The Australian Government first introduced the concept of a Significant Global Entity (SGE) in 2015 to increase the transparency of multinational groups with global group turnover in excess of AUD$1bn.

It was designed to align with the Organisation for Economic Co-operation and Development (OECD) Base Erosion and Profit Shifting (BEPS) initiatives relating to Country-by-Country reporting (CbCR).

However, in 2020 the Australian government amended and expanded the definition of an SGE to ensure that the definition applied consistently to all types of entities, including members of large multinational groups headed by individuals, partnerships, private companies, trusts, investment entities (private equity groups) and other entities.

However, as a consequence, even a small Australian company can be included under the SGE provisions, depending on their ownership structure.

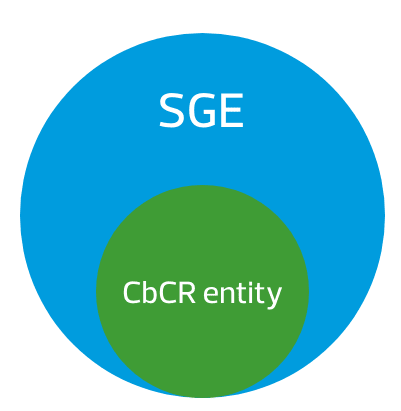

This new SGE definition extended further than the OECD BEPS initiative, so the definition of a CbCR entity was also introduced, to ensure that Australia’s additional compliance filing requirements remained closely aligned to the OECD’s recommendation. The below diagram shows that all CbCR entities are an SGE, though not all SGEs are CbCR entities.

As such, CbCR entities are required to attend to the additional compliance filing requirements, most notably the lodgement of General Purpose Financial Statements and Country by Country Reporting as discussed further below.

1. General Purpose Financial Statements (GPFS)

A CbCR entity that is a corporate tax entity with an Australian presence must file GPFS with the Commissioner by the lodgement due date of its income tax return in line with Section 3CA of the TAA1953. Legislative exemptions may be applicable if the GPFS has already been lodged with the Australian Securities and Investment Commission (ASIC), though the Australian Tax Office (ATO) does not have the authority to provide exemptions for GPFS. However, the ATO can grant extensions.

Filing GPFS with the ATO via the tax agent portal can often be overlooked by taxpayers who do not have audit or filing requirements with ASIC, or by tax agents who are unfamiliar with these rules.

The Commissioner will give a copy of the GPFS to ASIC, which will appear on ASIC's register and will be made publicly available. This has raised some privacy concerns for multinationals, where this information may not have previously been made public.

Taxpayers should consider how they will satisfy their GPFS reporting requirements in advance of their year-end to ensure lodgement can be made by the due date. Failure to do so may result in significant late lodgement penalties from the ATO.

2. Country by Country Reporting (CbCR)

A CbCR entity will also be required to lodge its CbC Reporting filings in Australia within 12 months of year-end, in line with Subdivision 815-E of the ITAA 1997. This includes three reports to the ATO detailing its global financial activities. These are:

- The CbC report: Contains information about where the economic activity is undertaken and profits that are reported by the global group.

- The Master file: Contains a high-level description of the group’s global business operations, including an outline of the group structure as well as intangibles and intercompany financing.

- The Local file: Contains information about a local entity’s management structure and business strategy, cross border related party transactional data, including information about how transfer pricing decisions have been made as well as financial accounts for the Australian entity.

The parent company will usually prepare most of the work relating to the CbC report and the Masterfile, though the Australian entity will need to ensure a CbC report notification is submitted to the ATO along with the Masterfile. Australia follows the OECD for both of these reports. If the parent company is not expecting to have a CbC report or Masterfile prepared for the Group, they may be able to seek certain exemptions from the ATO, though it is best to raise these issues as soon as possible to ensure they qualify.

However, local assistance is usually required to prepare the Australian Local File, in part because Australia’s Local file is quite different to an OECD Local File. The Australia Local File consists of a Short form, Part A and Part B and requires detailed transactional information to be reported to the ATO, including intercompany agreements, making it a more data-based submission.

Multinationals should note that an Australian Local File does NOT constitute transfer pricing documentation, as Australian transfer pricing documentation is more aligned to an OECD Local File. Australian transfer pricing documentation would include (amongst other things) an analysis regarding the actual conditions of the taxpayer for the income year, how these align with the arm’s length conditions and whether a transfer pricing benefit arises in Australia.

Additional SGE provisions

SGEs no longer have the above additional compliance requirements, as these are reserved for CbCR entities only. However, there are a number of anti-avoidance provisions and other penalties that can apply to SGEs, as summarised below.

Multinational Anti-Avoidance Law (MAAL)

MAAL applies to certain schemes on or after 1 January 2016, irrespective of when the scheme commenced. It is designed to counter the erosion of the Australian tax base by multinational entities using artificial or contrived arrangements to avoid attributing business profits to Australia through a taxable presence in Australia.

Broadly, the new law will apply if under the scheme, or in connection with the scheme:

- A foreign entity supplies goods or services to an Australian customer;

- An Australian entity, that is an associate of or is commercially dependent on the foreign entity, undertakes activities directly in connection with the supply;

- Some or all of the income derived by the foreign entity is not attributable to an Australian permanent establishment; and

- The principal purpose, or one of the principal purposes of the scheme, is to obtain an Australian tax benefit or to obtain both an Australian and foreign tax benefit.

MAAL has been inserted into Part IVA of Australia’s domestic anti-avoidance legislation, which is not affected by the operation of Australia’s double tax agreements.

Diverted Profits Tax (DPT)

The DPT came into effect for income years commencing on or after 1 July 2017 and is imposed at a rate of 40%. The introduction of the DPT was designed to ensure that the tax paid by SGEs properly reflects the economic substance of their activities in Australia and aims to prevent the diversion of profits offshore through contrived arrangements.

Broadly, the new law applies if under the scheme, or in connection with the scheme:

- A taxpayer ('the relevant taxpayer') has obtained a tax benefit in connection with the scheme in an income year.

- A foreign entity, that is an associate of the relevant taxpayer, entered into or carried out the scheme or is otherwise connected with the scheme.

- The principal purpose, or one of the principal purposes of a person who entered into or carried out the scheme, is to enable the relevant taxpayer to obtain an Australian tax benefit or to obtain both an Australian and foreign tax benefit.

- There are some exceptions: namely, the $25m income test, the sufficient foreign tax test and the sufficient economic substance test. These should be explored in detail if DPT appears relevant to your business.

Significant increase in penalties

The significant increase in penalties applicable to SGEs is one of their biggest practical challenges. These changes include:

- Tax avoidance and profit-shifting scheme penalties are doubled.

- The penalty for making a false or misleading statement is doubled.

- Failure to lodge on time penalties have been multiplied by 500 times – a late lodgment of one day late can currently result in a penalty of $165,500 increasing to $782,500 for a lodgement up to 113 days late1.

Given the harsh penalty regime in place for SGEs, it is important to ensure that they are addressing their Australian tax obligations in a timely manner. The increased penalties are not just restricted to late lodgement of GPFS and CbC Reporting, but a number of the ATO lodgments including:

- Income Tax Return

- Fringe Benefits Tax Return

- Business Activity Statement

- Instalment Activity Statement.

SGEs should continue to review their internal processes to ensure they remain vigilant with their reporting obligations, as the imposition of penalties could pose a serious financial risk. The ATO has previously been lenient to SGEs, however these rules have now been in place for some time, and so we are now seeing these penalties being issued more frequently.

Key Takeaways

Given the additional rules that are applied to SGEs, it is important to inform your tax adviser of your SGE status or work with your tax adviser to determine your SGE status. External advisers often do not have access to the global structure of their clients, and as such it is important to raise this with your tax advisers at the outset if you are concerned about your SGE status. Importantly, any changes in your structure or business operations may result in a change to your SGE status and as such, this should be reviewed on an ongoing basis.

If you are considered an SGE, you should ensure that any ATO filings are lodged on time to avoid any late filing penalties being imposed. If you are an SGE that is also a CbCR entity, this would extend to the GPFS and CbCR filings as well.

FOR MORE INFORMATION

If you need any assistance, please reach out to Danielle Sherwin.

record-keeping")