This article answers the following questions:

- How should accruals be recorded?

- What distinguishes prepaid expenses from accrued expenses?

- How can risks arising from discrepancies between local and group accounting standards be mitigated?

Accruals are among those accounting topics that may appear simple at first glance, yet in practice can pose considerable challenges – particularly for organisations operating in international environments, where financial processes are decentralised and accountability for their proper execution is dispersed. So how should they be managed to meet both Polish and global requirements? To answer this, it is worth examining accruals from the perspective of an auditor who reviews and optimises the accounting procedures in place.

What are prepaid and accrued expenses used for?

What exactly are cost accruals and what is their purpose? Cost accruals allow accountants to allocate expenses to the correct reporting periods. This is essential for maintaining the fundamental principles of accounting and – consequently – for preparing financial statements that accurately and transparently reflect the financial position and performance of the entity.

Cost accruals are divided into two categories:

- Prepaid expenses – costs incurred in the current period that relate to future reporting periods (e.g. prepaid insurance, subscriptions or memberships).

- Accrued expenses – costs relating to the current reporting period, recognised even if they have not yet been formally documented, such as via an invoice (e.g. salaries for the last month of the year or unbilled services).

The classification into prepaid and accrued expenses ensures that costs are correctly attributed to the period to which they actually pertain – regardless of the timing of payment or invoice issuance.

It sounds straightforward, so where do the difficulties lie? The realities of modern business – characterised by decentralised processes, outsourced accounting functions and data processing, the use of varying accounting standards for statutory and group purposes, and the inevitable automation of processes – bring new challenges. These require not only technical expertise but also flexibility in adapting procedures and internal controls.

Learn more about our services

What problems does modern accounting face when allocating costs?

Many companies today operate within decentralised structures: certain processes (or their components) are carried out in different locations and time zones, by remote teams or entirely outside the organisation. This impedes the efficient flow of information and documents, and thus the timely identification and verification of source documentation necessary for accurate accounting treatment of costs over time.

In decentralised entities, the most common issues are:

- for prepaid expenses:

- one-off recognition of costs in the period’s result that should be spread over time;

- holding costs on the balance sheet that should have been allocated to prior periods;

- for accrued expenses:

- omitting costs incurred in the period due to lack of an invoice;

- recognising costs based on requests without adequate supporting documentation (which complicates analysis in subsequent periods and is problematic during tax audits or financial audits);

- holding accruals on the balance sheet for months (or years) simply because the timing of their recognition was missed by the accountant.

Entities seeking to avoid such issues and the associated risks should focus on properly designing financial processes, embedding control mechanisms, and implementing internal audits that serve both preventive (e.g. through substantive document analysis) and detective functions (e.g. via well-designed balance reconciliation procedures).

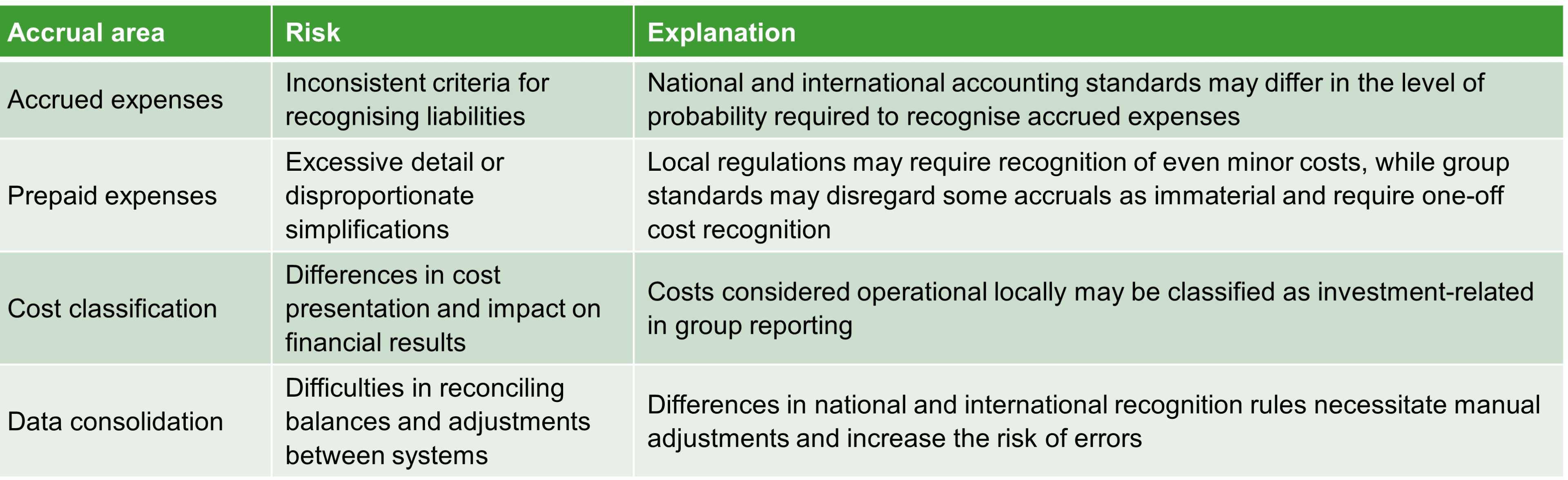

In addition to challenges related to decentralised processes and disrupted information flow, accountants managing cost accruals in international structures often face difficulties caused by dual reporting, which requires entities to maintain books in parallel according to national regulations (e.g. the Accounting Act) and group standards (e.g. International Financial Reporting Standards – IFRS).

Risks arising from dual financial reporting can be grouped into four key areas:

How to properly account for cost accruals in the balance sheet?

Accounting practice shows that group data, reported cyclically throughout the year (often even monthly), is subject to more rigorous procedures than statutory data, which is most intensively processed once a year during financial statement preparation.

To mitigate risks arising from discrepancies between local and group accounting standards, an entity should implement a consistent accounting policy that incorporates both reporting models.

Proper recognition of cost accruals also requires other actions. Key among them are:

- close collaboration (and effective information exchange) between the accounting team and financial controllers,

- regular training on both local and group reporting standards and implementation of technical solutions (often available in modern ERP systems) that enable clear dual-track accounting,

- appropriate control procedures, especially in areas requiring estimates.

How can a modern accounting system facilitate cost accruals?

In the world of modern accounting, enterprise financial management systems (ERP systems) and dedicated analytical and reporting tools play a key role in monitoring cost accruals. These solutions enable organisations not only to automate accounting processes but also to analyse and control them in real time. With these tools, it is possible to:

- create accrual schedules,

- assign accrual codes to documents,

- analyse data in real time.

However, full automation of cost recognition and accounting carries risks. Common issues include:

- incorrect system configuration,

- automatic posting without validation,

- limited access to clear supporting documentation,

- lack of integration with the accounting policy,

- limited auditability,

- incomplete accruals due to information flow outside the system.

Potential problems associated with new tools make it essential to ensure process traceability and documentation of the algorithms used by the system. Equally important are configuration and access reviews, as well as internal training.

Process and documentation transparency is even more critical for entities whose financial statements are audited by a statutory auditor.

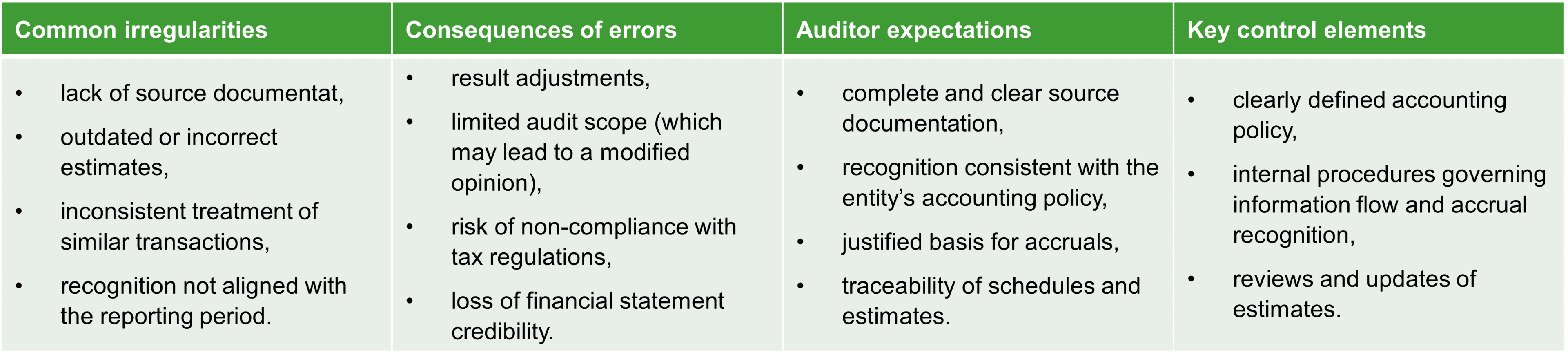

An organisation preparing for a financial statement audit should therefore also consider the expectations – particularly regarding documentation – of the audit team. When accounting for cost accruals, four key factors contribute to successful completion of the process:

Properly recognised cost accruals in the balance sheet reflect the quality of accounting processes and procedures

Although often seen as a technical detail in accounting, cost accruals – in the face of a rapidly changing business environment – in a sense reflect both the organisation’s condition and the quality of its implemented processes. Accruals operate at the intersection of various departments within an organisation, and thus clearly illustrate how effectively the entity functions in international structures. They reveal whether the organisation manages financial information efficiently and allow assessment of how well its internal control environment operates.

It is therefore worth giving them the attention they deserve.