlling interest in both entities, other situations may be more complex:

Example 1

Company A and Company B are each owned by three shareholders, each of whom owns 33% of the shares of both companies. The three shareholders are unrelated, and do not have any shareholders agreement or similar arrangement which compels them to vote or act together.

Company A and Company B are not under common control, even though they are owned by the same three parties, as no individual or group has control of either company.

Example 2

Company C and Company D are each owned by three shareholders, each of whom owns 33% of the shares of both companies. However, two of the shareholders are brothers, and have a history of always acting and voting together in making decisions about the management of the two companies..

Company C and Company D are under common control, since there is a single family group which acts collectively to control the two entities.

Accounting for common control transactions

While no specific requirements exist within Australian Accounting Standards, the there are two commonly accepted methods of reflecting common control transactions in financial statements:

- The acquisition method as set out in AASB 3; or

- The pooling of interest method

The acquisition method under AASB 3 is the same process that would be used for the acquisition of a business which was not under common control.

The pooling of interest method is sometimes referred to as “merger accounting”, "carry-over accounting”, or the “predecessor values method.”

We believe that if an entity does not adopt an accounting policy of using the acquisition method under AASB 3, or if the transaction is not in substance an acquisition of a business, the pooling of interests method should be applied when accounting for business combinations under common control.

AASB 3 makes no reference to the pooling of interests method, other than to reject it as a method of accounting for business combinations which are not under common control. Various local standard-setters have issued guidance and some, including US GAAP and UK GAAP allow or require a pooling of interests type method in particular circumstances to account for business combinations under common control.

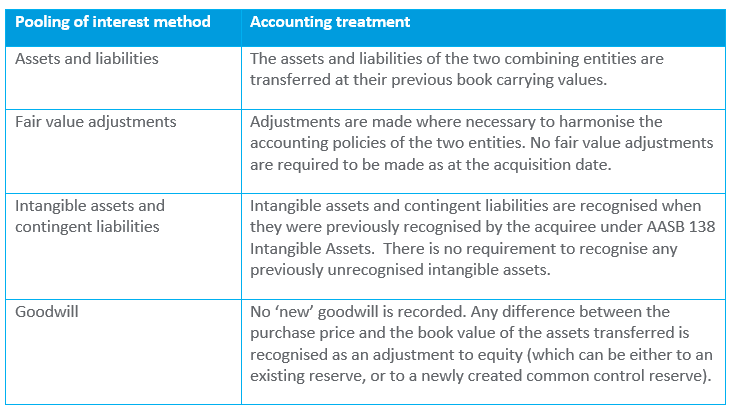

The pooling of interests method involves the following:

While both methods – the pooling of interests method and the acquisition method - are permissible under IFRS, in our view, for most common control transactions, the “pooling of interest” method is likely to be the more appropriate choice based on the following factors:

- It may better represent the substance of the transaction, being a group reorganisation rather than a genuine business acquisition.

- If the acquisition method were adopted, there would need to be an assessment of the fair value of the assets, including any previously unrecognised but separately identifiable intangible assets. This may be time-consuming, judgmental, and may incur substantial additional expense if specialist valuation services are required.

- The acquisition method may result in the recognition of additional goodwill. This appears inconsistent in principle with the requirement in Australian Accounting Standards that internally generated goodwill cannot be recognised. Furthermore, if additional goodwill were to be recognised as a result of this transaction, it would need to be tested for impairment annually – a potentially onerous exercise.

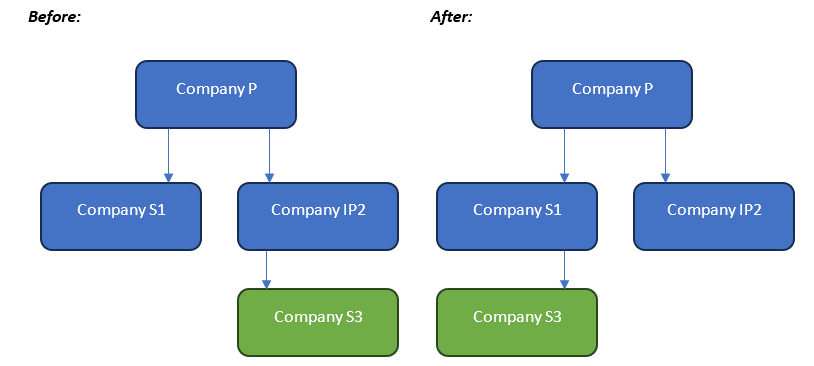

Example 3 – Application of the Pooling of Interest Method

Company S1 pays 80 to Company IP2 to acquire all of the shares in Company S3. The book value of Company IP2’s investment in S3 is 100 and the fair value of S3 is 130.

In applying pooling of interest method, the acquirer (S1) and the transferor (IP2) record the following entries, recognising the difference between the book value of the transferee (S3) and the consideration paid/received as an equity transaction with the shareholder (P) – i.e. as if S3 had been purchased for its book value of 100 and the difference of 20 paid back as a distribution made/contribution received.

Entries in S1:

Dr Investment in subsidiary (S3) 100

Cr Cash 80

Cr Contribution (equity) 20

To recognise contribution in S3

Entries in IP2:

Dr Cash 80

Dr Distribution (equity) 20

Cr Investment in subsidiary (S3) 100

To recognise disposal of S3

For more information

For any queries on common control please contact Ralph Martin (ralph.martin@rsm.com.au) or Nadia Hattingh (nadia.hattingh@rsm.com.au).