The COVID-19 pandemic has caused severe disruption to the global economy with its effects yet to be fully felt in various business sectors. Whilst assessing the impact, the Singapore Government has announced a series of COVID-19 relief measures over a record four Budgets, including Property Tax Rebate and Rental Relief Framework, which are aimed at cushioning the economic consequences brought about by the pandemic on individuals and businesses.

The Rental Relief Framework is designed to provide mandated equitable co-sharing of rental obligations between the Government, landlords and tenants. The principal aim is to help affected Small and Medium-sized Enterprises (“SMEs”) who need more time and support to recover from the pandemic. In the longer term, landlords stand to benefit from the recovery of SME tenants as this would ensure the continued viability of the rental and property market. The Framework also extends to cover eligible Non-Profit Organisation (“NPO”) tenants.

An Overview of the Rental Relief Framework

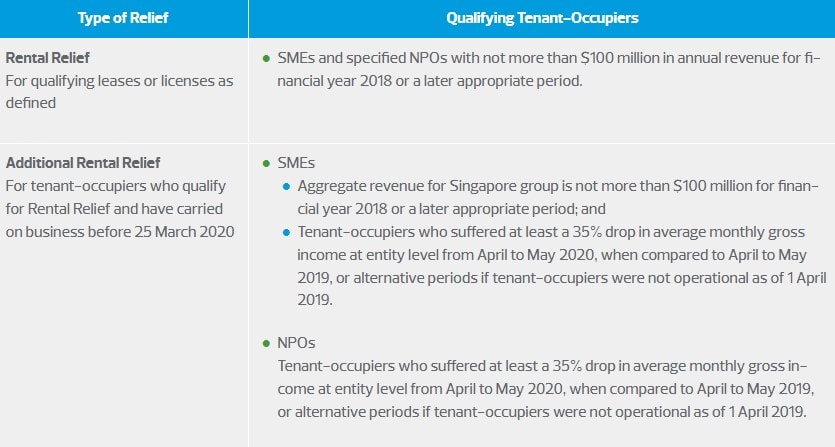

Eligible SMEs and NPOs who are tenant-occupiers qualify for the following benefits under the Rental Relief Framework.

May vary if tenant-occupier does not occupy the property throughout the relief period.

The rental to be waived is based on contractual rent that property owners concluded with their tenants and excludes any maintenance fees and charges for the provision of services such as cleaning and security.

Government assistance

The Government assistance to property owners is in two parts - (a) Property Tax Rebate for property tax paid for year 2020 and (b) the Government Cash Grant.

a) Property Tax Rebate (“PTR”)

Property owners of qualifying properties received PTR from IRAS calculated at either 30%, 60% or 100% of the property tax paid for year 2020, depending on the severity of COVID-19 impact on the businesses concerned.

Property owners are to fully pass on the PTR to their tenants within the following prescribed timeframe:

- by 31 July 2020 for January to June 2020 PTR.

- by 31 December 2020 for July to December 2020 PTR.

The PTR to tenants could be settled via a monetary payment or a reduction/offset in rental payments.

In the event of a dispute, either party may approach the Valuation Review Panel, no later than 31 December 2021, for a resolution.

b) Government Cash Grant

Government Cash Grant is disbursed by IRAS to property owners with eligible SME and NPO tenant-occupiers. Property owners are to on-pass such benefit to tenants by way of rental waivers.

Property owners are obliged to notify eligible SME and NPO tenants within 4 working days upon receipt of the Notice of Cash Grant and Rental Waiver from IRAS. Failure to do so, without reasonable excuse, is an offence under the COVID-19 (Temporary Measures)(Amendment) Act. Property owners should notify IRAS by 21 October 2020 if they have not received such Notice.

Eligibility criteria for tenant-occupiers to qualify for Relief

Property owners are tasked to ascertain if their tenant-occupiers met the following criteria to qualify for the Rental Relief and Additional Rental Relief.

Interactions between PTR and Rental Relief Framework

With the introduction of the Rental Relief Framework, property owners are mandatorily required to determine the total number of months (up to four) that rentals must be waived for eligible tenant-occupiers in terms of their entitlement to the Rental Relief and Additional Rental Relief. The PTR disbursed prior to 1 August 2020 plus any other monetary payments made previously may be taken into consideration in arriving at the remaining entitlement to the benefits, which will be settled via rental waivers.

The Government Assistance is calculated by reference to annual value of the properties. The benefits to be passed on by owners to tenants however are based on contractual rentals. In view of the differing bases adopted, what property owners received from IRAS and what they subsequently passed on to tenants may be different amounts. Landlords may keep any excess Cash Grant but not the PTR. On the other hand, if there is a shortfall, landlords would still have to give the full rental waiver as required by law.

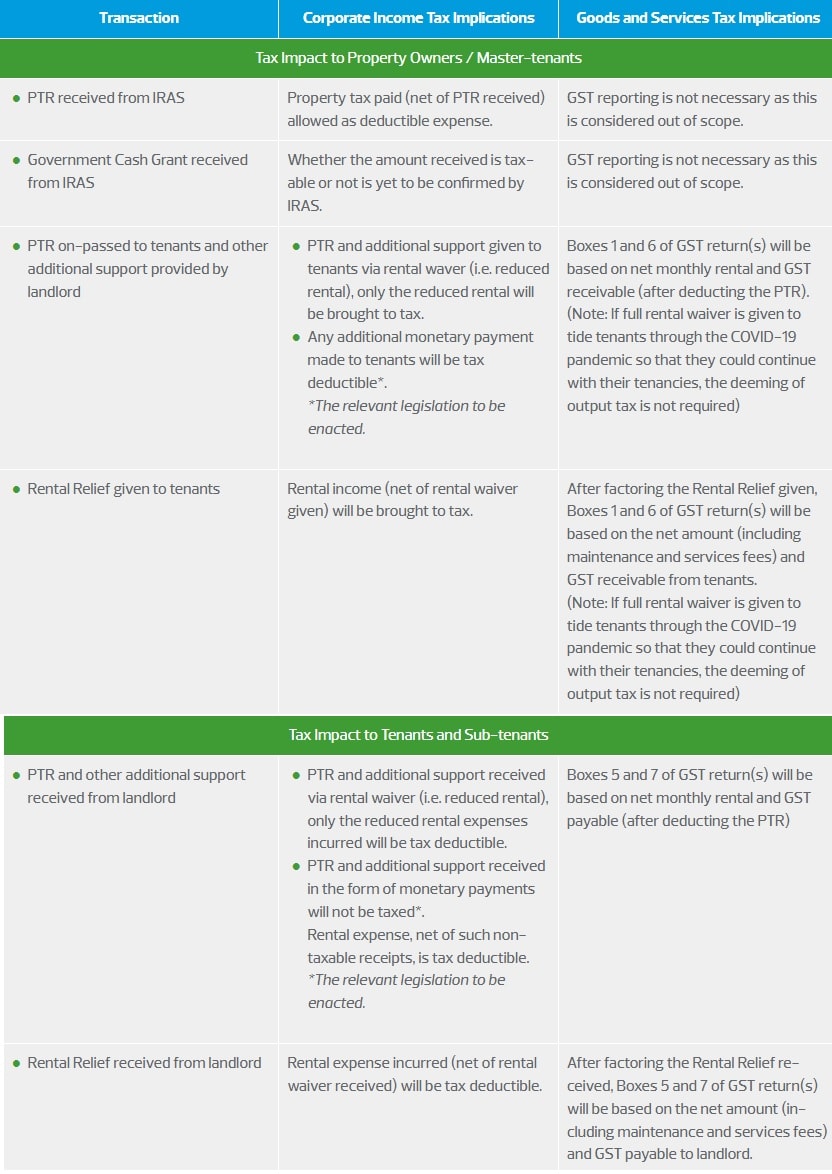

Corporate income tax and Goods and Services Tax implications

Corporate income tax and Goods and Services Tax implications are summarised in the table below.

This brief has been prepared for general information only. It is not intended to be relied upon as accounting and/or tax advice. Please feel free to reach out to our team for further clarifications and advice.

For further information or assistance, please contact:

| Koh Puay Hoon, Partner & Head of Tax T +65 6594 7820 [email protected] | Cindy Lim, International Tax Partner T +65 6594 7852 [email protected] |

| William Chua, Partner T +65 6594 7860 [email protected] | Richard Ong, Partner T +65 6594 7821 [email protected] |