As part of the collective effort in managing the impact COVID-19 has on tenants and owners of non-residential properties, rental waivers in full or in partial (“Rental Waiver”) have been extended on top of passing property tax and enhanced property tax rebate1 (“the Rebate”) to support tenants to tide over this challenging period.

To facilitate GST registered property owners and tenants in aligning and managing the GST reporting requirements as well as risk covering such arrangements relating to the Rebate and Rental Waiver, we have summarised them into salient points as shown below:

We have further illustrated three common scenarios below that GST registered property owners and tenants need to know with regards to GST reporting position for the upcoming quarter(s):

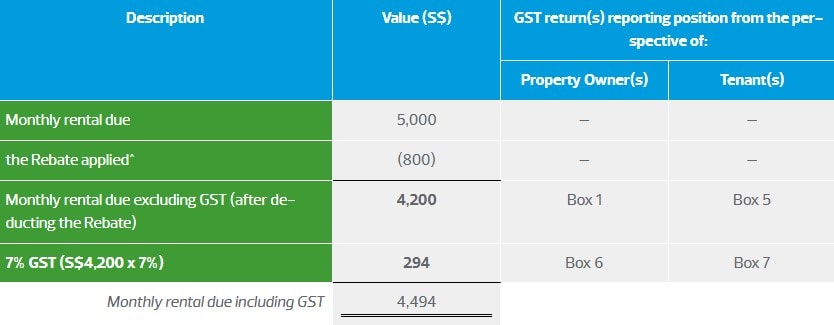

Illustration 1: Passing the Rebate from Property Owners to Tenants:

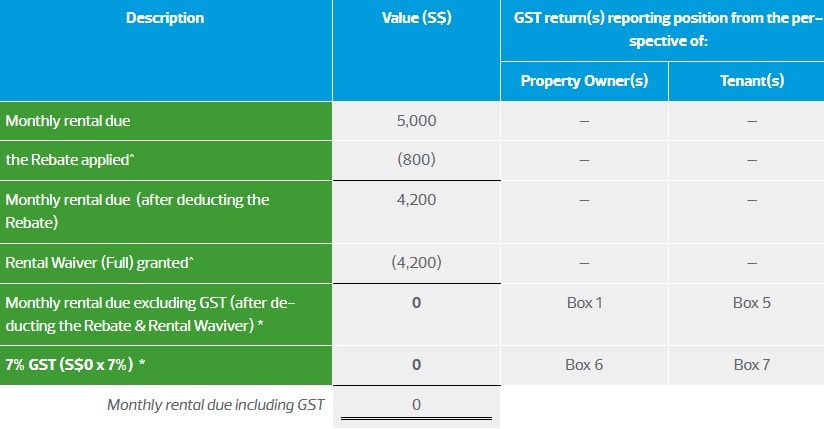

Illustration 2: Passing the Rebate and Granting Rental Waiver (Full) from Property Owners to Tenants:

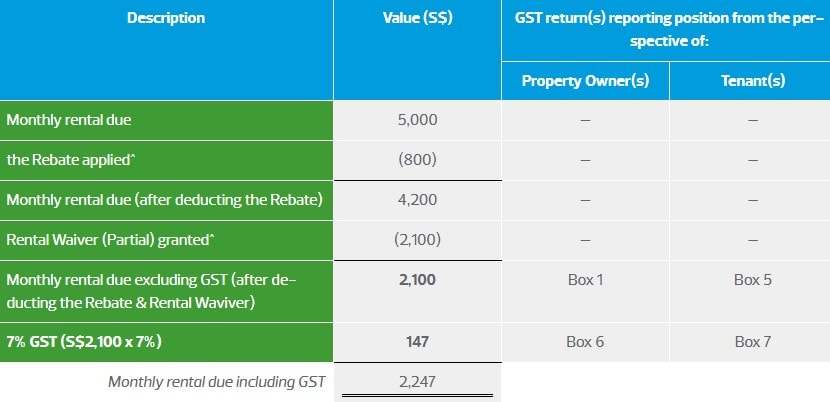

Illustration 3: Passing the Rebate and Granting Rental Waiver (Partial) from Property Owners to Tenants:

^ Amount illustrated excludes GST

* Deeming of output tax is not required considering the intent is to tide tenant(s) through this period so that they could continue with their tenancies.

Besides the above, GST registered property owners and tenants need to ensure their GST reporting position covering other supply and purchase transactions are aligned with GST requirements as an on-going process to minimise potential penalty/fine should an IRAS GST audit be initiated.

We support GST registered businesses to minimise and manage GST risks by utilising technology and applying specific industry knowledge to help them manage their GST position effectively and practically.

For more information, contact our team of GST professionals:

| Richard Ong, Partner T +65 6594 7821 [email protected] | |

| Lee Meow Ling, Senior Manager T +65 6715 1143 [email protected] |

=====================

1 The property tax and enhanced property tax rebate for non-residential properties announced during the FY2020 Budget and FY2020 Supplementary Budget covers a discount ranging from 30% to 100% of property tax payable by property owner(s) for 1 January 2020 to 31 December 2020.