In the 2023–24 State Budget, the Victorian Government announced that land transfer duty (stamp duty) on commercial and industrial property will be abolished and replaced with the Commercial and Industrial Property Tax (CIPT), which will apply annually based on unimproved land value. The Victorian Government contend that the CIPT represents a more efficient tax that will accelerate business growth and boost jobs in Victoria.

On 21 March 2024, one day after a pertinent Media Release from Victorian Treasurer, Hon. Tim Pallas MP[1], the Commercial and Industrial Property Tax Reform Bill 2024 (Vic)[2](the Bill) was introduced into the Legislative Assembly.

The Bill will give effect to the CIPT and reform the taxation of commercial and industrial property through amendments to the Duties Act 2000 (Vic) and the Taxation Administration Act 1997 (Vic.).

Set out below are some Frequently Asked Questions pertaining to the CIPT as currently drafted.

How will the CIPT apply?

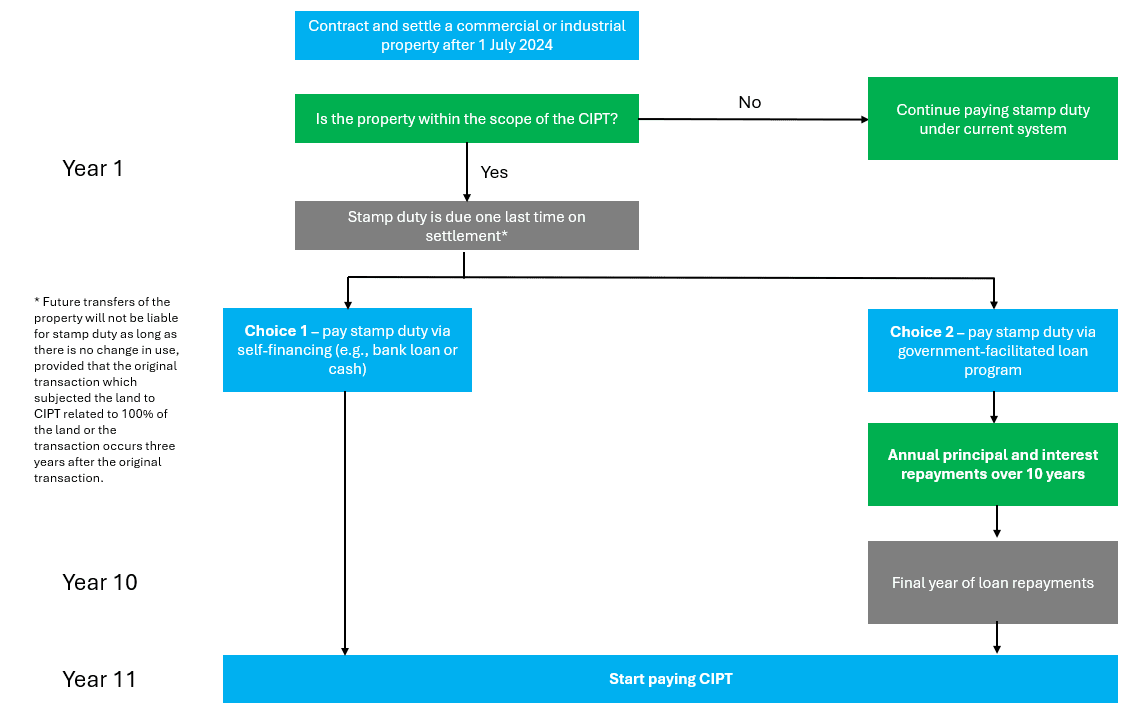

It is proposed that the CIPT will apply at a per-annum rate of 1% (0.5% for BTR) to an in-scope property’s unimproved value, with no tax-free threshold. The CIPT is expected to apply to transactions involving in-scope property from 1 July 2024, unless the transaction is effected by an agreement or arrangement entered into prior to that date.

Subject to the availability of existing full exemptions from stamp duty, which will continue to apply, where a ‘qualifying dutiable transaction’ or ‘qualifying landholder transaction’ relating to an interest of 50% or greater in a property with a ‘qualifying use’ occurs on or after 1 July 2024, final stamp duty will be payable on the land, and CIPT will become payable 10 years after that date.

Subject to a specific anti-avoidance provision, subsequent transactions in connection with the same will not be chargeable with stamp duty provided that:

- The original transaction that subjected the land to CIPT related to 100% of the land; or

- The subsequent transaction occurs at least three years after the original transaction.

The following diagram illustrates the process:

KEY AREAS OF INFORMATION ARE BELOW:

A transaction will be a ‘qualifying dutiable transaction’ and therefore in-scope for the purposes of the CIPT where a dutiable transaction (other than certain leases or an economic entitlement acquisition) occurs on or after 1 July 2024, and the dutiable transaction:

- is in respect of a prescribed interest in land (e.g., an estate in fee-simple); and

- is not exempt from stamp duty or eligible for an intra-group transaction concession; and

- the dutiable transaction relates to an interest of 50% or more in the land (subject to integrity rules concerning the aggregation of certain transactions involving associated persons);

Alternatively, a transaction will be a ‘qualifying landholder transaction’ and therefore in-scope for the purposes of the CIPT where the transaction isa ‘relevant acquisition’ (i.e., a 50% acquisition in a private corporation or 20% interest in a private trust that holds a prescribed interest or prescribed interests in land (e.g., an estate in fee-simple) with a ‘qualifying use’), and:

- The ‘relevant acquisition’ is not exempt from stamp duty or eligible for an intra-group transaction concession; and

- The ‘relevant acquisition’ relates to a ‘qualifying interest’ in land, i.e., an indirect interest of 50% or more in land (again subject to integrity rules concerning the aggregation of certain transactions involved associated persons).

It is worth noting that land will also become subject to the CIPT regime where there is a consolidation or subdivision of titles, and 50% or more of the area of the consolidated, or the aggregate subdivided land, has been subject to the CIPT.

Land will have a ‘qualifying use’ where:

- The Australian Valuation Property Classification Code (AVPCC) allocated to the land as part of the valuation process under the Valuation of Land Act 1960 (Vic.) falls in the ranges of 200-499 or 600-699[3];

- The property has been allocated more than one AVPCC in the latest valuation, at least one of which is outside the abovementioned ranges, but the land is used primarily or solely for a use described in the abovementioned ranges; or

- The land is used primarily or solely for ‘eligible student accommodation’ (a defined term).

Existing stamp duty concessions for commercial and industrial properties, including the regional concession, will all continue to be available for the final stamp duty payment.

Where a transaction involving commercial and industrial property attracts a full exemption from stamp duty (e.g., deceased estates, transfers on a change of trustee, or transfers between spouses or de facto partners), the transaction will not cause the property to be subject to the CIPT. However, transfers of in-scope property eligible for concessions such as the Regional Commercial and Industry Duty Concession will become subject to the CIPT, where the abovementioned requirements are satisfied.

If land subject to the CIPT undergoes a change of use to a ‘non-qualifying use’, such as residential use, duty may be payable on a dutiable transaction or relevant acquisition in respect of the land that was otherwise exempt from duty.

Foreign owners will be liable for the CIPT. Relevantly, there is no ‘absentee owner surcharge’ on the CIPT.

This reform does not make any changes to existing land tax arrangements in Victoria – Landholders will still be subject to land tax. Existing land tax exemptions will continue to apply[4]

To smooth the transition to the new tax system, the Government will give purchasers of commercial or industrial property (who meet the relevant eligibility criteria) the option of accessing a government-facilitated transition loan as an alternative to self-financing the upfront final stamp duty amount. The loan will be on commercial terms at a fixed interest rate and administered by the Treasury Corporation of Victoria. The transition loan will free up capital for businesses so they can expand or employ more workers.

The transition loan can be repaid in fixed instalments over 10 years.

The loan will be available where all the following conditions are satisfied:

- Australian citizens/permanent residents or an Australian business;

- the first purchaser of a commercial or industrial property where settlement occurs for contracts entered into on or after 1 July 2024;

- purchasing property up to a maximum purchase price of $30 million; and

- approved for finance from an Authorised Deposit-taking Institution or other approved lender for the subject property.

Where a transitional loan is availed of, the Treasury Corporation of Victoria will have a first ranking statutory charge over the interest in the land in relation to the loan. This will be registered on title to inform prospective purchasers.

General anti-avoidance provisions will apply to schemes intended to either avoid entry into the new tax regime or avoid application of the new tax.

- Bill link: Commercial and Industrial Property Tax Reform Bill 2024 (legislation.vic.gov.au)

- Explanatory Memorandum link: Commercial and Industrial Property Tax Reform Bill 2024 (legislation.vic.gov.au)

- Hansard link: VIC LA Hansard

- State Revenue Office Victoria: https://www.sro.vic.gov.au/news/commercial-and-industrial-property-tax-1-july-2024

- Department of Treasury and Finance website: https://www.dtf.vic.gov.au/funds-programs-and-policies/commercial-and-industrial-property-tax-reform

FOR MORE INFORMATION

For further information regarding the Victorian Commercial and Industrial Property Tax please contact Mira Brewster, Michael Watkins, or Simon Aitken.

[1] Stamp Duty Reforms to Back Victorian Businesses

[2] Commercial and Industrial Property Tax Reform Bill 2024 (legislation.vic.gov.au)

[3] AVPCCs are accessible at Appendix A to the Victorian Department of Environment, Land, Water and Planning’s 2023 Valuation Best Practice Specifications Guidelines.

[4] Land tax exemptions | State Revenue Office (sro.vic.gov.au)

now")