Boards of all charities are required to have an Audit Committee (‘AC’) and a Finance Committee (‘FC’) under the 2017 Singapore Code of Governance for Charities & Institutions of a Public Character. However, charities differ in their views on whether both the AC and FC are necessary as the committees need to be headed by board members with relevant accounting qualifications and experiences, but limited availability of qualified directors remains a common constraint.

While both the AC and FC relate to finance matters, they play different roles in the organisation. The AC provides oversight on the operational effectiveness of internal controls and risk management frameworks and processes, whereas the FC establishes financial reporting and financial management controls. In addition, the committees should be independent of each other to avoid a conflict of interests, but flexible arrangements, such as joint meetings and regular communications, can be made to facilitate efficient decision-making.

Some charities feel that the FC may not be necessary as its responsibilities, such as reviewing financial reports and setting budgets, could be shared among the finance staff and board members. But others believe that the FC is essential as the finance function in charities is usually not adequately staffed and therefore support from the FC for finance operations is indispensable. Furthermore, an effective FC would ensure the efficient use of resources for charitable programmes.

It is therefore ideal for charities to have separate audit and finance committees for operational and governance purposes. However, the extent of support from the FC for financial operations depends on the capability of the charity’s finance department. In order to address the limited availability of qualified directors, charities may consider inviting non-board members to sit on the AC and FC.

Key pillars of an effective AC

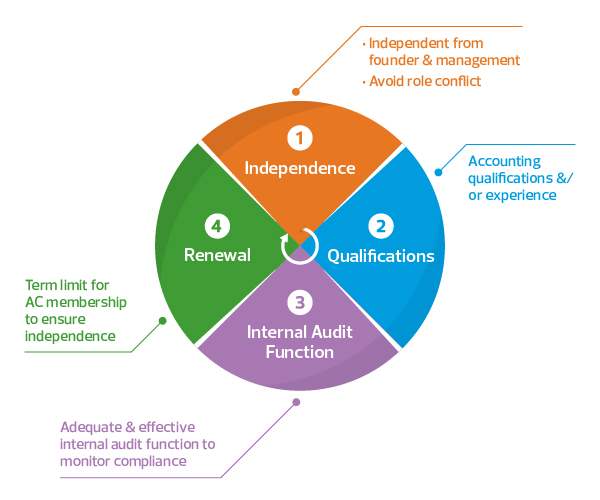

An effective AC should consist of four key pillars—independence, qualification, the internal audit function and renewal—as shown in the following diagram.

Four Pillars of an Effective Audit Committee

Independence means that the AC should be independent from other operational committees and management so that it can provide an objective view.

AC members should also have the appropriate accounting qualifications and experience, as well as understand the charity’s operations to properly identify the risks faced by the organisation.

The internal audit function should ensure that internal audit findings are promptly reported to the AC. This allows top management to be notified of operational issues for follow-up actions and continuous improvement.

The final pillar, or renewal, involves setting an appropriate term limit for AC members to prevent overfamiliarity and a reluctance to reveal issues overlooked previously. It is recommended that AC members should serve for not more than six years to allow for fresh ideas and new initiatives.

Need for better understanding of internal audit

While charities normally engage external auditors for the annual statutory audit, the need for internal audits is not well understood by many in the sector. External audit focuses on checking financial statements to ensure that they are free from material misstatement, whereas internal audit covers internal control processes that address both financial and non-financial risks, such as cybersecurity, compliance with fundraising regulations and public image management.

External auditors are appointed through the annual general meeting, while internal auditors are usually appointed by the AC to assist the committee in reviewing the design and operational effectiveness of internal controls.

If internal auditors are not engaged, internal control reviews can be performed by other staff or members, the AC itself or a partner organisation. Good internal controls ensure that the charity adopts systemic approaches on decision-making, resource planning and service delivery to achieve its objectives. Therefore, as the governance body that provides independent oversight of the internal control system, the AC plays a vital role in this process.

This article was written by Sovann Giang, Business Consulting Senior Director & Deputy Industry Lead of our NPO Practice.