An entity shall disclose material information about the sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s prospects (IFRS S1, Paragraph 17).

Understanding materiality

Materiality refers to information that could influence stakeholder decisions. There are two primary approaches to materiality, depending on the target stakeholders or the sustainability reporting framework adopted:

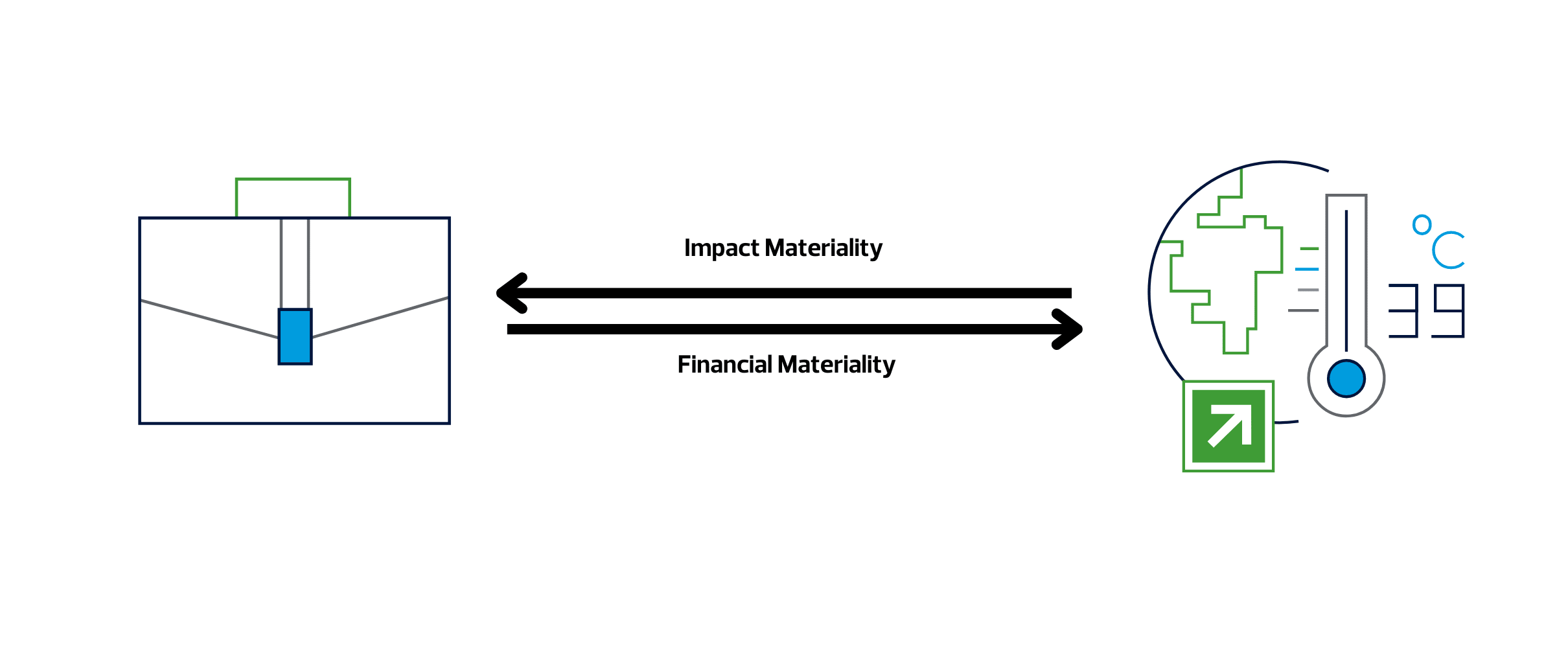

Financial materiality – Focuses on how sustainability factors impact an entity’s financial performance, such as increased operational costs, decreased revenue or asset devaluation. TCFD and IFRS adopt this approach by focusing on financial disclosures that shape investment decisions made by users of financial reports, such as investors and lenders.

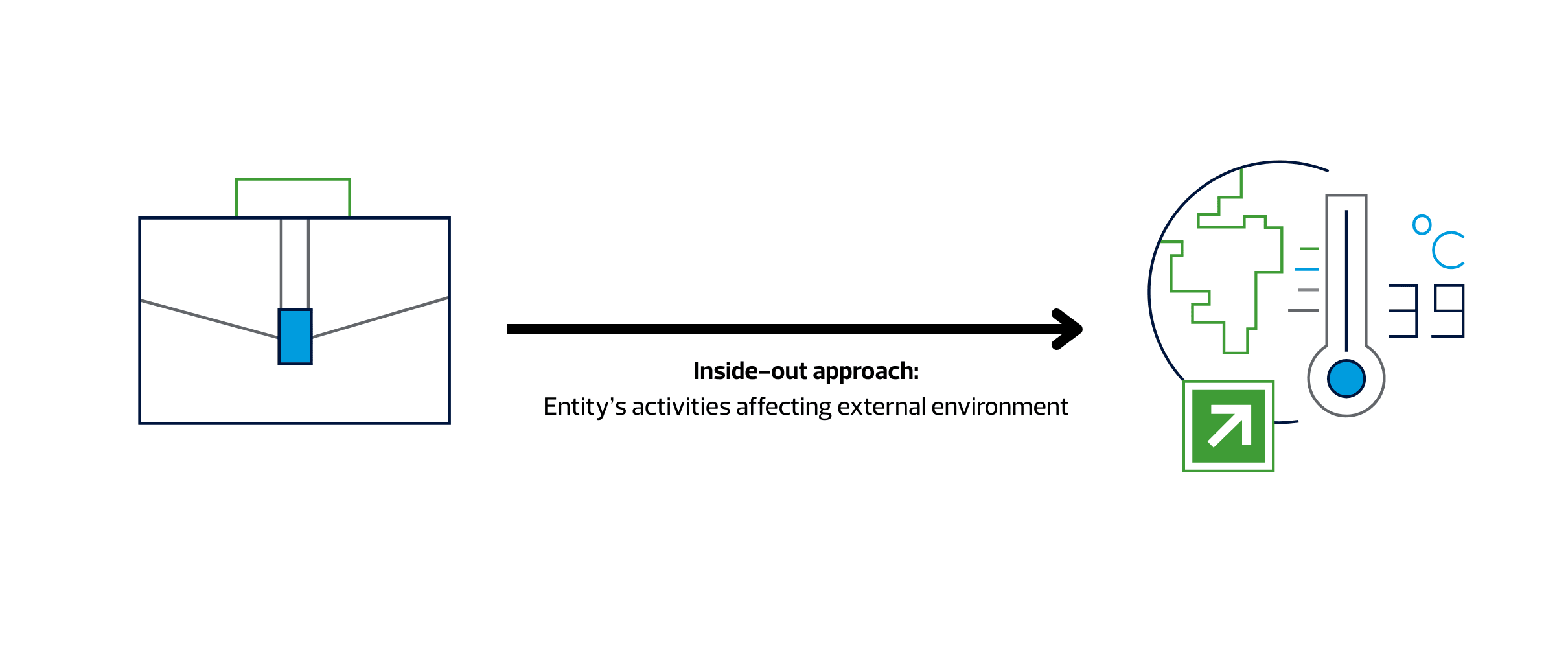

Impact materiality – Considers how an entity’s activities affect the external environment, such as climate change, pollution and human rights. The GRI Standards apply this approach, addressing a wider range of stakeholders including the local community, employees and regulators.

Double materiality, a key concept under the European Union’s CSRD, incorporates both financial and impact materiality.

Putting materiality into practice

Biodiversity, waste management, child labour, water pollution—these are all critical sustainability issues. But when it comes to reporting, how do we decide which topics truly matter to include? This is where a materiality assessment becomes essential. It helps prioritise the sustainability topics that matter most to both the entity and its stakeholders.

Here’s a step-by-step guide for making materiality judgements under the IFRS Sustainability Disclosure Standards:

| Identify | Assess | Organise | Reassess |

| sustainability topics that could influence stakeholder decision-making use industry specific metrics, search for emerging environmental or social issues, or conduct stakeholder engagement to gather opinions | the relevance and significance of each topic over short, medium and long-term | material topics using tools like a materiality matrix to enable clear communication through visual representation | material topics annually to ensure they remain relevant based on both internal developments and changes in the external environment |

Turning materiality into business value

A well-executed materiality assessment can bring several benefits to an entity:

- Enhanced risk management: Identifying material sustainability-related risks allows entities to plan ahead and be better prepared to mitigate potential disruptions to operations.

- Strengthened investor trust: Transparent sustainability disclosures show an entity’s accountability in addressing material risks, helping build investor confidence in the entity’s management and positively influencing investment decisions.

- New business opportunities: Addressing material risks may unlock innovation and new investments opportunities, such as renewable energy or green financing, gradually enhancing market reputation.

In our client engagements, we’ve seen this in action. For example, one of our clients in the chemicals industry, driven by increasing consumer awareness and a shift away from toxic chemicals. We noted a potential decline in revenue - an area of concern raised by business partners and investors during stakeholder engagement. In response, the client began exploring opportunities to diversify its product offerings by developing non-hazardous alternatives. This strategic pivot not only mitigates the identified risk but also aligns with stakeholder expectations—turning a challenge into an opportunity for sustainable growth.

Looking ahead

When applied strategically, materiality enhances the value of your sustainability report from a mere compliance exercise to a valuable strategic asset. It can serve as a decisive factor for investors and create collaboration opportunities with both governmental and non-governmental organisations, contributing to the long-term financial resilience of your business. In today’s dynamic landscape - marked by geopolitical shifts such as tariff disputes, extreme weather events like heavy rainfall and heatwaves, and evolving sustainability reporting regulations - a responsive and forward-looking materiality process is critical to protecting your business operations. For further guidance, refer to the IFRS S1 sections on “Materiality” and “Identifying material information.”