This article answers the following questions:

- What are qualifying assets?

- How should specific borrowing costs be recognised in the accounts?

- What liabilities are covered by general financing?

External borrowing costs (such as interest on loans and borrowings, fees or exchange differences) often constitute a significant element of a company’s cost structure, particularly during periods of intensive investment. Why? When an entity produces assets for which the production, construction or preparation is a lengthy process, part of these costs may – under certain conditions – be capitalised, i.e. added to the initial value of the asset. Capitalisation, in turn, directly affects the entity’s financial result and the carrying amount of assets, which is why its correct application is crucial for the reliability of financial statements. How do Polish and international regulations govern this aspect of accounting, and what should be done to avoid errors when recognising borrowing costs?

Legal basis for capitalising borrowing costs

Methods for capitalising borrowing costs are governed by both domestic and international accounting standards:

- Accounting Act – indicates that borrowing costs may increase the cost of producing a given asset if they are directly attributable to its production. In the Polish framework, particular importance is attached to Article 28(4) and (8) of the Accounting Act, as well as guidance contained in two additional documents:

- National Accounting Standard No. 11 “Tangible assets” (NAS 11),

- National Accounting Standard No. 13 “Cost of production as a basis for measuring products” (NAS 13),

- International Accounting Standard 23 “Borrowing costs” (IAS 23) – a standard entirely dedicated to borrowing costs, introducing uniform capitalisation rules at the international level.

Differences between domestic and international approaches

- Domestic regulations place greater emphasis on documentation and the direct relationship between the costs analysed and the investment.

- International standards adopt a broader approach to capitalisation, including general borrowing costs.

For entities that prepare financial statements in accordance with domestic regulations but belong to a capital group requiring reporting under International Financial Reporting Standards (IFRS), the scope of capitalisation may differ. Such entities should bear in mind that adjustments may be necessary in financial statements prepared for audit or in reporting packages submitted to the group. In case of doubt, it is advisable to consult the intended approach with a statutory auditor and draw on their knowledge and experience of observed practices.

Find out how we can support your business

Qualifying assets

Capitalisation of borrowing costs applies to qualifying assets, i.e. assets that necessarily take a substantial period of time to get ready for their intended use or sale.

In practice, qualifying assets most often include:

- assets under construction,

- investment property,

- inventory of work in progress (e.g. in long-term projects).

Both domestic regulations and IAS require borrowing costs to be capitalised from the commencement of work on the asset until it is ready for use or sale.

Capitalisation of specific borrowing costs

Specific borrowing costs arise when a company incurs liabilities exclusively to finance a particular investment (e.g. taking out a loan to build a production hall).

Example:

Assume that Company X started a three-year investment project in January 2025 involving the construction of a new production line, with a total estimated cost of PLN 3,500,000. The project meets the definition of a qualifying asset, as it requires a substantial period of time to prepare it for use.

In the first year of the investment, the company used two sources of external financing:

- Loan A: PLN 1,000,000 with an interest rate of 6% (funds received in December 2024).

- Loan B: PLN 2,000,000 with an interest rate of 8% (funds received on 1 April 2025).

| Source of financing | Annual interest rate | Amount of debt | Share of financing period per year | Interest amount |

| Loan A | 6% | 1 000 000 | 12 months | 60,000 |

| Loan B | 8% | 2 000 000 | 9 months | 160,000 |

Funds obtained from the loans that had not yet been used for the investment were not invested.

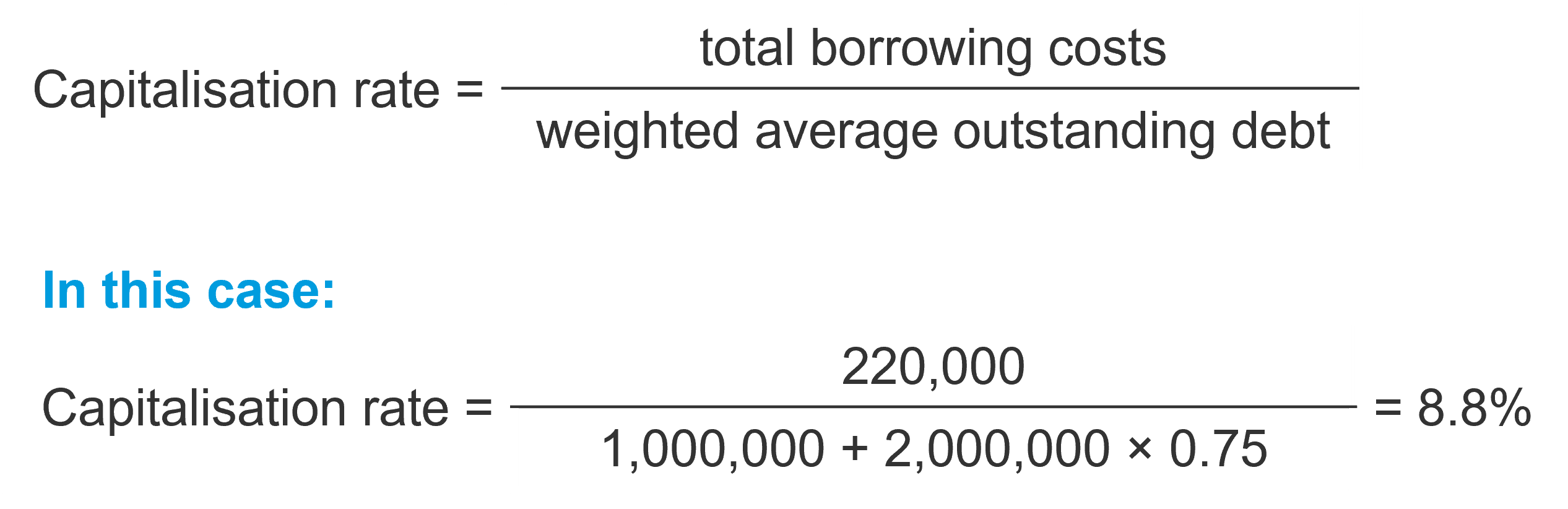

In this case, all liabilities finance the construction of the facility, therefore the related financing costs qualify for capitalisation in the initial value of the asset. The capitalisation rate is calculated using the formula:

The schedule of expenditures incurred for the asset under construction in the first year of the investment was as follows:

| Date of expenditure | Amount |

| 01.04.2025 | 600,000 |

| 01.07.2025 | 700,000 |

| 01.10.2025 | 400,000 |

| Total | 1,700,000 |

Borrowing costs to be capitalised are determined as the product of the capitalisation rate and the weighted average expenditure on the asset. Therefore, borrowing costs capitalised in 2025 amount to:

| PLN 600,000 | × 8.8% | × 9/12 | = PLN 39,600 | borrowing costs from 01.04 |

| PLN 700,000 | × 8.8% | × 6/12 | = PLN 30,800 | borrowing costs from 01.07 |

| PLN 400,000 | × 8.8% | × 3/12 | = PLN 8,800 | borrowing costs from 01.10 |

| Total | = PLN 79,200 | |||

Capitalisation of general borrowing costs in accordance with IAS 23

General financing covers liabilities not assigned to a specific investment – such as bond issuances or overdraft facilities. IAS 23 permits the capitalisation of part of general borrowing costs if the entity incurs expenditure on qualifying assets.

In practice, it is difficult to directly assign a specific portion of a loan to a given investment expenditure. Therefore, entities apply proportional allocation, for example:

Expenditure financed by specific borrowing should be excluded from the calculation. It is also important that the capitalised amount does not exceed the total borrowing costs incurred in a given period.

Practical recommendations for those responsible for capitalisation

When taking out loans and borrowings and conducting activities financed externally, it is worth remembering two aspects that facilitate proper recognition in the accounts:

- documentation – each capitalisation should be supported by appropriate documentation, including an investment schedule and financing agreements,

- cooperation – ensuring compliance with regulations requires close cooperation between the finance department, accounting and auditors.

What are financing acquisition costs?

Financing acquisition costs are expenses incurred by an entity in connection with obtaining funding, regardless of the outcome. They include, among others:

- financial advisory services,

- legal analyses of contracts,

- market research,

- development of business models.

Such costs are not subject to capitalisation and should be recognised in the profit or loss for the period in which they were incurred.

Income related to external financing

Income related to external financing – such as positive exchange differences, interest on unused funds or income from deposits – may reduce the value of the asset if it relates to funds intended for its financing.

Borrowing of financial resources is a complex matter

Capitalisation of borrowing costs is a tool that can significantly affect a company’s financial position and should therefore be applied with due care, taking into account numerous regulations and factors. Correctly distinguishing between specific and general financing – and properly applying capitalisation principles – is not a minor detail, but something that allows for a fair presentation of investment values and financial performance.